The 15 best stock pitches from Omaha

Part 1/3

I heard over 50 pitches in Omaha.

I made a selection of the 15 I consider to be the best.

Since I want to provide you with a first analysis, the 15 best pitches will be split into 3 parts, as otherwise this article would become way too long.

Each company will have:

A short description of what they do

The type of company they are

The pitch

I’ll need to do more due diligence on several of these names, but I think it’s worth getting them to you as quickly as possible. (After all, I did have 2 stocks go up over 100% while sitting in my research pipeline. So I do plan to publish ideas more quickly, so you might benefit from them.

I pitched our last deep dive, which had a great quarter and is up 20% since March.

If you hesitated about taking a paid subscription, we’re running a special Omaha sale for the next week. You’ll get 25% off an annual subscription. Prices of the annual subscription will go up permanently after the sale. This is your chance to lock in the current rate.

Now let’s look at the first 5 stocks. The best ones are at the end of the article.

5 AMCORI Group (AMCO on AIM in the UK)

Description: Amcom buys small, boring British engineering companies from retiring owners, makes them run better, then bolts more of them together.

Imagine a 68-year-old guy in Sheffield who runs a valve repair shop. He started it in 1987. Forty employees. Nice profits. His customers are power stations and oil refineries, and they’ve been buying from him for 30 years. He wants to retire, but his kids don’t want the business. He’s too small for private equity. Selling to a competitor would gut his loyal team. He’s stuck.

That’s the seller Amcomri targets.

Type: Tiny serial acquirer

The pitch: They have a long runway to reinvest capital profitably (the ability to buy small, family-owned businesses with little competition at less than 5x EBITDA). They have a very experienced management team with deep operational and deal-structuring expertise. The underlying businesses are resilient and mission-critical (high recurring revenue, low customer-concentration risk, less susceptible to AI disruption).

