3Y Sales CAGR of 48%: Code Cracked

Earnings Update Q2 2025

I-TECH AB is a small Swedish manufacturer of a compound called Selektope. This compound is used in paints on ship hulls. It helps repel the accumulation of barnacles on the hull. This leads to increased fuel efficiency and less labor to remove the barnacles.

I-TECH has seen solid growth over the last few years.

You can find the full deep dive here.

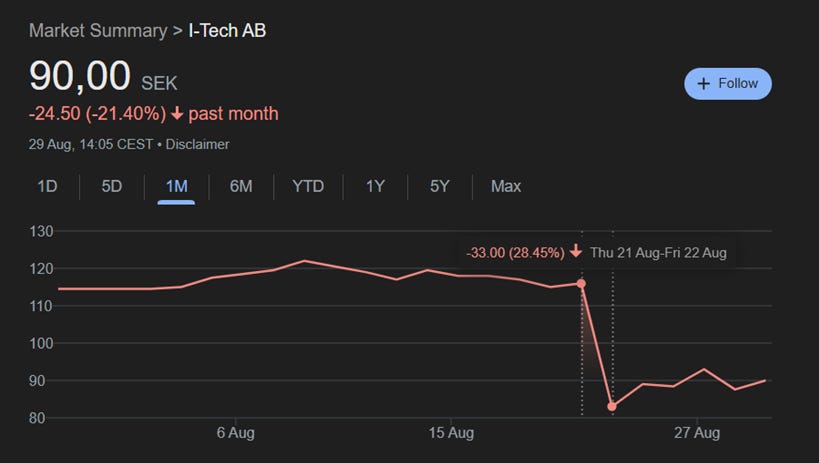

However, over the last quarter, they announced a decline of 26% in sales.

The market reacted:

The cause:

One of their biggest customer stocked up on inventory in the previous quarter, with less intake in the last quarter

Another customer faced financial constraints, which could limit their uptake in 2025 versus 2024

Uptake will vary from quarter to quarter, management has warned about this in the past. Previous quarters were unusually strong

The 26% decline also suffered from currency effects. In USD, the decline was 17%

New sales are up 9% YTD, but when compared to the previous quarters, it does not look great. Here’s the full explanation by the CEO:

The relatively weak sales in Q2 is the result of natural quarterly variation and exceptionally strong sales in Q4 2024 and Q1 2025, further amplified by currency headwinds. Year-to-date sales by the end of June 2025 have grown 9% year-on-year in SEK and 14% in nominal currency. CMP recorded a sales growth of 7% in nominal currency during H1 and released a positive report for the first quarter in their fiscal year. Customers other than CMP have increased their combined volume by 40% during the first half of 2025.

Source: Q2 earnings release

And global coatings giant PPG dramatically ramped up usage of I-Tech’s anti-fouling agent, with a +172% year-to-date increase in offtake – a strong endorsement from a key industry player.

And what about the other numbers besides sales?

Gross margins actually improved a bit

But operating profits took a 50% decline

The biggest risk remains their dependence on a limited number of big customers. That means if the “Financial Troubles” continue with one of their big clients, it could limit spending.

On the other hand, management has stated that they estimate to be serving about 3,000 vessels at this time, out of a global commercial fleet of 100,000 vessels.

That’s a mere 3% market penetration with a lot of room to grow.

Concerning the reregistration in Europe (low revenue risk but higher “image” risk), they seem to be on top of things. They had a meeting with the European Commissioner in charge of this:

Our team also met with the Commissioner’s Cabinet to provide specific feedback on factual errors in the ongoing Selektope re-registration case. We look forward to seeing the potential outcome of the Cabinet meeting, possibly in the next step of the process, which is the next quarterly meeting of the Standing Committee on Biocidal Products (SCPB) in September.

And when it comes to the underlying business outlook and the future:

Despite currency headwinds and market uncertainty, the business continues to develop positively. Operational excellence and business development efforts are reinforcing momentum. During Q2, the team participated in shipping exhibitions in Japan and Norway and met with shipyards and customers in Korea to strengthen relationships and advance ongoing projects. One product development initiative reached major technical milestones, and additional partnership discussions are underway.

Strengthening existing relationships

Advancing ongoing projects

A new product technical milestone that was overcome

Additional partnership discussions

When you read it like that, there are no new actual contracts that have been signed. But the new product development is important. As we outlined in the original thesis, we want to see more diversification in the products they sell. It would derisk their business model.

Now let’s get into the good stuff and why, after an exchange with Cristopher Mayer, the author of 100-baggers, I think he might be on to something… ⬇️

Capital allocation

Management decided to “reward” shareholders with a 1.75 SEK per share dividend. (ordinary + special).

