A death-focused serial acquirer: recession-proof

Death and taxes.

This week’s setup

A short overview of the markets

Rumbu Holdings, a tiny serial acquirer

How to measure dilution risk in microcap companies

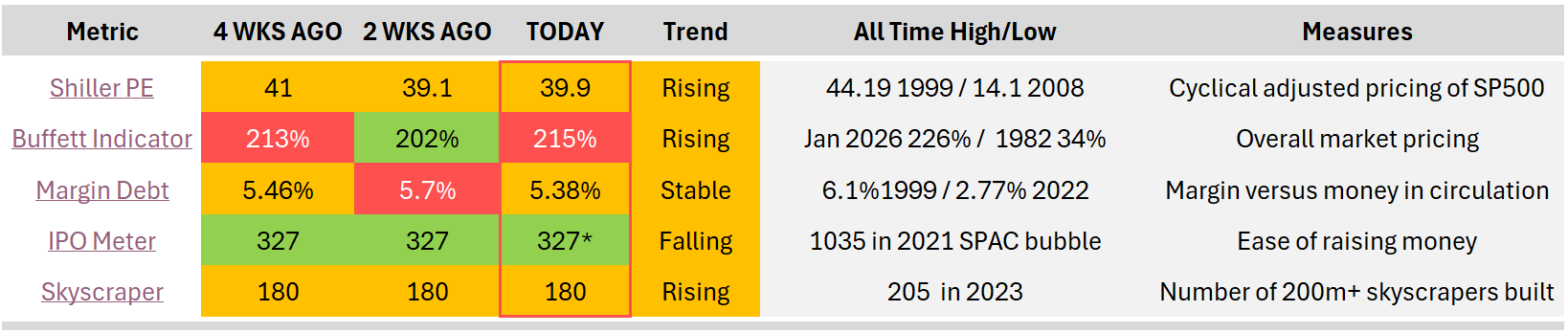

1. Bubble meter

“We look at some metrics to gauge what the market temperature is.”

Note: Take the skyscraper metric with a grain of salt

After war troubles, the market has jumped once more. Shiller PE has risen, and the Buffett indicator has briefly touched 200%. Margin debt has declined a little bit, and IPO’s are still flowing (96 this year in the US).

You know I follow the macro from afar. If a tariff storm comes in, it’s easy to check your companies. I did do a quick portfolio check with the Hormuz blockage, but nothing to worry about.

2. Stock in the funnel

Peter Lynch always said to go look at boring businesses. Well, I found one, and it sits in our serial acquirer database.

Rumbu Holdings (Ticker: RMB.V) is a microcap Canadian serial acquirer that buys up funeral homes. Here’s my first assessment of the company.

Description: Never heard of it? Neither had I if I hadn’t built the database. Rumbu Holdings buys funeral homes in Western Canada. That’s the business. Death care. This business is recession-proof. People die. They’ll keep dying. (don’t want to sound too morbid, but it’s true).

Type: Early-stage micro-cap roll-up

Why it’s interesting: Canada’s death-care industry generates C$1.5–1.8 billion a year. More than 70% of it is still family-owned. Not chains. Not private equity. Grandpa built it from the ground up. His children grew up watching him work and decided they wanted a different life. Now, grandpa is 72 and has nobody to hand the keys to.

That’s the supply side of this story.

CEO Daryl Lockyer spent 30 years in the funeral industry. He built 17 homes himself before taking Rumbu public via a reverse takeover in late 2023. When he calls a family owner about selling, they know he’s one of them. His pitch is easy: keep your name on the door, keep your staff, take your cheque, and go enjoy retirement.

The business model is simple math. Rumbu buys these homes at 3–6× EBITDA. It trades publicly at 8–10× EBITDA. That difference is where the money is. Every acquisition is theoretically accretive on day one.

And Rumbu has a tailwind. Statistics Canada projects 40% more deaths per year by 2040 as the baby boomers age.

This playbook has worked in Canada before. Park Lawn Corporation ran this exact roll-up and eventually got acquired by a US firm at a meaningful premium ($1.2 billion; it owned 170 funeral homes). Western Canada alone has roughly 300 independent homes still available. Rumbu has six. The runway is long.

Current Status (in the WATCHLIST). The road is clear. But the execution is early.