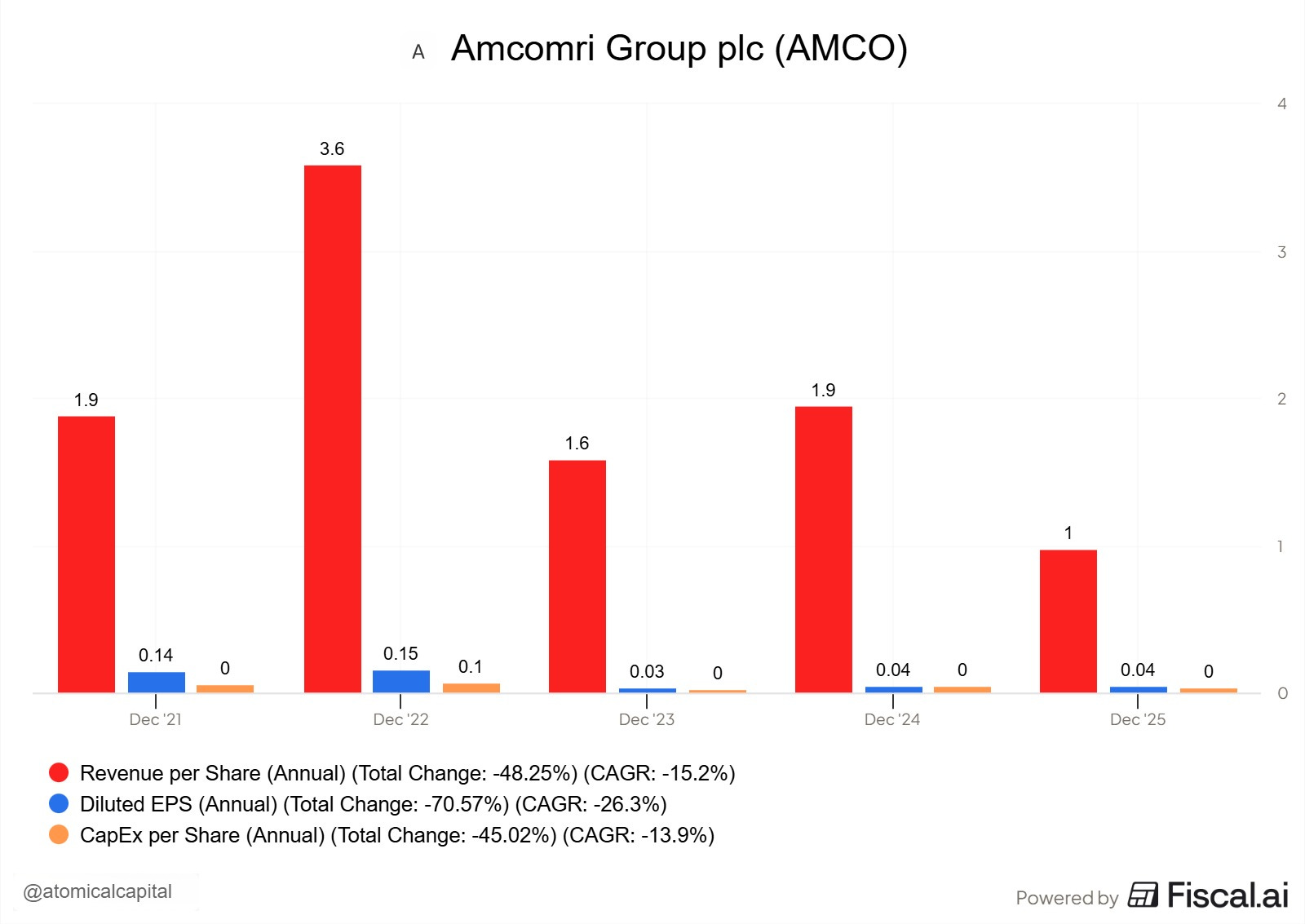

Now, fiscal has a great feature that shows revenue per share along with earnings per share.

Which means, as you can see, despite overall revenue growing, revenue per share dropped, indicating they issued capital to finance acquisitions.