I’m going to be honest. I’m not a fan of dividends.

In the 100 Bagger project, we’ll try to show if data confirms that dividends are “an expensive pastime” except for large mature companies that have no reinvestment runway at all. But they are detrimental to multibagger performance.

This was not my idea. I’ve had a discussion with Christopher Mayer on this topic, and he proposed to include it in the project.

But dividends should always be considered in their context.

And I get it.

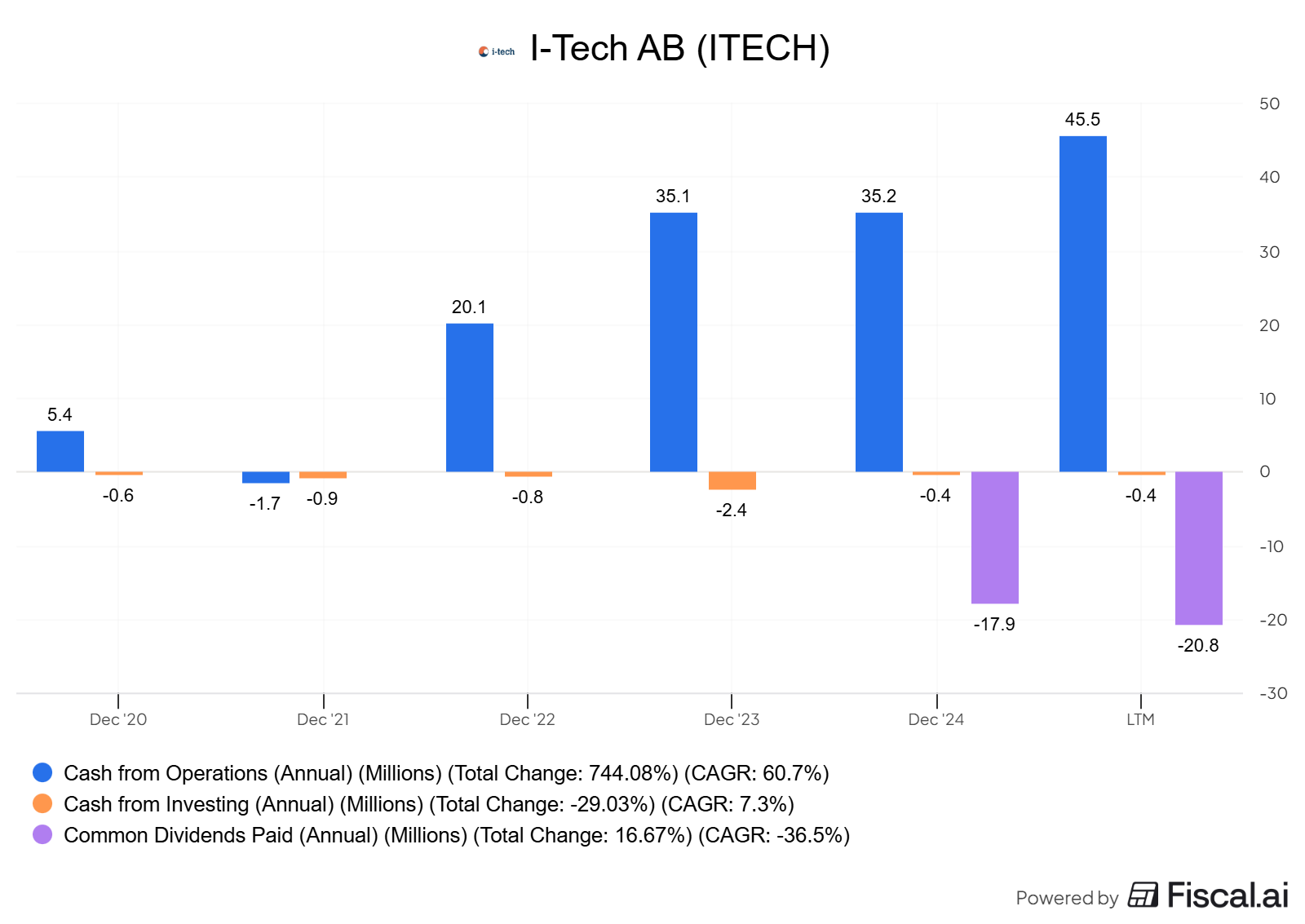

When you look at a chart like this, it’s like they “cracked a code” with their Selektope compound:

Cash is coming in (blue)

They have very few investment needs (orange)

So they give some of it back to the shareholders (purple)

But I would prefer buybacks over dividends any day. Because they allow for a lot more flexibility.

So, what to do? Buy, sell, hold?