3 companies inflecting towards high ROIC

Inflection Investing

Two weeks ago, I wrote about going beyond ROIC

And most of us use ROIC as one of our favorite ratios, by a wide margin.

And then I showed you the ROIC chart from the company Medpace [MEDP]:

And a great question came from you guys:

“How to identify the company’s potential in December 2016?”

Well, I’m not sure you could have. Maybe.

But if we have more data points, we could increase our odds. Here’s what I mean:

After the IPO, Medpace was, for a moment, trading at a P/E < 90. In the next 2 years, it started making more and more profits, and ROIC increased. So, a more realistic time to get into the company would be at the start of 2019, when you had more historical data (3 data points.

And just to be clear, if you bought Medpace on the 7th of February at 66USD, and you held it until today -> 6-bagger or 33% CAGR.

In other words, there is no reason for anxiety, we have time.

Secondly, always take into account where the company is in its lifecycle. Medpace at the end of 2016 had a net profit margin of 3%. In 2014 and 2015, it was unprofitable. Usually, when companies tip over from unprofitable to profitable, their profitability rapidly increases in those first years (for Medpace, EPS doubled two years in a row).

Great, some insights from the past, now how to use them to spot potential winners for the future?

Let’s take Medpace as a blueprint and screen for companies that exhibit a similar pattern.

Here’s our screening criteria:

ROIC < 10%

ROIC increasing for 3 years

The company is profitable now (but not in the past)

We use unclestock.com the most powerful screener known to man. The criteria are pretty wide, but here are 3 companies on an inflection point.

Docusign (Ticker: DOCU)

Description

What’s in a name? DocuSign helps businesses and individuals manage and sign documents electronically. Its platform is available in 180 countries and 44 languages. It’s a SaaS company used by 1 billion people.

The data

First off, there is an unusual item that skews the ROIC calculation (Finchat uses the net profit so we need to correct for that.

DocuSign has inflected, though it became profitable in October of 2023, and profitability seems to be increasing. If we correct the current ROIC for the outlier, and calculate the ROIC based on NOPAT and invested capital, I get:

2022: < 0%

2023: 1.6%

2024: 5.3%

Now when we look at what price it trades, we have to correct the data based on the above discussion.

Conclusion

Although Docusign has inflected towards profitability, a lot of EPS growth needs to happen to justify the current price in the market. If you think this company, as Medpace did, can double its EPS in the coming 2 years, and afterward, keep growing at 40%, then it could be a great investment.

Do you own DocuSign?

ServiceNow (Ticker: NOW)

Description

Another platform (I swear, I wasn’t looking on purpose). ServiceNow helps businesses streamline and automate workflows to increase efficiency. It started for IT service management but has since expanded into HR, Customer Service, and security operations. It’s a SaaS business just like DocuSign.