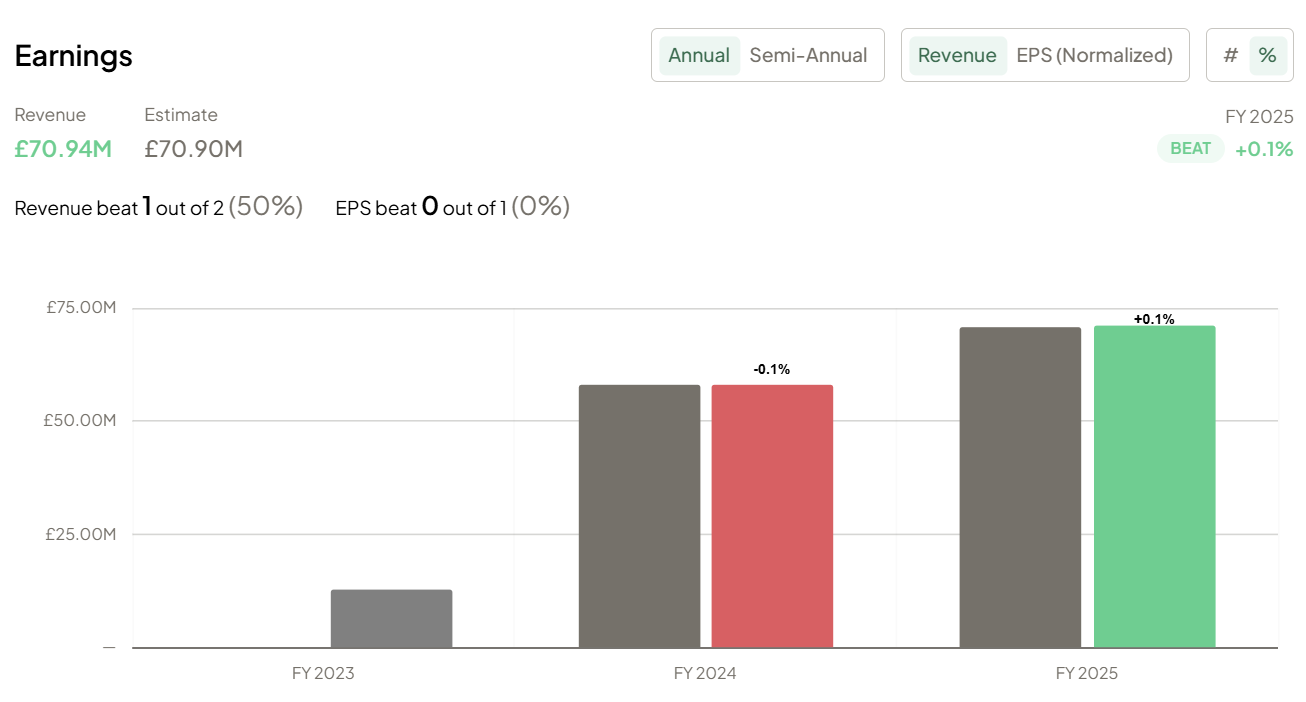

Fiscal.ai has a revenue and earnings beats/misses view now. We’ll use that for each company. If you’re interested in a 25% discount on a fiscal.ai subscription, they are running a sale at the moment.

Here’s what it looks like for AMCO.

I think this could be an interesting idea. But I would need to dig a lot deeper.

The price of the stock has seen only strength, which I like a lot:

The bet for this company would be:

The founders keep finding deals at 4-6x EBITDA over the next 5-10 years

Their own equity multiple stays at 9-10x or rerates higher

They avoid blowing up an integration

The UK SME succession wave keeps producing supply

They eventually scale to £30-50 million EBITDA, at which point institutional money piles in and rerates the stock

So, despite the long runway, the only potential problem is that a lot has already been priced in.

Now let’s go from a microcap to a bigger company.

4 Primoris (PRIM on NYSE)

Description: Primoris is the company that physically builds and maintains the boring but essential infrastructure that keeps America running. The high-voltage line, the gas main, the solar farm out past the highway, the long-distance oil pipeline crossing Texas. None of that installs itself.

They are a specialty contractor: they don’t own the wires or pipelines, they get hired to put them in the ground and keep them working by utilities, oil and gas operators, solar developers, and state highway departments.

The business splits into three buckets.

Utilities is the steady recurring half (gas, electric, and telecom distribution, mostly under long-term Master Service Agreements).

Energy/Renewables is the growth half (utility-scale solar, battery storage, refinery work, and highway projects for state DOTs).

Pipeline Services is the legacy half going back to the company’s 1960 roots as a California pipeline outfit (big oil and gas trunk lines, pump and compressor stations).