Run-rate revenue is around C$7M. Operating cash flow margin sits at 12% (well below their 20–26% targets). A full management team, TSXV listing costs, and audit fees are being spread across only six locations, which explains the difference. Those costs don’t scale with funeral volumes. If they reach 12–15 locations, the same overhead becomes a fraction of revenue. The business would start funding its own growth. But right now, every new acquisition still leans on the BMO credit facility (C$9.96M, roughly 40% still unused), and net leverage sits at 4.5× EBITDA, which is elevated for a company this size.

Although they wanted to grow purely on debt, Rumbu announced a C$2M equity raise in early 2026 at C$1.00/share. The reason: They needed to satisfy bank covenants and unlock the next deal. The placement got delayed because the stock had slid below C$1. Nobody wants to subscribe at C$1.00 when the stock trades below it. So the next acquisition is on hold. The flywheel isn’t spinning yet.

The business model is sound: Make sure you have the cash to reach a certain scale, so that margins increase, more operational cash can be used for growth, and debt can be repaid. Grow to 170 funeral homes, and get bought by private equity like Park Lawn in the past.

What I like: Zero analyst coverage. Average daily volume is around 17,000 shares, so pretty illiquid.

So the question becomes: Is this an opportunity or not?

I see two possible outcomes:

The raise closes. Rumbu gets back to 2–3 acquisitions per year and reaches 12–15 locations by 2027–2028. Their overhead shrinks as a share of revenue. Annual cash flows cross C$1.5–2M. The business starts compounding on its own. A US consolidator eyeing Canada shows up and pays a premium. Early investors do very well.

The raise stays stuck. BMO tightens covenants. Acquisitions stall at six locations. The cash flows cover debt service and not much else. No growth. No re-rating. The thesis doesn’t break, but the stock goes nowhere for years.

I like this company because the setup is easy to understand. But it’s too early for my taste. That’s why I added it to my watchlist. To track it, see how it evolves.