The data

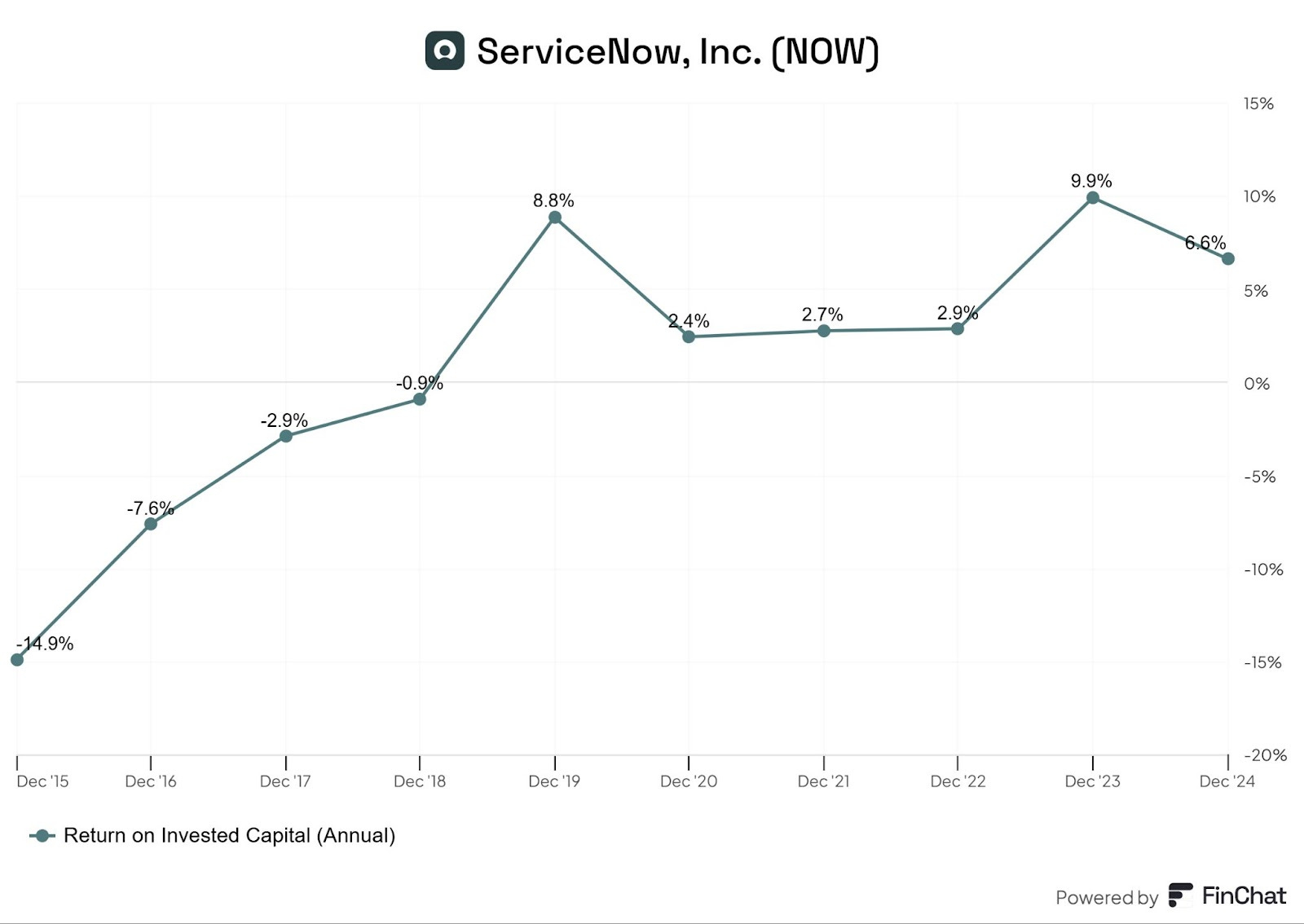

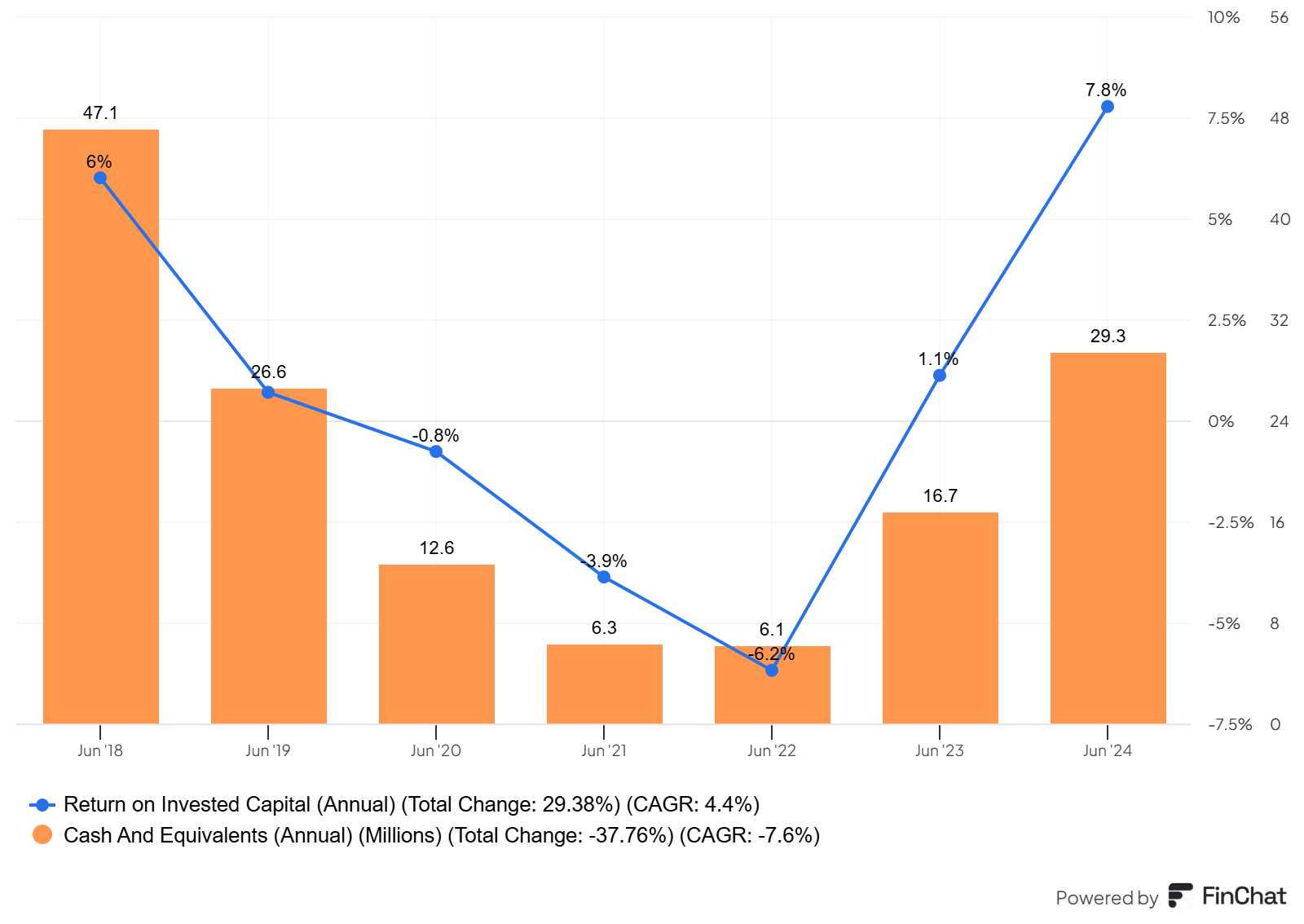

ServiceNow has already inflected a couple of years ago.

But based on ROIC, it has somehow stagnated.

However, there is a big difference with the aforementioned Docusign:

