From SpaceX to Einstein and how to gain an edge in investing

How to think for yourself

Are you able to think for yourself when investing?

How much of your thesis is constructed by analogy from reading other investors' work?

Can you construct your unique view of a company when all is read and done?

When you read my disclaimer, “Do your due diligence”, I’m not joking. The path to wealth is to find the ability to think for yourself. But it’s easier said than done in our current information age. When I finished college, I was not well equipped to think for myself, so our education system might be lacking on that front.

Let us explore some techniques and models that can allow us to think independently and gain an edge in investing.

Mental Techniques

What’s fascinating about people like Elon Musk, James Clear, or Michael Mauboussin?

They think in first principles: breaking a problem down into its smallest parts, into the most basic truths. In other words, they use a different way of thinking to represent reality.

One of the most famous examples is how Musk envisioned rockets. Deconstructing the base cost of all the materials that went into them, it turned out, that 98% of the cost is spent on rearranging atoms. So he figured out a way to do it differently. He almost failed though. I can keep watching that starship booster being captured by Mechazilla all day long:

Tim Urban has probably written the best article on the power of first principles thinking. The Cook and the Chef: Musk’s Secret Sauce

A cook is a trained professional who executes recipes to perfection. A chef is the one who creates the recipes and seems to have some sort of talent or creativity. But maybe the chef understands cooking into its fundamental parts, and then uses those parts to create something new, the world has never seen before.

This kind of reasoning uses a lot of brainpower. You cannot go about your daily lives thinking this way.