3. Best article of the week

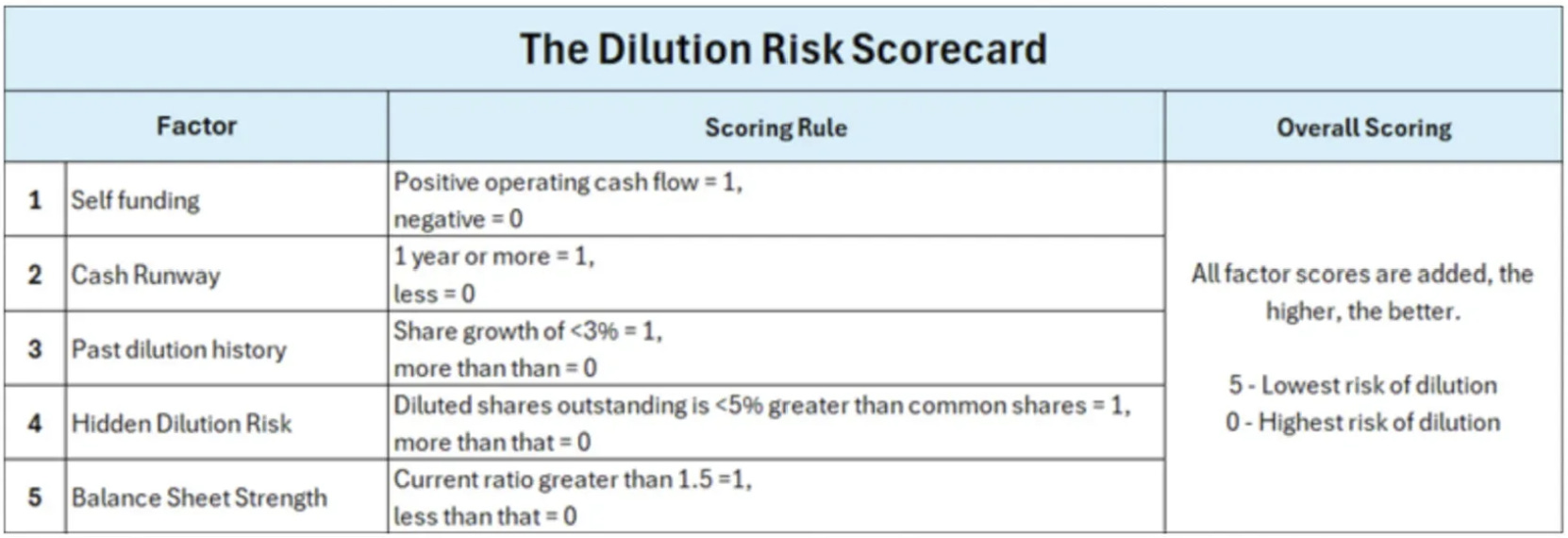

When you’re diving into small companies, as we saw with Rumbu, one thing to consider is dilution risk.

They can have a great business model and a market tailwind, but if, for some reason, they cannot get the cash to grow, you as an investor might be in trouble.

Ryan Telford introduces the dilution risk scorecard

It’s a way to assess a company’s dilution risk.

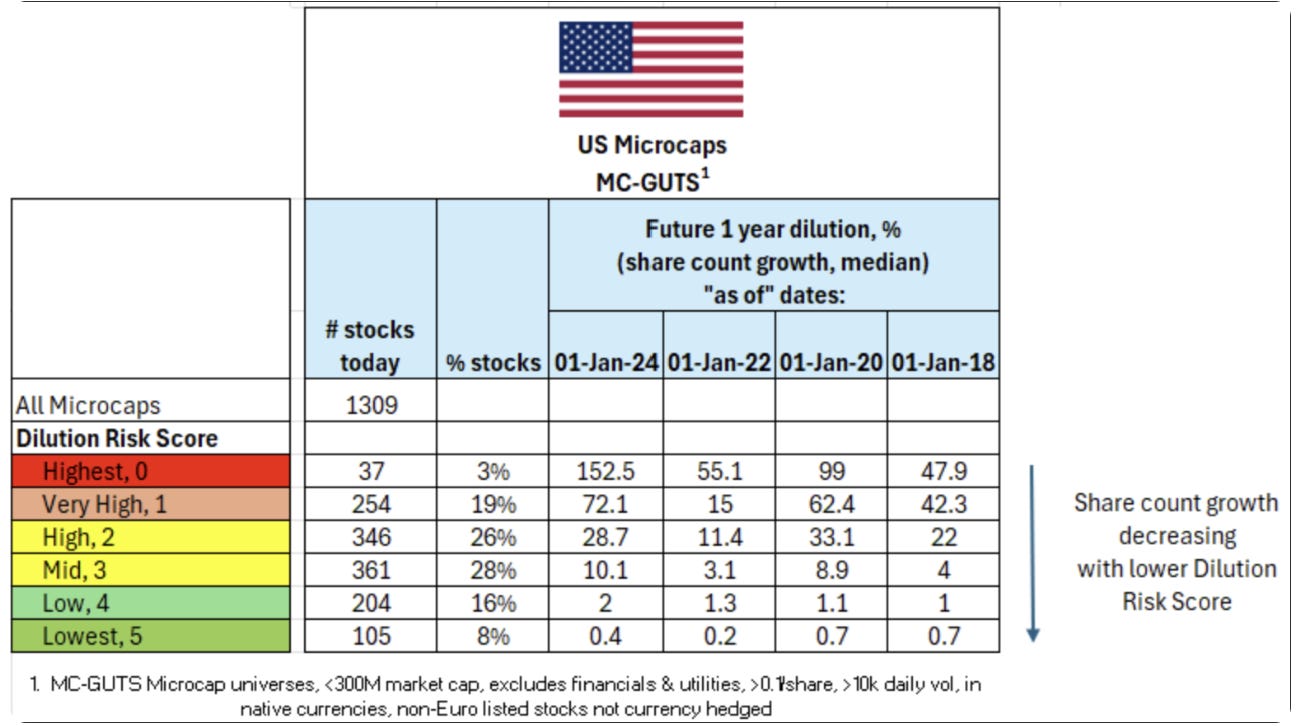

And he tested this on the US microcaps universe and got some interesting results.

Check out the full article below ⬇️

https://microcapclub.com/how-to-avoid-dilution-in-microcaps-a-dilution-risk-scorecard/

That’s it for this week.

Portfolio analysis incoming soon!

May the markets be with you, always

Kevin