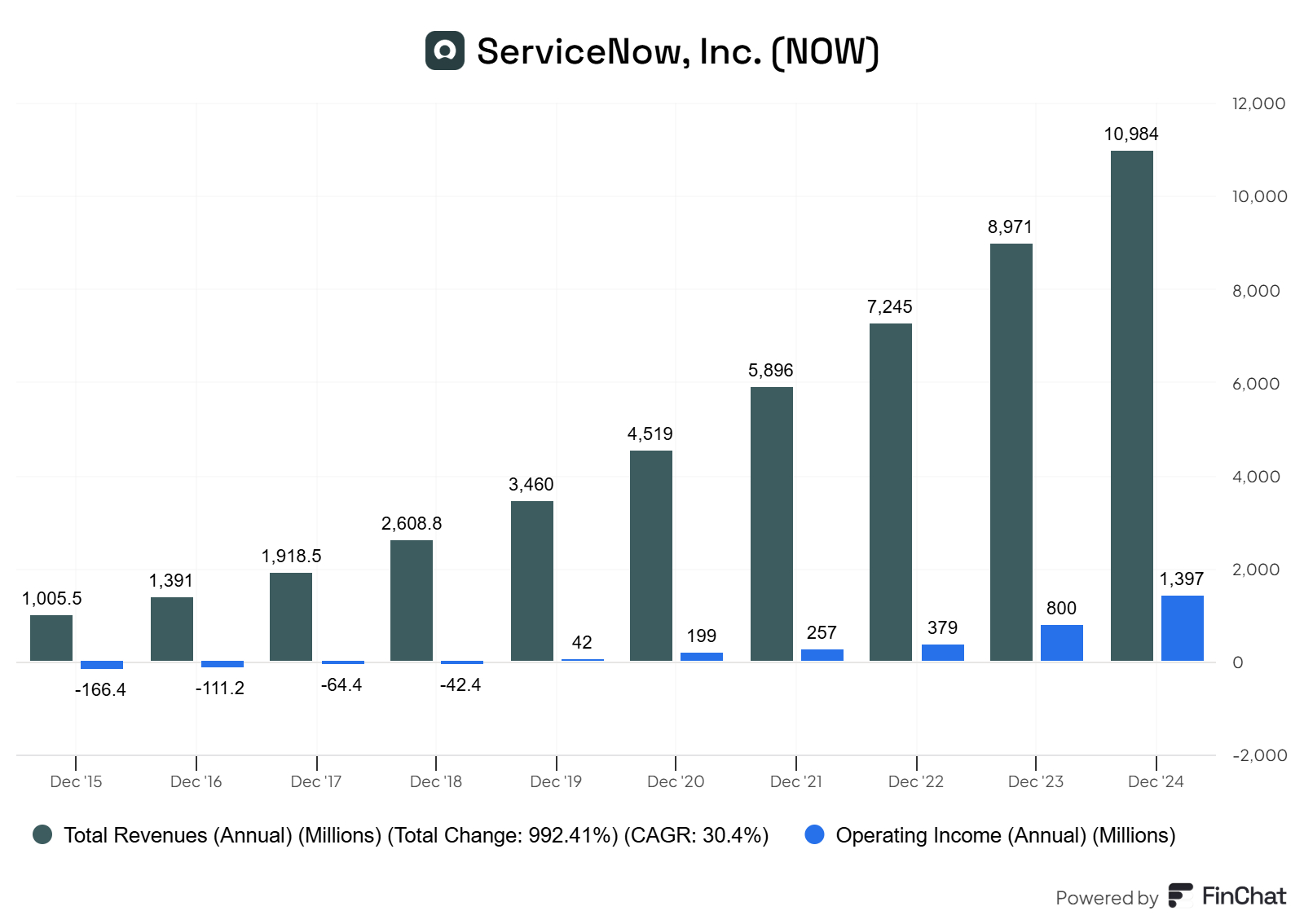

Revenue keeps growing at a solid pace and operating income significantly increased over the last 2 years.

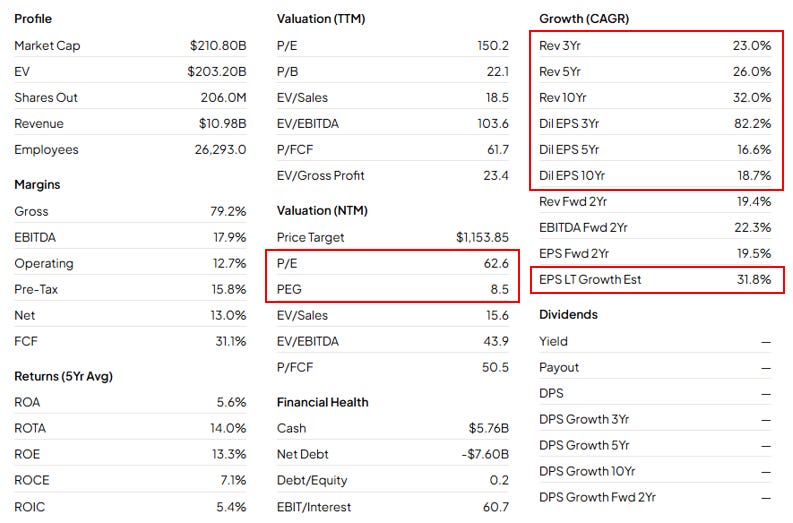

But no matter how you turn this stone, you need a lot of growth to justify the current price in the market:

Conclusion

ServiceNow seems to be the stronger company compared to DocuSign. And although it will go stronger still, a lot of growth is already priced in at the moment.

Do you own ServiceNow?

The 2 examples above have already inflected from unprofitable to profitable. Let’s see if we can find one that is on the verge of inflection.

Fiverr(Ticker: FIVR)

Description

I’m supposing you already know Fiverr. It’s an online marketplace connecting freelancers with businesses or other individuals. For each “gig” a freelancer sells to someone, Fiverr takes a 20% cut.