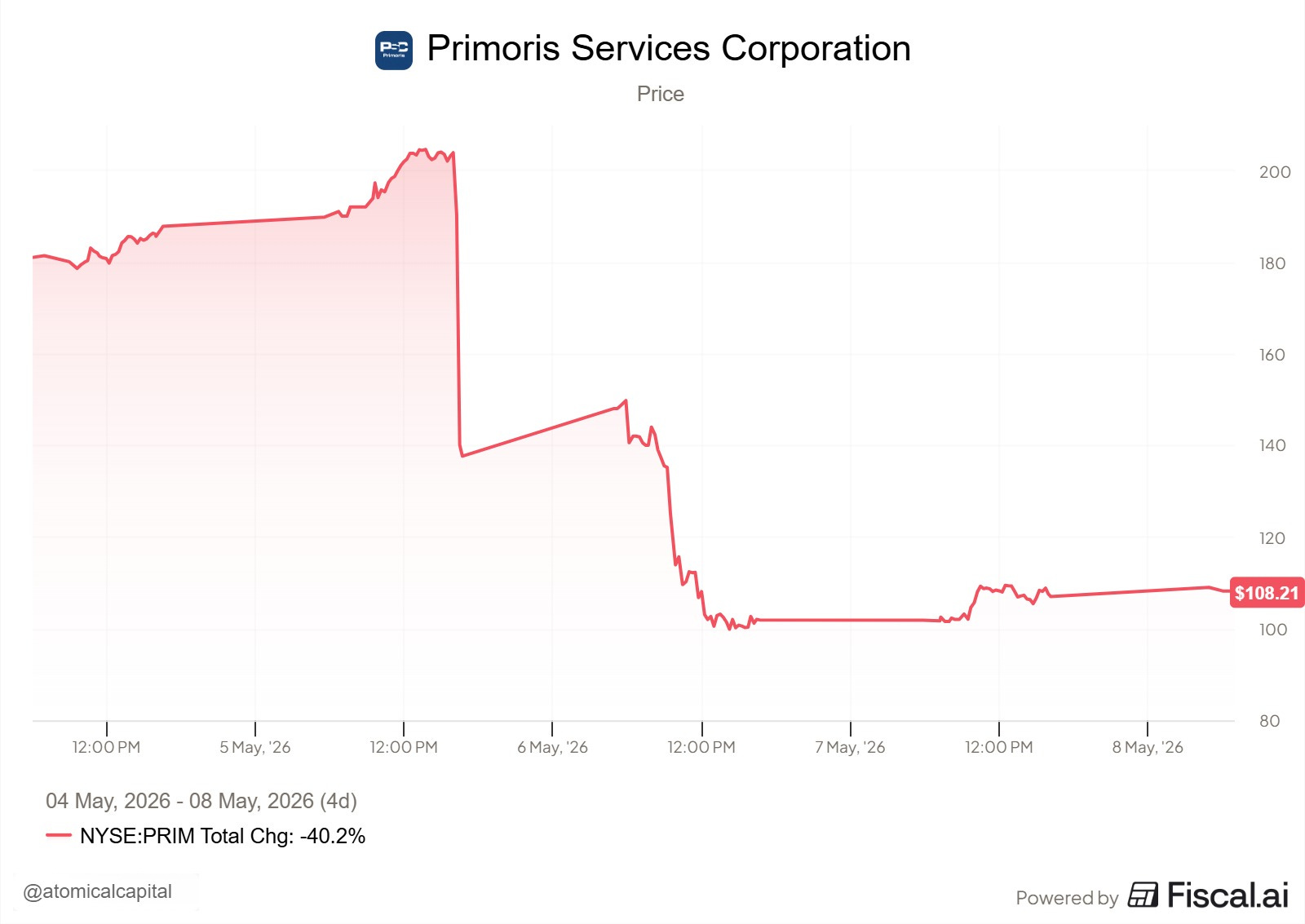

Although it’s a bit big for my taste, with a market cap of almost 6B USD, I wanted to take a look at this as a data center infrastructure play. And since the company missed its quarterly estimates, the stock dropped 40%.

I mean, it went from a 12B USD market cap to 5.8 in a matter of days…

Now, before jumping into this stock, it did trade at a forward P/E of 38 before the drop, which is staggering for an infrastructure services company. They missed their renewables segment and had to cut their year-end guidance.

