Power scarcity creates massive tailwinds

Business update NUAI

Yesterday, NUAI gave a business update.

Find our initial thesis on NUAI here.

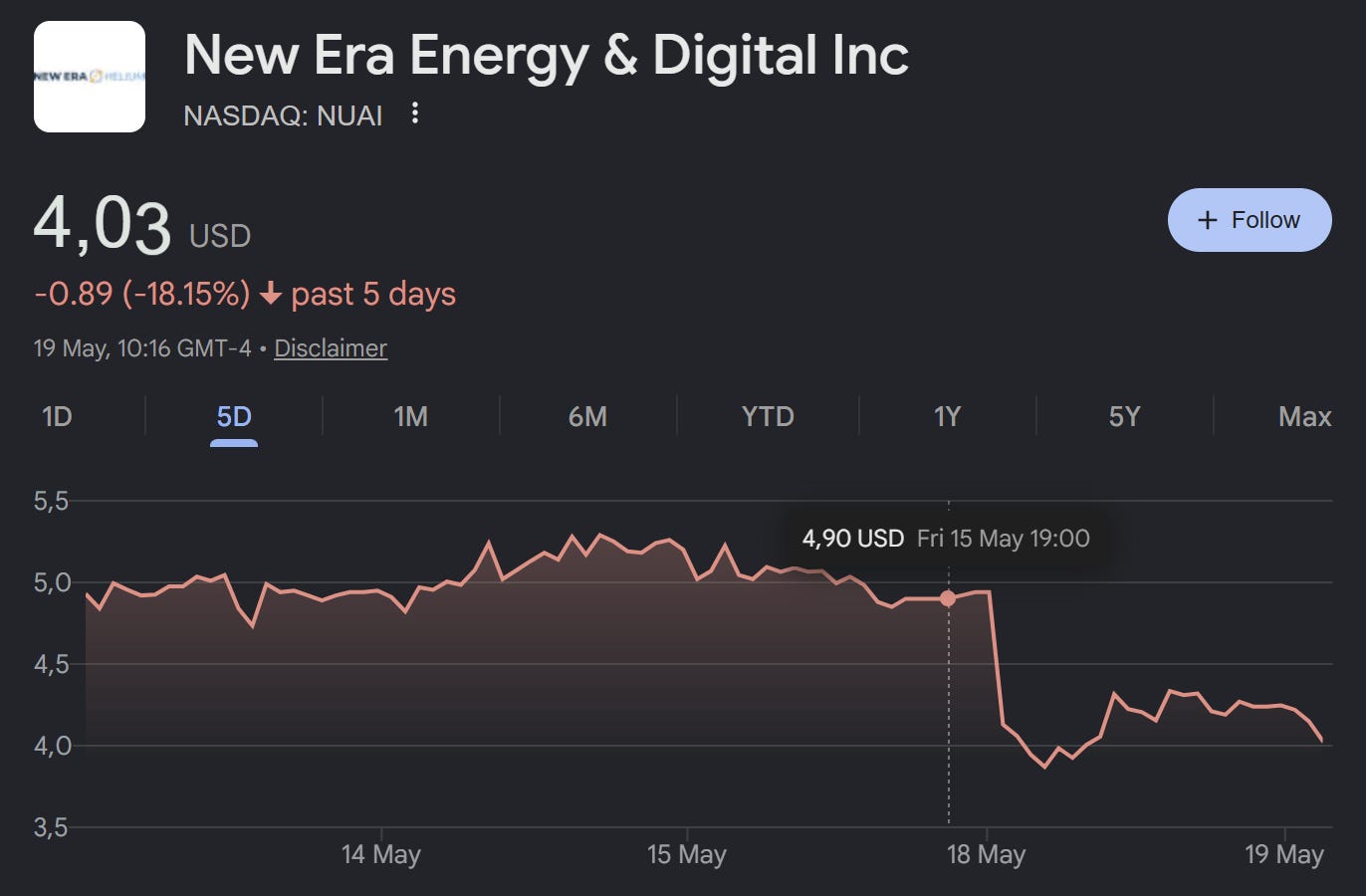

Price action was wild:

But we know this was going to be a bumpy ride.

A speculative bet, in a speculative stock.

So I ran my tracker agent to read the transcript and go through the business update. Then it compares this new information to our initial thesis.

It concluded: Thesis intact.

I then got the report and analyzed it.