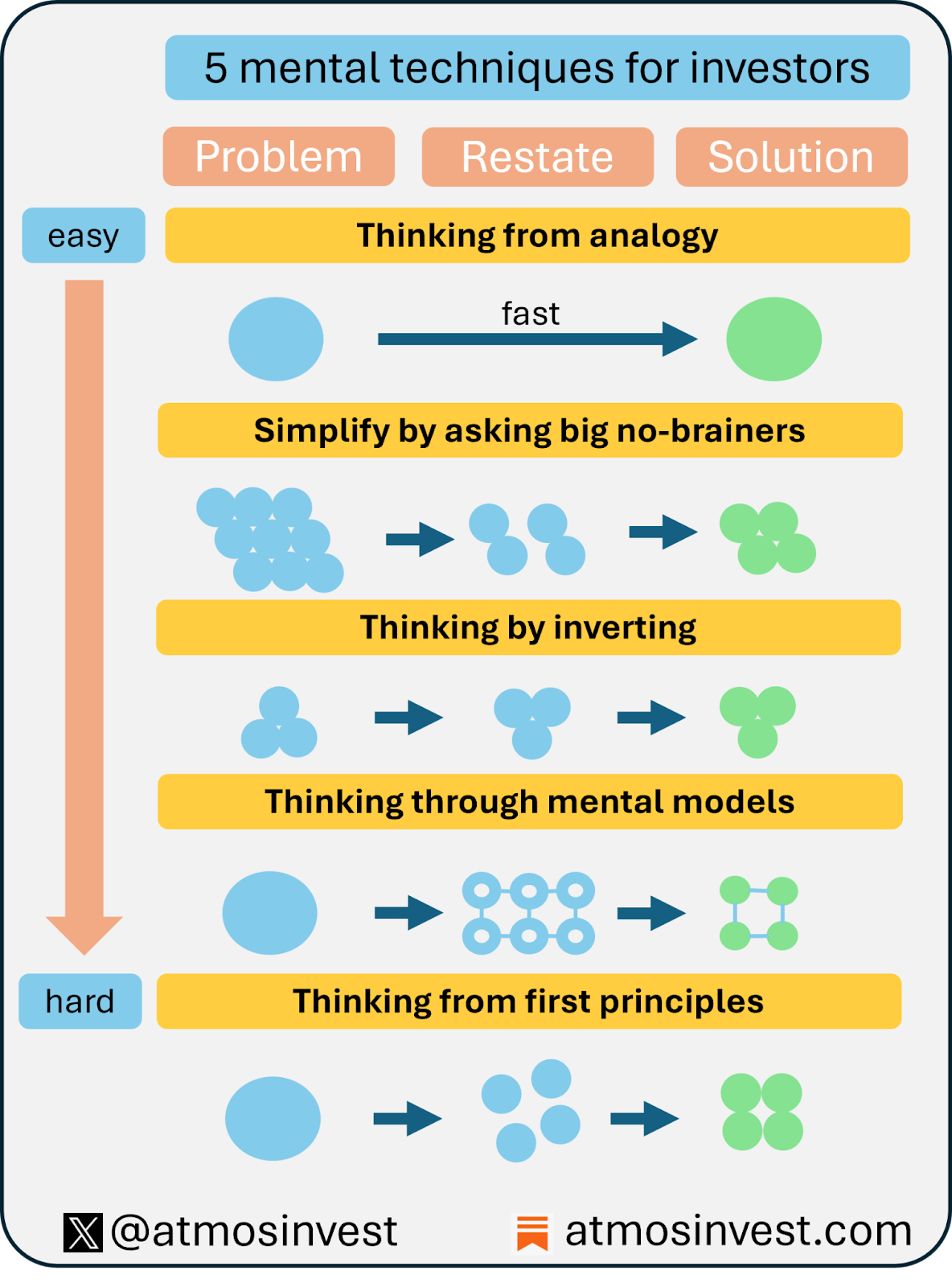

A mental technique is a way that describes HOW to reason. There are several:

Thinking from analogy

First principles thinking

Invert the problem statement

Use multidisciplinary wisdom or models

Simplify by asking big no-brainer questions

Here’s a schematic overview (click to enlarge)

The last 3 come from Charlie Munger. Thinking by inverting was touted by the German mathematician Carl Jacobi: Invert, always invert.

Munger famously used this technique during his Harvard Commencement Speech. “I cannot tell you how to be happy, but here are the things that will guarantee misery”. Or another one: “Show me all the ways I could die, so that I can avoid them.”

These mental techniques, going downward, consume more and more brainpower, getting progressively harder to use.

We’re going to focus on number 4, using different mental models.

Mental Models

A mental model has the following definition from Wikipedia

A mental model is an internal representation of external reality: that is, a way of representing reality within one's mind. Such models are hypothesized to play a major role in cognition, reasoning, and decision-making. The term for this concept was coined in 1943 by Kenneth Craik, who suggested that the mind constructs "small-scale models" of reality that it uses to anticipate events. Mental models can help shape behaviour, including approaches to solving problems and performing tasks.

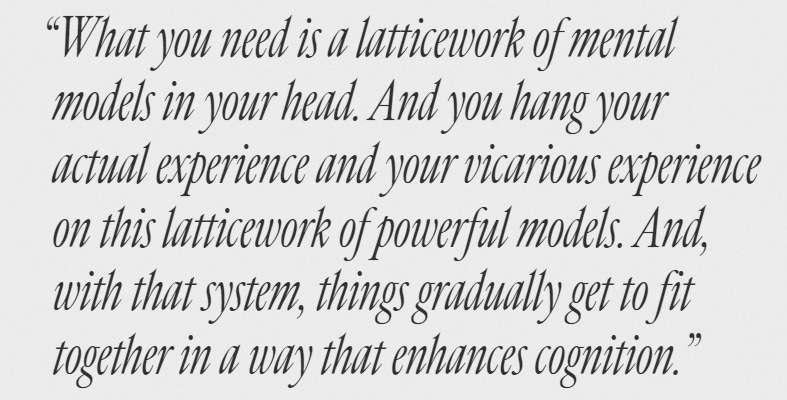

A mental model is a lens you can use to view the world around you. If you only have a few, your process for analysis is limited. Munger proposes to collect as many lenses as possible, from different disciplines, and go through them like a checklist. This might get you closer to the truth.

A mental model needs to be simple. That’s why I link them to axioms or basic premises we deem to be true. We can find them in finance, psychology, biology, math, etc.

If you want to read a business example of using mental models, read chapter 4 of Charlie Munger’s Almanack, where Charlie uses his models to analyze Coca-Cola. Charlie mentioned that nobody seemed to understand that chapter. I think of it as an example of how to reason through mental models. There is hindsight bias as he already knew what happened to Coca-Cola, but I feel it’s his way of saying that people no longer reason their way through things. Most of us think from analogy. As Charlie stated:

Every investor needs to make his/her journey. This usually means traveling from the simplest terms to making exceedingly complex models, to coming back to basics. As Mauboussin has rightly written: You need to earn the right to use the P/E multiple. You need to understand what it means.

I’ll list five mental models and show how I use them in my investing strategy.

1. An investor’s edge

Source: Finance

“Use your edge in the markets.”

- Peter Lynch

Whenever you buy a share, a person on the other side of the table is selling. You only buy when you think the price is going up. Selling can happen for different reasons, but let’s assume the person on the other end of the trade does it because he thinks the investment is going sour.

What is your edge compared to that person in this gorgeous game we play?

According to value investor Bill Miller, there are only 3 sources:

Informational: You have information the other person does not

Better process: You arrive at a superior conclusion from the same information

Behavioral edge: You are a master of your emotions and take the long-term view

If you ask any investor what their edge is, they will probably say behavioral.

And I agree. Unless you’re hunting in the realm of microcaps, behavioral, and process are all that is left.

Do you believe an informational edge still exists?

2. Shareholder returns

Source: Finance

“In the end, shareholder returns are all that matter.”

No matter how you look at any company, shareholder returns are always generated in the same manner.

EPS growth

P/E expansion

Shareholder yield

That’s why it's important to further expand this mental model and see what are the different factors that influence these 3 criteria. Mauboussin did it for us:

Shareholder yield is only related to capital allocation when there is excess cash. P/E expansion is linked to EPS growth and market expectations. Absolute EPS growth will increase value over a certain period. If EPS growth is more than expected, the multiple can increase. A multiple can increase when the business has become stronger OR if the story has attracted more investors. The first reason is more sustainable. The second one is also a sound strategy (momentum investing).

I suck at it.

3. The Compounding effect

Source: Mathematics

“Compounding is the eight-world wonder.”

- Albert Einstein

There are only 2 things to understand about compounding:

For a long time, it seems like nothing is happening

It is exponential, given enough time, in the end, the effect is massive

Let’s take a simple example: A CAGR of 15% (doubling every 5 years)

Year 5: 2X

Year 10: 4X

Year 15: 8X

Year 20: 16X

Year 25: 32X

Year 30: 64X

Year 35: 128X

So that’s a 100-bagger in 33 years. But after 10 years, your company is up 300%. Although 15% yearly is a great return, 300% over 10 years feels slow.

Waiting is hard

Waiting for 30 years is crazy hard

A business returning 15% or more over 30 years is an outlier

No wonder holding on to a 100-bagger is so rare (we didn’t even mention all the downturns on the way).

4. Scarcity

Source: Economic Theory | Psychology of Persuasion

“The first lesson of economics is scarcity: there is never enough of anything to fully satisfy all those who want it”

- Thomas Sewell

There is power hidden in small amounts. FOMO happens when demand quickly outpaces supply. Understanding the concept of scarcity is what makes a luxury brand succeed or not.

Yet it is hardly used in the investing world. Imagine a company has a limited number of shares in circulation. What will happen if the fundamentals of the company improve?

More investors will want to buy shares. But the amount is scarce. You can imagine an investor setting a limit order. The price continues to increase. His order is not fulfilled. What happens? He wants in on the action. He increases the price he is willing to pay. But others want to pay the same price. And because the supply is scarce, again, his order does not go through. The price action screams at him, and again he increases his limiter order. Finally, he buys the shares.

This is what I’ve seen happen in microcap companies with few shares outstanding that start performing. Scarcity can lead to violent price behavior.

Have you ever run a screen on the number of shares outstanding?

5. Relativity

Source: Physics

“Nothing is absolute, all is relative.”

- Albert Einstein

Just like Einstein showed that everything depends on the observer and his view of the world, the markets are also relative.

A company has a MOAT because it is doing things differently than its competitors. It’s the GAP between them that is important, not the absolute value. Look at the difference between ROIC and ROIIC. If the GAP is widening, you might have found yourself a winner, because it will become more and more difficult for the competitors to close that GAP. A company is growing in revenue, great. But how is it growing relative to the others, how is its market share changing?

But just as they haven’t figured out how to match the theory of relativity and quantum mechanics, when you go smaller, relativity becomes less important.

When looking at microcaps, you’re more focused on the absolute and less on the relative. MOATS are rare in the land of microcaps. Market share is less important.

Summary

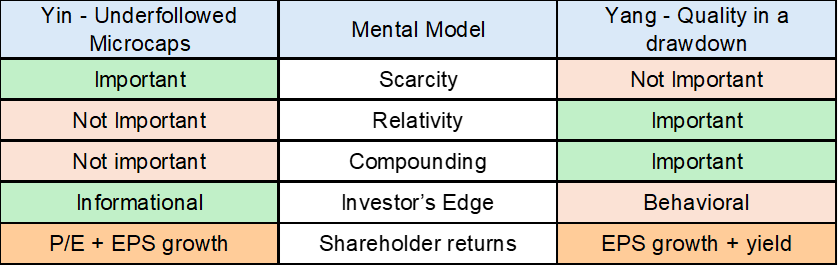

Now let’s look at these 5 mental models, and compare them with our yin-yang investing strategy.

Yin is the hunt for underfollowed illiquid microcaps. Yang is looking for a high-quality company during a temporary downturn. Here’s an overview of how the different mental models apply:

Yin - Underfollowed Microcaps

Doing an industry analysis with a full comparison of all competitors is pretty useless. You’re looking for change. An inflection. This is where the informational edge comes in. Not only is the stock illiquid, but the information flows like jelly. It’s slower. You look at float, share count, and share turnover. We’re not looking for compounders. Compounding only makes sense in a long time frame. Shareholder returns should come from a P/E expansion and EPS growth.

Yang - Quality in a down-turn

When looking at high-quality businesses, you look from a relative perspective. What is the business doing that the others are not? How does this translate into a difference in ROIC and ROIIC? Scarcity is non-existent. Compounding is important. Can it reinvest all its proceeds? If not, what is it doing with the excess cash? Shareholder returns come mainly from EPS growth and shareholder yield unless you’re buying during a market downturn. There is no informational advantage. These companies are usually well-studied by a lot of analysts. Your edge as an investor has to come from the fact that you can drive conclusions that are different (process), or that you behave counterintuitively.

The holy grail?

To find some yin with some yang or some yang with some yin.

A quality microcap operating in a niche market that shows some signs of an increasing competitive advantage

A quality compounder that you can buy at a low P/E because of some sort of a downturn that you know is only temporary

If we truly want to think for ourselves, our goal should be to collect as many mental techniques and mental models and use them as a checklist. This might allow us to look at certain investment cases differently than other investors do and gain an edge.

What other mental techniques and models do you use?

May the markets be with you, always!

Kevin

Patience is super important, the finance industry is based around action

Great breakdown of mental models! Your points on behavioral edge and looking at companies from multiple angles match my NASDUCK approach. This type of thinking is exactly what separates the pros from the amateurs in today's market.