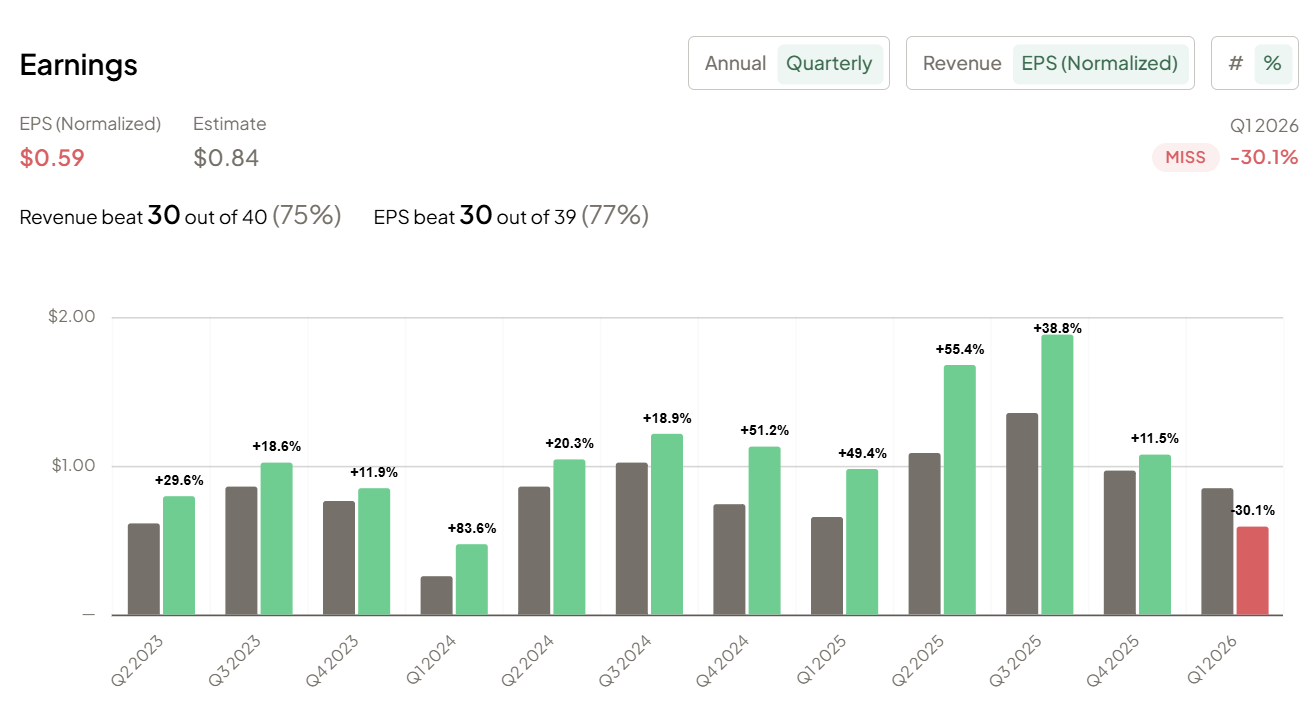

And we’ll need to dig, but it has almost always beaten expectations.

Now, what’s great about these kinds of companies is that their backlog gives us some visibility into the future.

From their latest report:

About 5.2 billion of that management states should be converted into revenue over the next 12 months, which sets a floor for upcoming revenue. (The Master Service Agreement part) (compared to 7.6 billion in revenue in 2025).

The pitch: The infrastructure supercycle is driving massive spending in the utilities and energy sectors; Primoris has an enormous backlog. There is a significant uptick in energy prices, datacenter construction, and electric utility projects. Their proximity to Texas energy companies and long-term relationships with utilities.

So the final question for this company is: Is their renewables setback a one-off? If so, and they resume growth in 2027, you could buy this company at an attractive price.

Based on the new guidance from management, the stock is trading at a forward P/E of 24.

3 Lesaka Technologies (LSAK on Nasdaq)

Description: Lesaka is a South African fintech for people and small businesses that regular banks ignore. In townships across Southern Africa, most commerce happens in spaza shops, taverns, and gas stations. The owners and their customers mostly never had bank accounts. They live on cash. Cash gets stolen and can’t be tracked, so no bank will lend to them. Lesaka fills that gap from both sides.

For shop owners, it installs card terminals, sells software to run the business, and lends working capital based on the cash flowing through the till.

For consumers, it offers a bank account, small loans, and affordable insurance, such as funeral cover.

Lesaka earns a cut on every card swipe, interest on every loan, a premium on every policy, and a margin on every prepaid airtime and electricity top-up.