The data

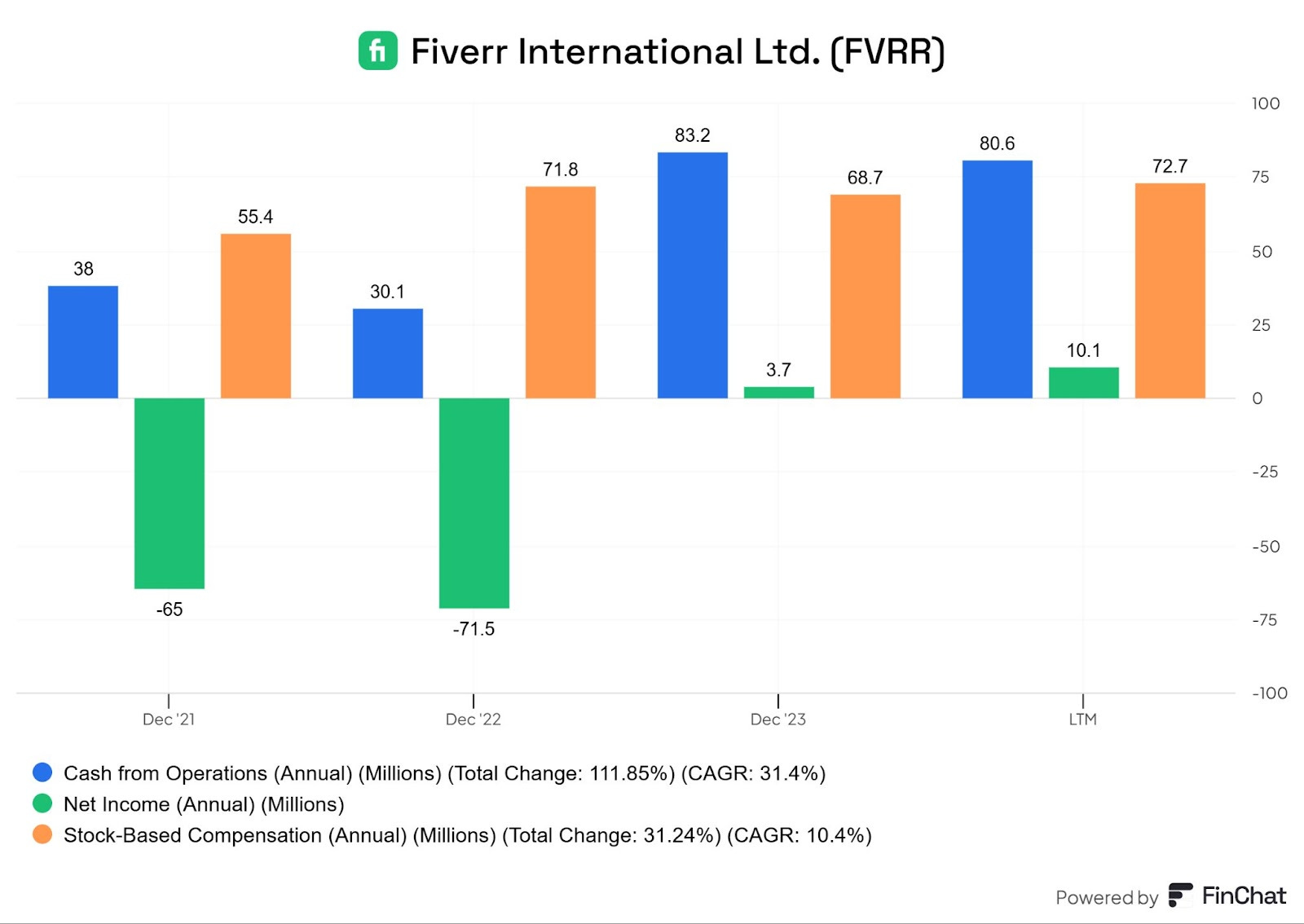

Fiverr runs a marketplace at a deficit. Their EBIT is negative, but their EBT is positive because of interest income. This means that their marketplace is not making a lot of money from an operational standpoint at the moment. Looking at the income statement, this seems like a company where we need to examine cash flows more closely.

There is very decent cash flow from operations and few investments at this time. I am not sure how this will impact growth in the future, but based on an FCF yield, it sits at 7%.

You would be wrong though.

The 80 Million in operational cash flow is because Stock-Based Compensation (not in cash) is added back to the income.

Indeed, there has been an inflection towards positive net income, however, the operational cash flow is dominated by stock-based compensation (which does not flow back to the investors).

Conclusion

Yeah. “Me not liking this.”

Although the business seems to be inflecting, not a lot of cash is coming in at the moment. Although I believe in the “gig economy,” I would need more time with the company to see if it can reign supreme. Their competitor, Upwork, has fairly similar economics.

Do you own Fiverr?

The moral of the story

Always take into account the lifecycle of the company

Don’t just focus on the what and the how search for the why

I believe screeners can be useful when searching for change

I’m a big fan of Finchat, but always be skeptical when looking at the numbers

Now I did find one company with the following chart

Company inflecting

Cash position increasing

Trading in the market at a P/E = 1

But I need to spend more time on it, to avoid drawing rash conclusions (future article coming up if it amounts to something)

How do you look for change in the markets?

May the markets be with you, always!

Kevin

Great post, thanks for sharing, Kevin! 😎

Thanks for sharing this. Taking this instruction, what do you think about #GRAB.

Grab Holding