Here’s what matters:

The good

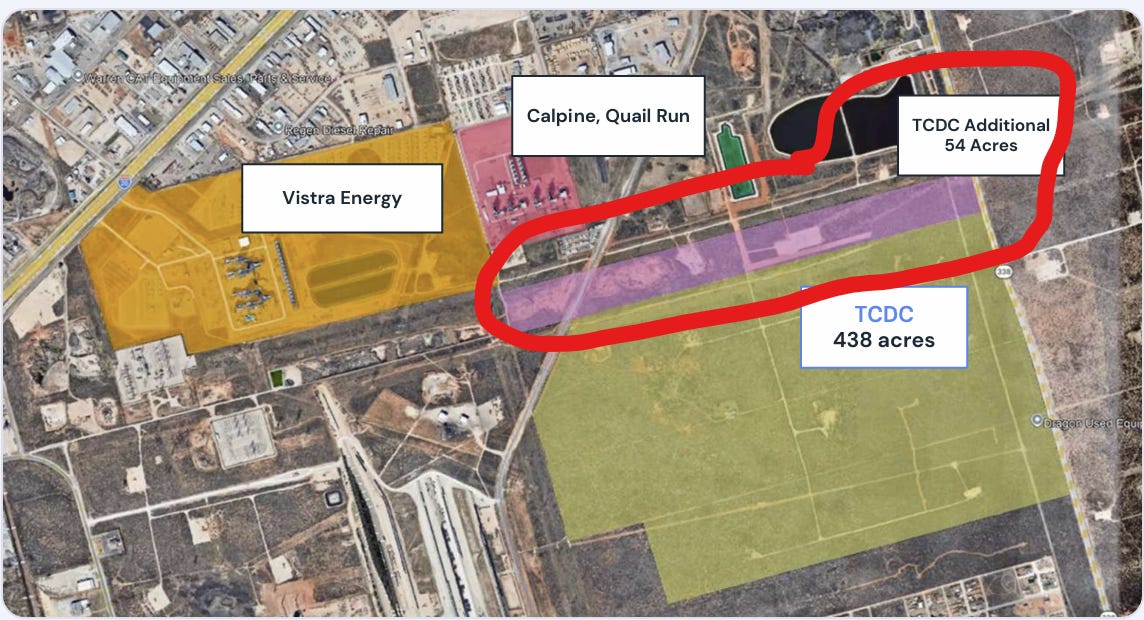

54 acres of land

They entered into a binding agreement on the 54 acres of additional land they wanted to purchase. That doesn’t mean the deal is closed, but it’s on its way.

We flagged it as a “kill condition” in our thesis because, based on our understanding, it was an explicit demand from their hyperscaler client.

So this is a big milestone in the development of this project.

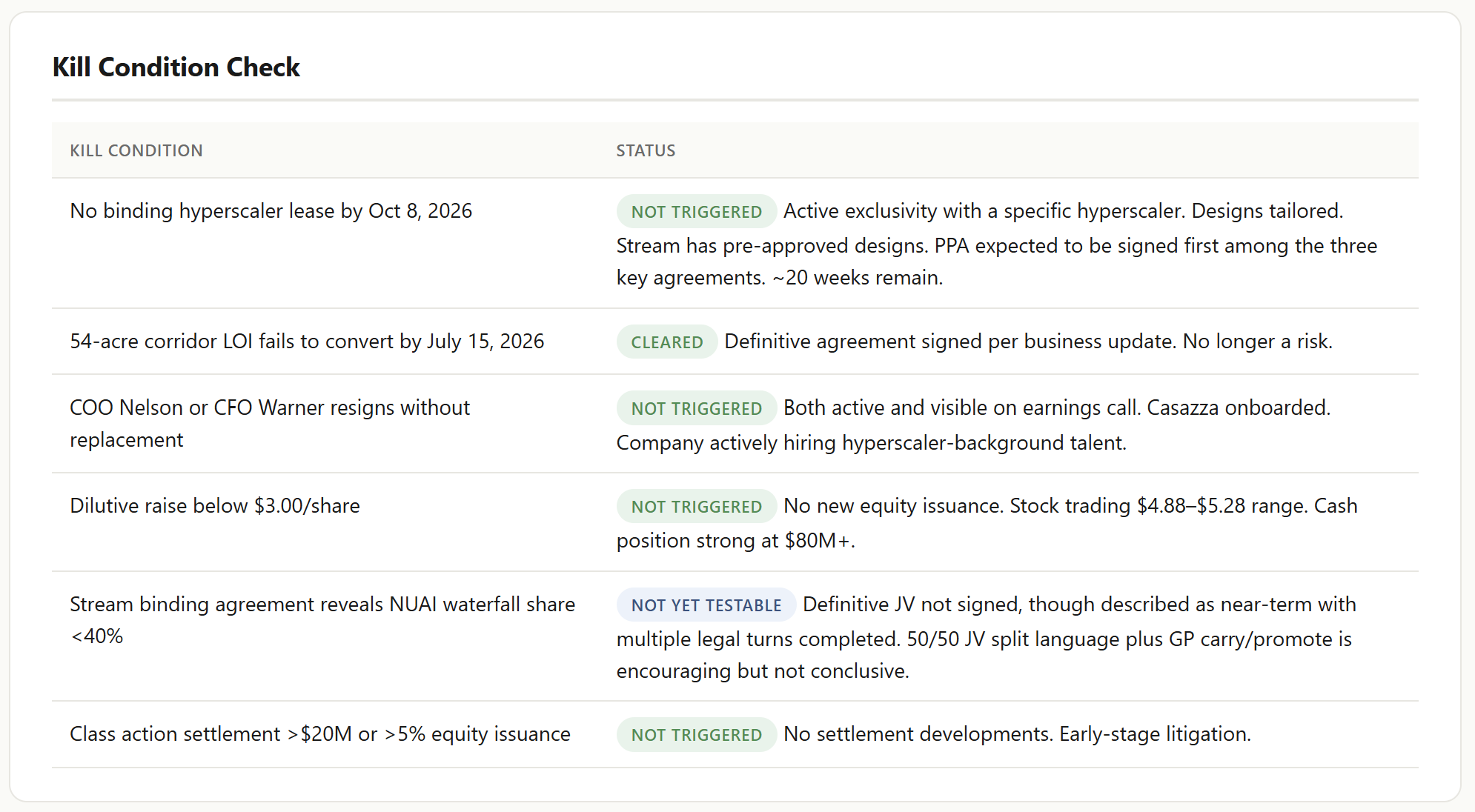

And just to show you how our tracker surfaces the kill conditions, it looks like this:

All other kill conditions remain on the table.

This company is a free sample. If you want to continue receiving these kinds of articles + deep dives and everything else, please consider taking a subscription.

Phase 1: bypassing the ERCOT queue

This was already hinted at in a previous update. Their first 200 MW is not a behind-the-meter solution. That means they need a grid connection, but they remain vague on how this will be implemented: By using existing infrastructure.

This is an assumption, but the only way they can pull this off, and effectively bypass the ERCOT queue for grid interconnection:

Negotiate a power purchase agreement with Vistra or Calpine plants

Because they are adjacent: They can probably connect to an existing substation (and not directly into the grid)

The 54-acre corridor allows them to build this connection

No new power means no air permits needed for phase 1.

This makes everything a lot simpler.

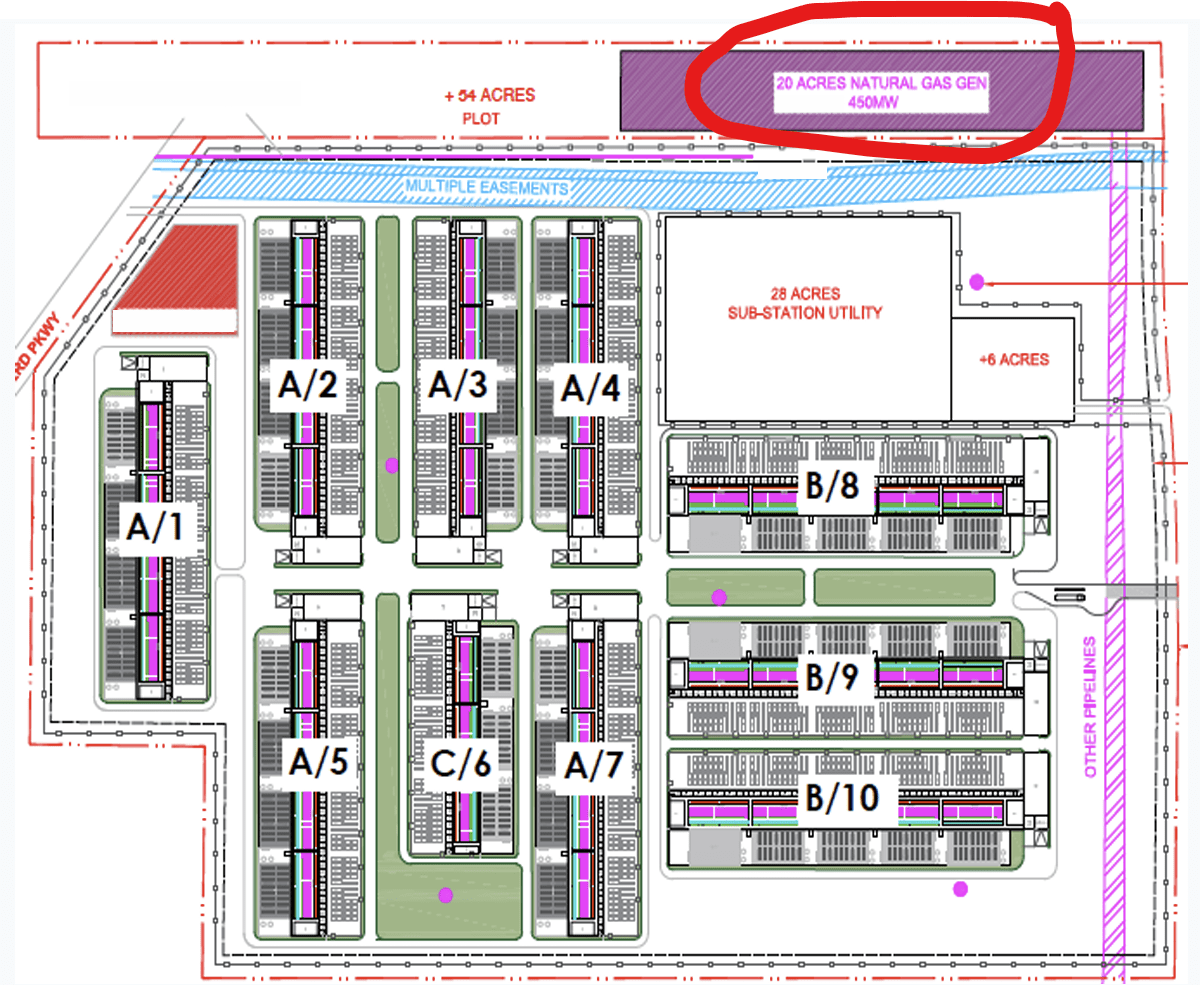

Phase 2: 450 MW

They showed an updated picture of what the Texas data center would look like, and you immediately see what they plan to do with half of the new land they are acquiring:

It’s where the Behind-The-Meter power generation will come in.

Cash burn is manageable

Cash sits at >$80M as of April 30, confirmed on the earnings call. SharonAI note is fully prepaid.

Burn rate sits at $7 to 8M/quarter. The current runway extends well past the Oct 8 deadline (the loan covenant). Management states that current liquidity is sufficient for NUAI's phase one equity share without material near-term dilution.

Sharon AI: No problem

During the Sharon AI earnings call, they implied that the hyperscaler had walked away from the deal with NUAI.

The rebuttal from the CEO:

"I can't speak for Sharon directly on why they chose to word the paragraph the way they did, but I can say that I don't blame investors for being confused… we put out a press release on July 1st of 2025… This group [the LOI counterparty] was not considered a hyperscaler and I don't think they would be today… that LOI was not related to a lease and it wasn't with a hyperscaler. It was related to a sale and us hopefully providing some behind the meter power."

This is a thing from the past, and it was not the “hyperscaler deal”.

Sharon AI is now fully off the cap table. (paid back in cash).

Moving along.

The bad

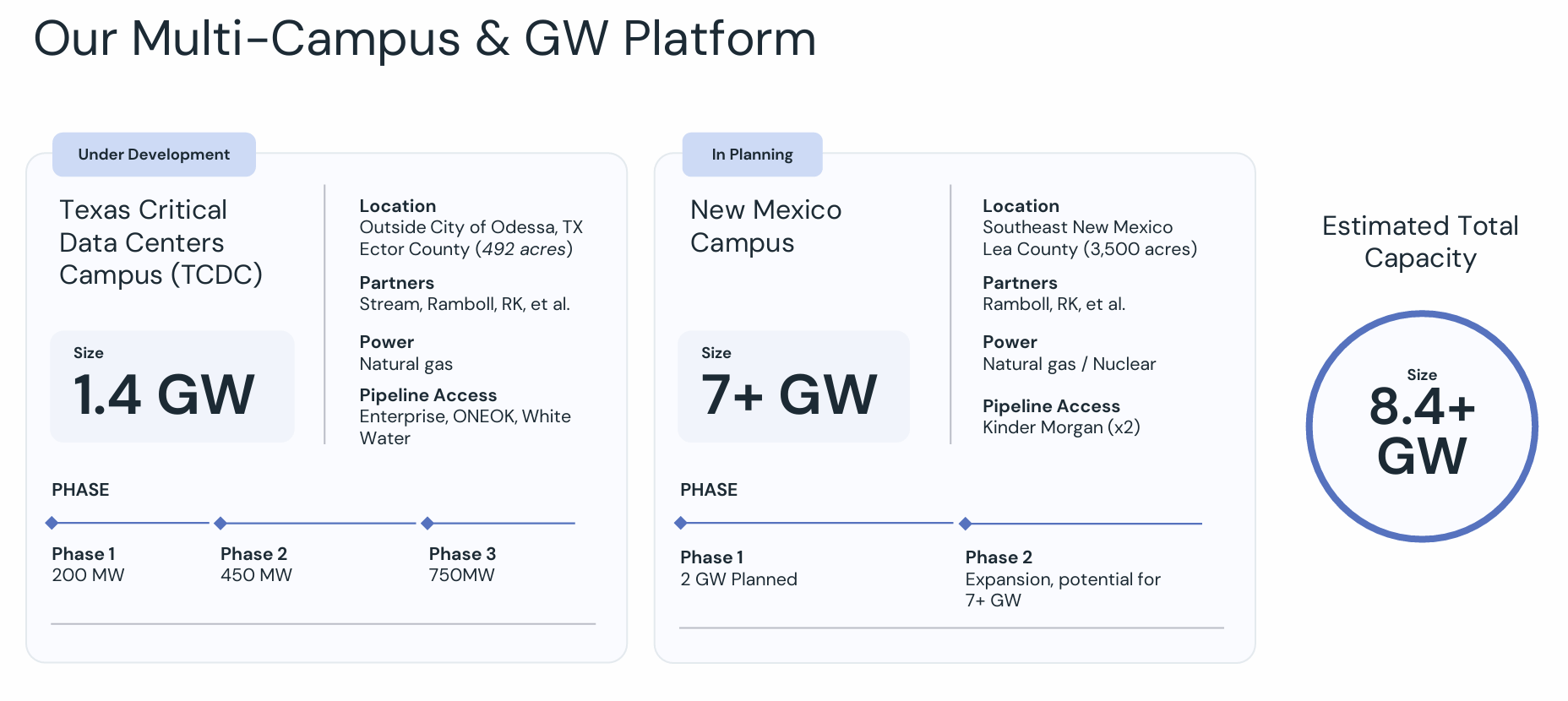

Well, it’s not exactly bad. But the company keeps talking about “building a platform” and now building an 8.4 GW total campus.

And I admit, they did refrain from showing the atom, modular design in this recent business update.

I get it. Big Hairy Audacious Goals. (BHAG)

But in business, the saying is: Sell 1 dollar first. Then sell some more.

Sell that 200 MW first. Then sell some more.

Now, if you compare NUAI to other companies like IREN, APLD, etc., and assume they can actually reach that number, on a pure peer-to-peer comparison, you would be looking at a stock price between $50 and $100. (I considered a 17% of the total platform value because of their GP/LP structure).

The future

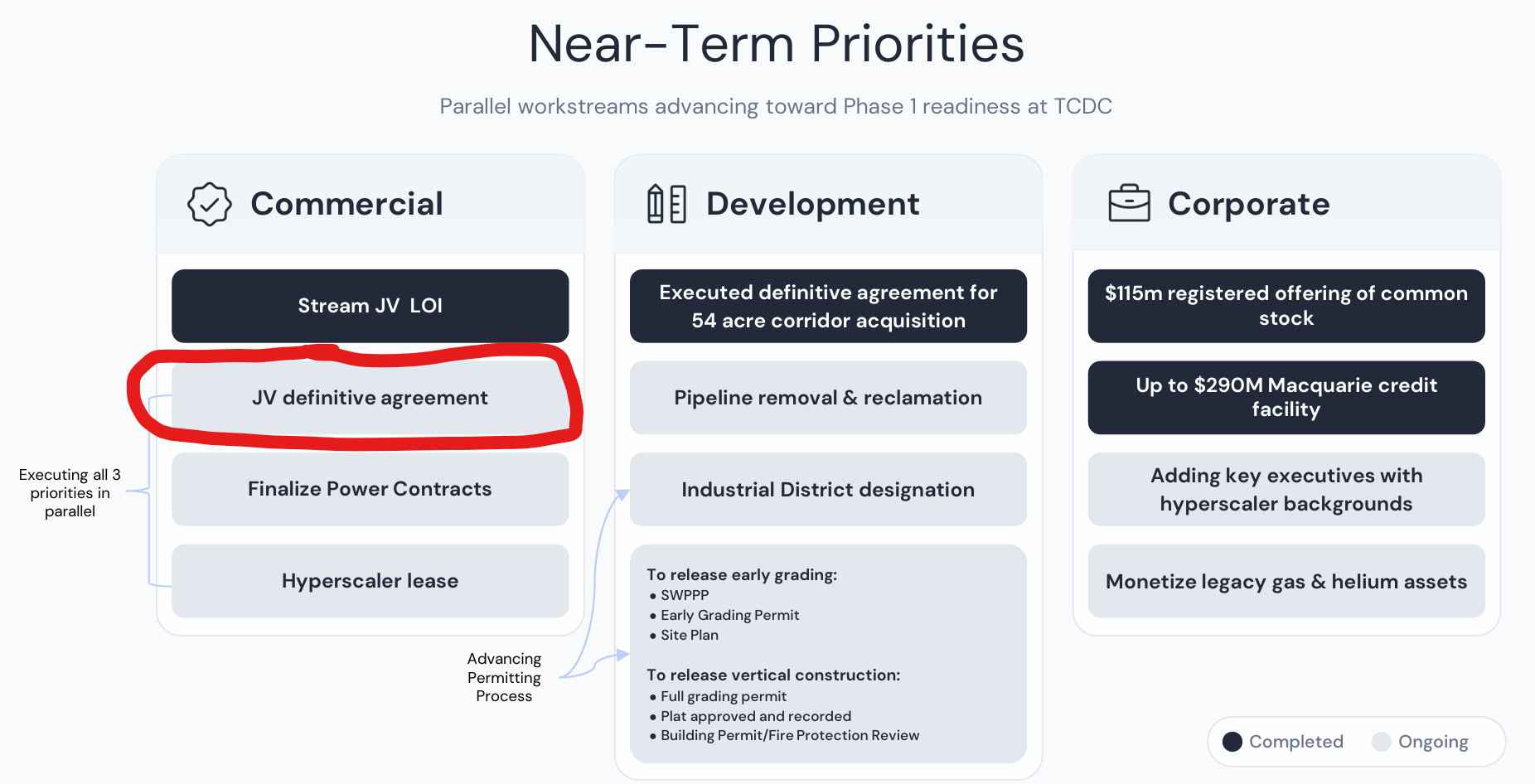

The most important task at the moment is to finalize the Joint Venture Agreement with Stream.

Why?

Here’s part of the transcript with Charlie Nelson, who was leading the business update:

“We were also getting offers to buy this from actual hyperscalers. And one of those we did sign an exclusivity agreement because we kept turning them down on selling. And we wanted to work with them on how we can partner with you to own something here. And essentially, it was you’ve got to work with a really reputable developer. We went and tried to find one. And that exact same party, as we said before, sort of led us to a different party. And now here we are with that party stream. They’ve been incredible to work with, just every day checking boxes…

And the same party, that hyperscaler is still the person that we hope will be our tenant that our designs are specifically for.“

This means that:

A hyperscaler wanted to buy the land in Texas, but NUAI refused

They agreed to maybe partner up, but only on 1 condition: they had to bring in Stream

That means a final contract with Stream is key to signing on the hyperscaler.

Here’s their slide:

It’s true that they are working on all three in parallel, but the thesis now becomes clearer:

Agree on the final joint venture with Stream

Get those power purchase agreements for 200 MW

The hyperscaler can come on board for phase 1.

The market is hungry for compute

I bought into NUAI because I believe powerful forces are at work, creating unique scarcity in the market.

Companies are hungry for tokens

But token prices are rising because of the lack of compute

More computing needs mean more power requirements

If NUAI can pull it off, it would be an incredible feat. This is startup land governed by experienced executives.

So my read of the current developments is positive.

But make no mistake. This is still a speculative play.

The downside risk decreases with each passing month. But if that hyperscaler does not sign, this company will be dead in the water.

You’ll receive an update on all the other positions in the coming week.

May the markets be with you, always

Kevin

I was thinking of approaching the stock this way. Once the news of a contract with a hyperscaler is announced, I will buy some shares. Yes, this means that I will miss out on some of the returns as the share price will have jumped immediately. However, I can’t believe the value will be priced in completely from the initial price jump. Any insights on this approach?