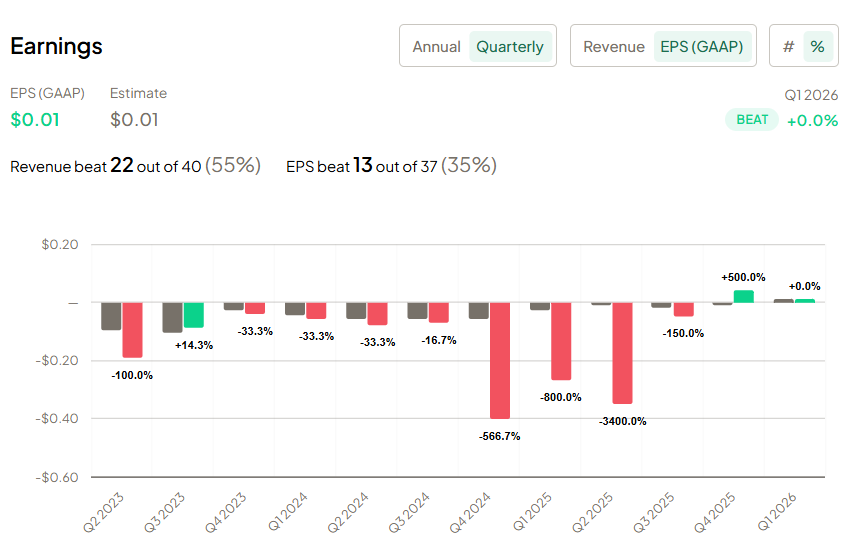

Previous earnings and revenue beats/misses from fiscal.ai.

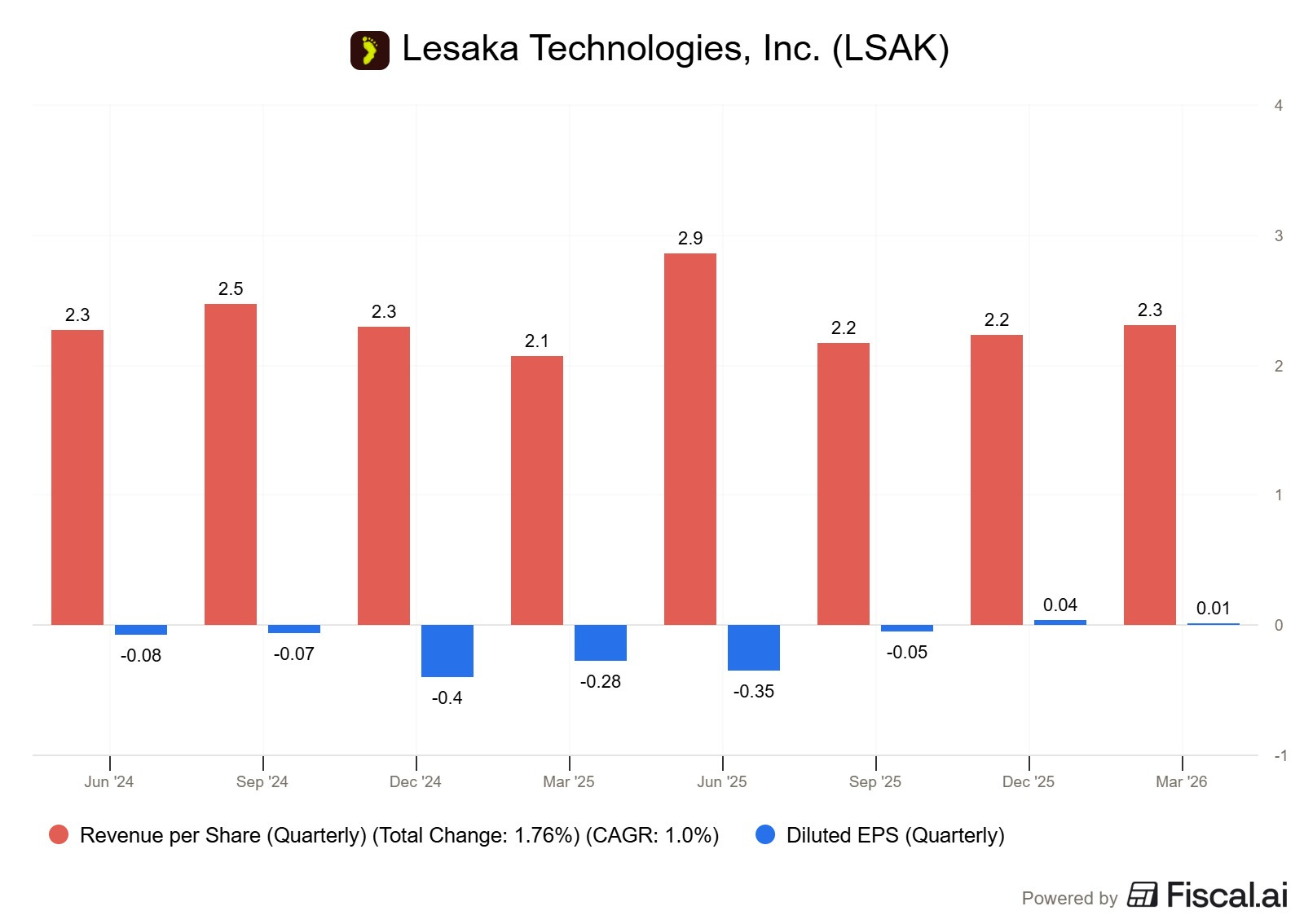

And revenue and earnings per share per quarter (as this company had to raise capital to acquire other companies)

Type: Fast grower. Inflected Earnings.Consolidator.

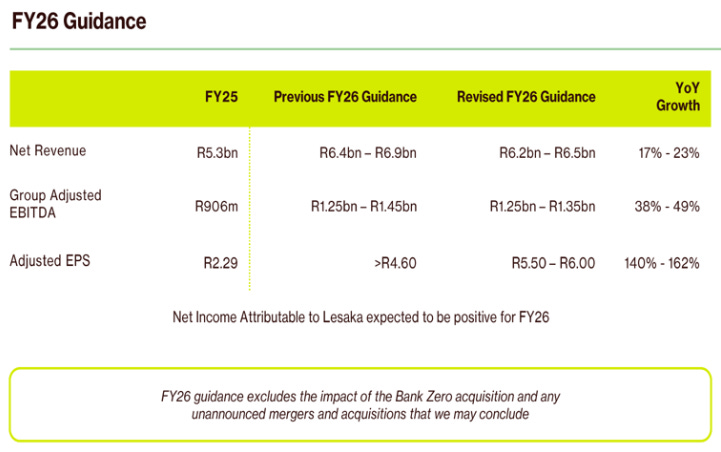

The pitch: Lesaka is a Fintech displacing cash transactions in South Africa, serving the underbanked with high incremental margins. It just shifted to positive earnings based on their earnings report on the 7th of May. Based on expected earnings in 2027, it sits at a forward P/E ratio of 14, which is lower than that of emerging-market peers.

However, this forward P/E is based on non-GAAP EPS numbers (see figure below). Because Lesaka has made several acquisitions, amortization is not included.

3 forces working together could make this an interesting setup:

The amortization will naturally increase GAAP EPS over time (but management must refrain from another big acquisition). But the business is framed as a consolidator, so they will keep acquiring companies.

The company’s market cap is still small. As the market cap increases, Emerging Markets funds can come in, and this will have a positive impact on the multiple

The business growth itself, where management guides towards 30% operating margins (from the current 21%)

Final note: The local devaluation of the currency (the ZAR) will reduce the final ROI, but if the management base case holds, it should be more than offset by the company’s growth.

Now we get to the best. The ones I regard as the highest potentials for multibagger returns.

If you want full access, consider the current 25% discount to continue reading.

Let’s dive in: