This $400m microcap is the hidden backbone of the world Cup

The company is currently mid-transition, evolving from a cyclical hardware vendor into a software ecosystem platform with growing recurring revenues

Hi hunters!

I used to be a soccer fan, a long time ago, when my hair was less grey.

Now, I only look at some matches when a World Cup is on.

Which is today, right on the day of the SpaceX IPO.

Let’s take a look at a company that profits from these kinds of events, and who recently dropped 20% in price.

In this article, we are going to look at a company that plays a key and lucrative role in the industry that brings live sports events into the homes of billions of fans.

This company created its own ecosystem and built a trusted brand for more than a decade, with gross margins over 70% and net margins over 15% while reaccelerating revenue.

Whereas most businesses in sports are barely profitable, this company found its niche and is looking to transform itself to capture most of the biggest infrastructure upgrade cycles in decades.

Company Snapshot

Company: EVS Broadcast Equipment

Ticker: EVS

Exchange: NYSE EURONEXT

Industry: Communications Equipment

Market Cap: $400M

Founding year: 1994

Gross Margins: 70%

ROIC: 20%

Guidance for 2026: $230M (11% growth)

Executive Summary: The architecture of live production

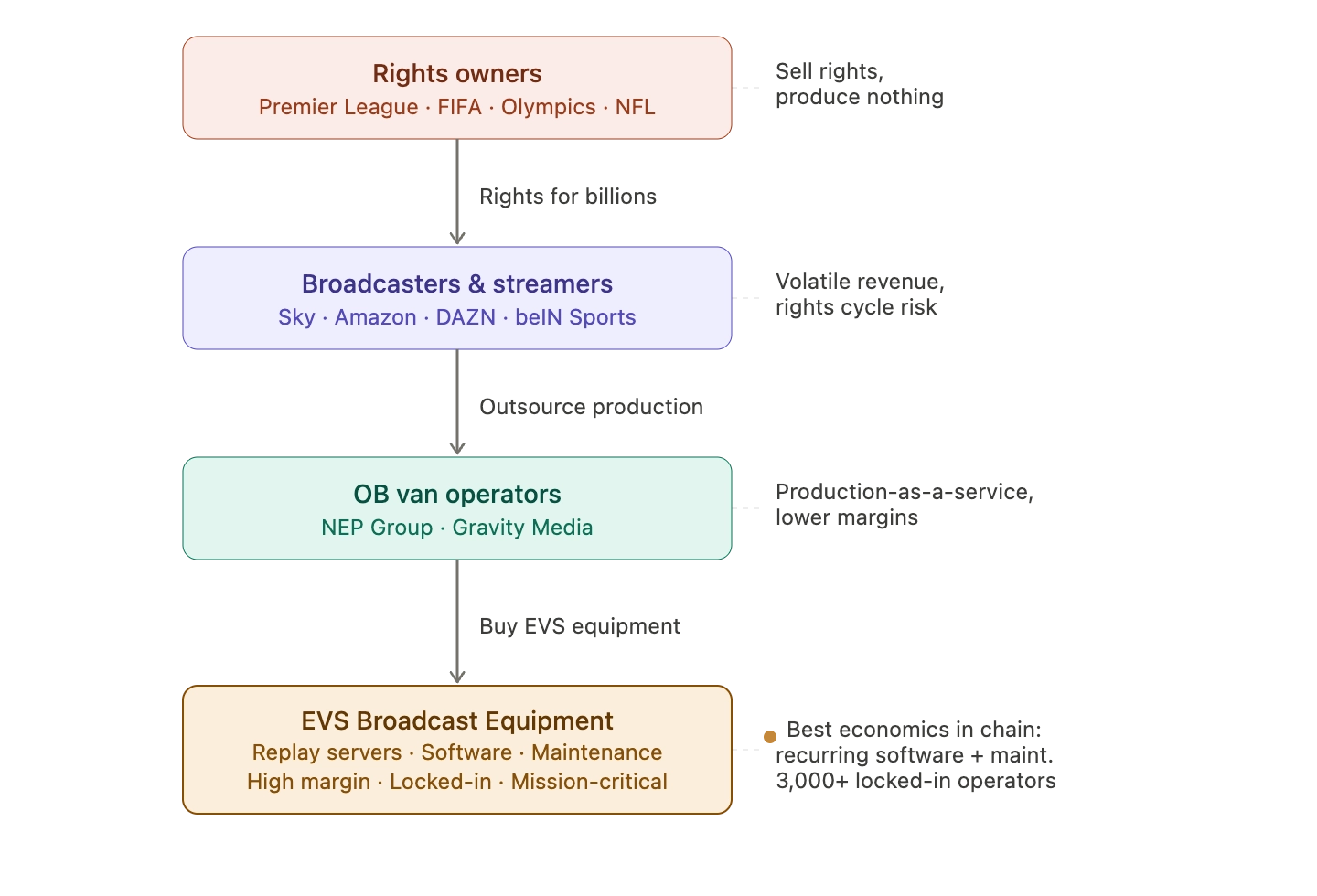

The value chain

EVS Broadcast Equipment designs and sells the hardware and software layers that facilitate the capture, management, and engagement of live video content. At its core, EVS solves the problem of instantaneous storytelling. It allows operators to capture dozens of high-resolution video feeds, synchronize them, and create a broadcast-ready slow-motion highlight or tactical review within seconds of the event. EVS is essentially the Adobe of live production, providing the essential, high-end toolkit that professionals rely on to turn raw footage into a finished masterpiece in seconds.

Let’s use the Champions League quarter-final between Bayern Munich and Real Madrid as a real-world example.

Rights owners: UEFA controls the rights to the Champions League and sells them to Broadcasters for billions. The rights are being auctioned ahead of every season.

Broadcasters and streamers: Sky, Amazon, and DAZN pay enormous sums for those rights and monetize via subscriptions and advertising. They then, most of the time, outsource production to…

OB van operators: Companies like NEP Group and Gravity Media own the trucks, hire the crews, and run the entire live production. They bill broadcasters per event or on long-term contracts. They are operationally complex with lower margins.

Broadcast Equipment: Unlike many technology vendors in the broadcast sector that occupy peripheral or replaceable segments of the value chain, EVS provides the fundamental recording, replay, and media-processing architecture for the world’s biggest live events.

Broadcasters are volatile, OB operators are margin-constrained, and EVS is the high-margin, mission-critical, locked-in supplier that wins regardless of who holds the rights.

As customers, we pay for a subscription and get to see these games live. We get to see dozens of camera angles on the pitch, which are the input data that EVS captures. Replay operators use EVS to edit the game while it’s still happening. Adding slow motion and choosing the best angles to show you exactly what happened. Once the game is over, TV stations around the world can instantly access the footage and show it to fans on their phones or in news broadcasts. It also powers the VAR Assistant.

Business Model

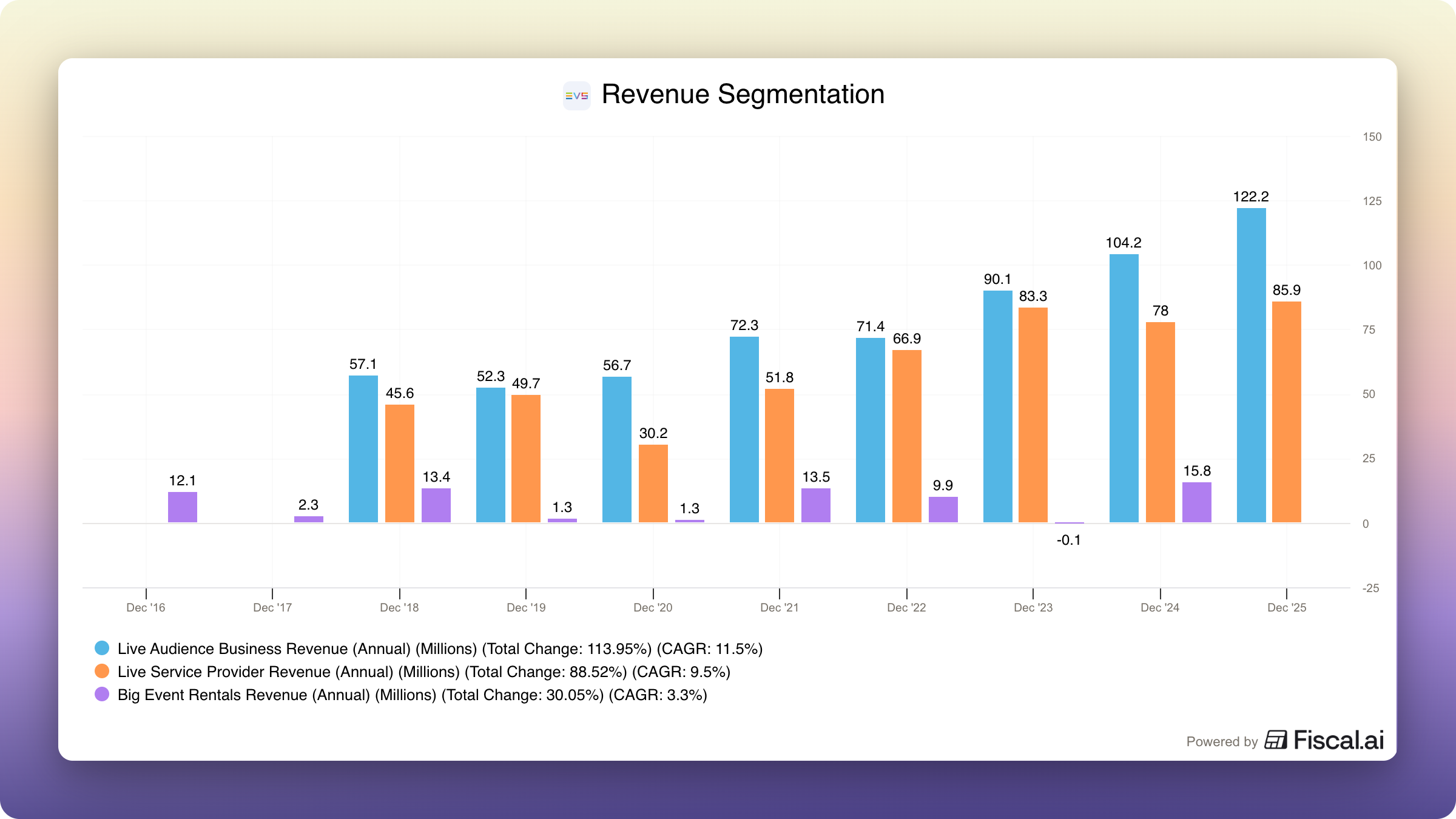

EVS segments its revenue into three categories:

Live Audience Business (LAB): These are customers who have built their own infrastructure to manage their content, such as Sky, ESPN, or stadiums like Real Madrid’s Santiago Bernabéu. EVS can score higher margins in this segment through its recently launched SaaS model and its ecosystem bundle.

Live Service Providers: These are clients like NEP Group and Gravity Media that own a fleet of vans and are contracted to broadcast events. They are the largest buyers of EVS hardware, often purchasing dozens of servers to equip a single large fleet of trucks at lower margins than LAB customers.

Big-event rental: These are large contracts for events like the Olympics and the World Cup, where top-quality equipment is needed to ensure reliable broadcasting.

The growth story here is LAB customers who are increasingly broadcasting their own content.

Competitive Advantages

EVS positioned itself as the default operating system of live sports production. This positioning comes from deep product entrenchment, operator lock-in, and a proven track record at the world’s highest-stakes live events. EVS built a sticky ecosystem around its own hardware and software that a software-only player can’t match. As mentioned before, their products are on the same level as Adobe’s professional products, but in the broadcasting space.

They developed operator familiarity over decades. There are over 3,000 operators globally who have spent 10-20 years mastering the EVS remote. Switching from EVS to a competitor would require retraining the entire freelance crew, introducing unacceptable operational risk for the broadcaster. The maintenance and support renewal rate is exceptionally high, estimated at over 95% for Tier-1 broadcasters. This gives EVS pricing power, as it has an intangible asset that justifies premium pricing due to its high reliability.

The SaaS Transition

Historically, software was a free or low-cost add-on to sell servers or hardware in general. Now the company is pivoting its value proposition from high upfront Capex with long-milestone payments to multi-year subscriptions with software at its center. This recurring revenue mode is expected to exceed 50% of the mix by 2026–2027. This is important for them because it means that they can decouple their base business from its cyclicality.

Strategic Roadmap: PLAYForward 2030

The SaaS Transition is also underscored by management’s stated “BHAG” (Big Hairy Audacious Goal): to be the #1 solution provider in the live video industry by 2030, with a revenue target of $350mn. To achieve this, they plan on executing their strategy via three pillars:

From product provider to ecosystem:

from pure hardware sales (CAPEX) to software and SaaS models (OPEX)

from OB van operators to broadcast centers

from sports-only to entertainment, news, and digital

from a replay specialist to a live production ecosystem in multi-tier markets

Strategic M&A Track Record:

They recently started ramping up their M&A activity to accelerate their technology through:

Axon (2020) is now part of the MediaInfra division with its control (Cerebrum) and IP-gateway (Neuron) technology.

MOG Technologies (2024) was acquired to add to the MediaCeption portfolio, with its cloud-based transcoding and ingest capabilities.

Telemetrics & XD Motion (2025) is now the T-Motion robotics division, used to expand the ecosystem to include automated camera capture.

Those businesses are expected to contribute around €30 million in revenue, accounting for 14% of total revenue in 2025.

Geographic Strategy “Double Down North America”:

North America is EVS’s fastest-growing region, contributing 37,5% of revenue in 2025. North America is the largest and most competitive market, driven by massive sports media rights deals (NFL, NBA, MLB) and a concentration of Big Tech (Amazon, Apple) entering the live arena.

Management

The founder is still on board as the CTO of the hardware department (the largest insider owner,>6%). The CEO is an industry veteran who joined in 2019. He pushed the PLAYForward strategy and the aggressive move into IP and North America.

The live broadcast equipment industry

The broadcast equipment industry is currently passing through its most significant structural pivot since the transition from analog to digital. Historically defined by proprietary hardware and quadrennial sporting cycles, the sector is evolving into a software-defined, IP-native, and AI-augmented ecosystem.

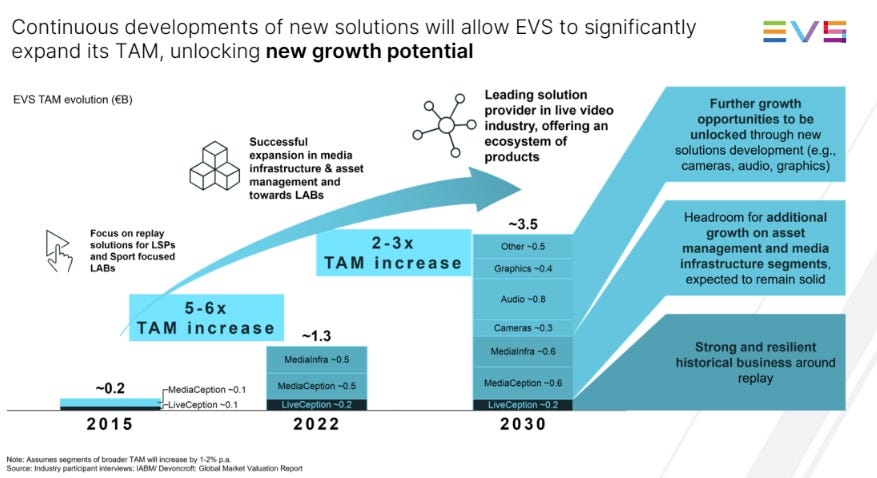

Addressable Market

EVS’s own estimated TAM is the best approximation for what the company could address since it does not compete across the entire live broadcast market. It targets tier-1 sports broadcasters and OB van operators for whom downtime is simply not an option. From where we are now, the company projects the TAM will double by 2030, which is ambitious but justified by their product and market expansion.

Demand-side

It is important to note that EVS’s demand has historically followed a power-law distribution of spend. The top 10 global broadcasters and sports federations (e.g., NBCUniversal, BBC, Sky, FIFA) account for more than half of enterprise spend on high-end production kits. This gave them bargaining power over EVS, but it also meant that they chose EVS because of an existing trust relationship.

Streaming Platforms Entering Live Production

In recent years, however, the entry of Amazon, Netflix, Apple, and DAZN into live sports rights has brought substantial fresh capital into the market. They spent a combined $12.5 billion on sports rights in 2025, representing 20% of the global total sports rights spend of $64 billion. These new entrants need to either build, rent, or partner to ensure a good broadcast experience for their customers. This structurally expands the addressable customer base for EVS and OB operators alike.

The best part is that EVS doesn’t care whether it’s Sky, Amazon, or DAZN buying the rights. As long as high-end live production is happening, EVS gets paid. And since it is the de facto default operating system of live sports production, all professionals needed will demand EVS’s products.

Supply-side

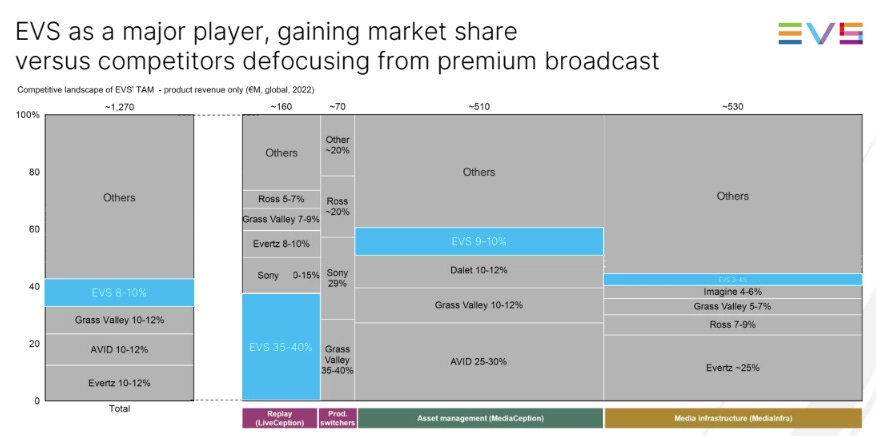

The overall market share for broadcast technology is fairly evenly distributed, with no player exceeding 12%, according to EVS’s own management. Historically, the sector struggled with declining revenues due to the decline of TV. This led to consolidation pressured by PE and the expectation of synergies.

Established Players

EVS stayed independent and kept a tight focus on live production, which is their bread and butter. In recent times, however, they have begun to strengthen their share in other pillars, such as Infrastructure and Media Asset Management, through M&A. This is strategically important, as current trends demand an overall package with greater control across the value chain.

Grass Valley was taken private by Black Dragon Capital in 2021. Grass Valley has emerged as EVS’s most direct competitor, with comprehensive end-to-end solutions and leadership in cloud platforms. The company competes aggressively by leveraging bundled pricing strategies in major sports contracts.

Avid Technology was taken private by the PE firm STG in November 2023 in an all-cash deal valued at roughly $1.4 billion. It overlaps with EVS in the newsroom and Media Asset Management adjacency. Avid’s competitive pressure on EVS comes from owning the creative and editorial layer of the value chain that EVS is increasingly trying to reach through MediaCeption.

Evertz Technologies is listed on the Toronto Stock Exchange (TSX: ET). Its centre of gravity is the broadcast infrastructure. Therefore, it competes with EVS primarily in the MediaInfra pillar rather than in live replay, making it an adjacent infrastructure specialist more than a direct threat to EVS’s core.

Sony’s broadcast business sits inside the professional solutions arm of Sony Group Corporation, the publicly traded Japanese conglomerate. Sony R&D depth and balance-sheet scale can’t be matched by any pure-play vendor. Sony dominates cameras, sensors and image quality, but it has been deliberately building toward an end-to-end position that competes with EVS’s own ambitions to own more of the chain. The result is a “frenemy” dynamic with EVS because their systems are routinely deployed alongside Sony cameras.

A risk worth monitoring for me is the entry of PE capital trying to consolidate the market to increase pricing power, like in the case of Grass Valley. For EVS, this could result in margin pressure fueled by seemingly infinite money that distorts competition, as seen in the case of Chelsea Football Club and professional football. On the other hand, it could also result in a takeover bid for EVS with a premium between 25% and 40% over today’s price (Avid at 32% over the share price at that time).

Risks

EVS operates in a growing market driven by streaming, but is transforming due to the cloud. More live sports events and more streaming buyers expand the volume of production needed, but cloud-native production workflows threaten to gradually commoditize the hardware layer that EVS has historically monetized at 70%+ gross margins. They redraw the competitive map and hand EVS both its biggest long-term risk and its clearest strategic imperative. This transformation can be categorized into two simultaneous shifts.

The architectural shift: from on-premise to cloud-native production

The industry is moving past the binary choice between on-premises and cloud, with compute, switching, and playout occurringhappen in the cloud rather than in a physical OB truck. Grass Valley’s AMPP platform, AWS Elemental MediaLive and Adobe’s Frame.io integrations are the clearest articulations of this vision. For a vendor whose heritage is purpose-built hardware, this is the most serious threat as it questions not the product, but the premise.

The business-model shift: CAPEX → OPEX

Broadcasters and OB operators are under structural pressure to move away from large upfront capital expenditures, such as buying servers outright, toward operating-expense models. The shift is double-edged. Done well, it converts lumpy, event-driven hardware sales into predictable recurring revenue. Done poorly, it cannibalizes the high-margin hardware business before the software revenue stream is mature enough to replace it. The classic SaaS J-curve.

EVS’s answer: Balanced Computing

EVS’s response is a deliberate bet against the binary. Rather than choosing on-prem or cloud, it is positioning itself around a hybrid model in which high-performance on-prem hardware handles what genuinely requires it, while cloud modules handle everything else in a more elastic way.

Conclusion

The company’s bet is that ultra-low-latency live replay is the last function to move to the cloud, that the 2-second requirement for a Super Bowl replay is a hard physical constraint that keeps dedicated on-site hardware relevant for longer than skeptics assume. So far, the market has validated that bet.

Whether it holds through 2030 is the kicker question!

The opportunity - why the shift to IP matters for EVS

One of the most underappreciated drivers behind EVS’s growth is the industry’s migration from SDI (Serial Digital Interface) to IP (Internet Protocol) infrastructure. Think of SDI as dedicated cables each carrying a single video signal point-to-point, and IP as a flexible, software-defined network. For decades, live production ran on SDI.

Crucially, this is a structural transition over time, making it a long, staggered investment cycle for equipment vendors.

For EVS, that cycle reshapes what it can sell. In the SDI world, EVS sold replay servers, which it pioneered and still dominates. In an IP world, feeds, metadata, replay, routing, and control all run on a single network, and that complexity is an addressable market: EVS can now sell the control systems, orchestration software, and infrastructure layer that tie the whole production together. The prize is the shift from selling one box to capturing a far larger share of each customer’s infrastructure budget.

But IP is not pure upside. The same shift onto standard hardware and networks that expands EVS’s market also lowers the barrier that protected purpose-built broadcast hardware, letting software and cloud players into the same workflows.

For an investor, this is ultimately a revenue-mix story where EVS is trying to turn a cyclical, hardware-driven business into one with more software and recurring revenue. If it works, EVS re-rates from a hardware vendor toward a stickier platform business; if the hardware base erodes faster than software can scale, it becomes the J-curve risk.

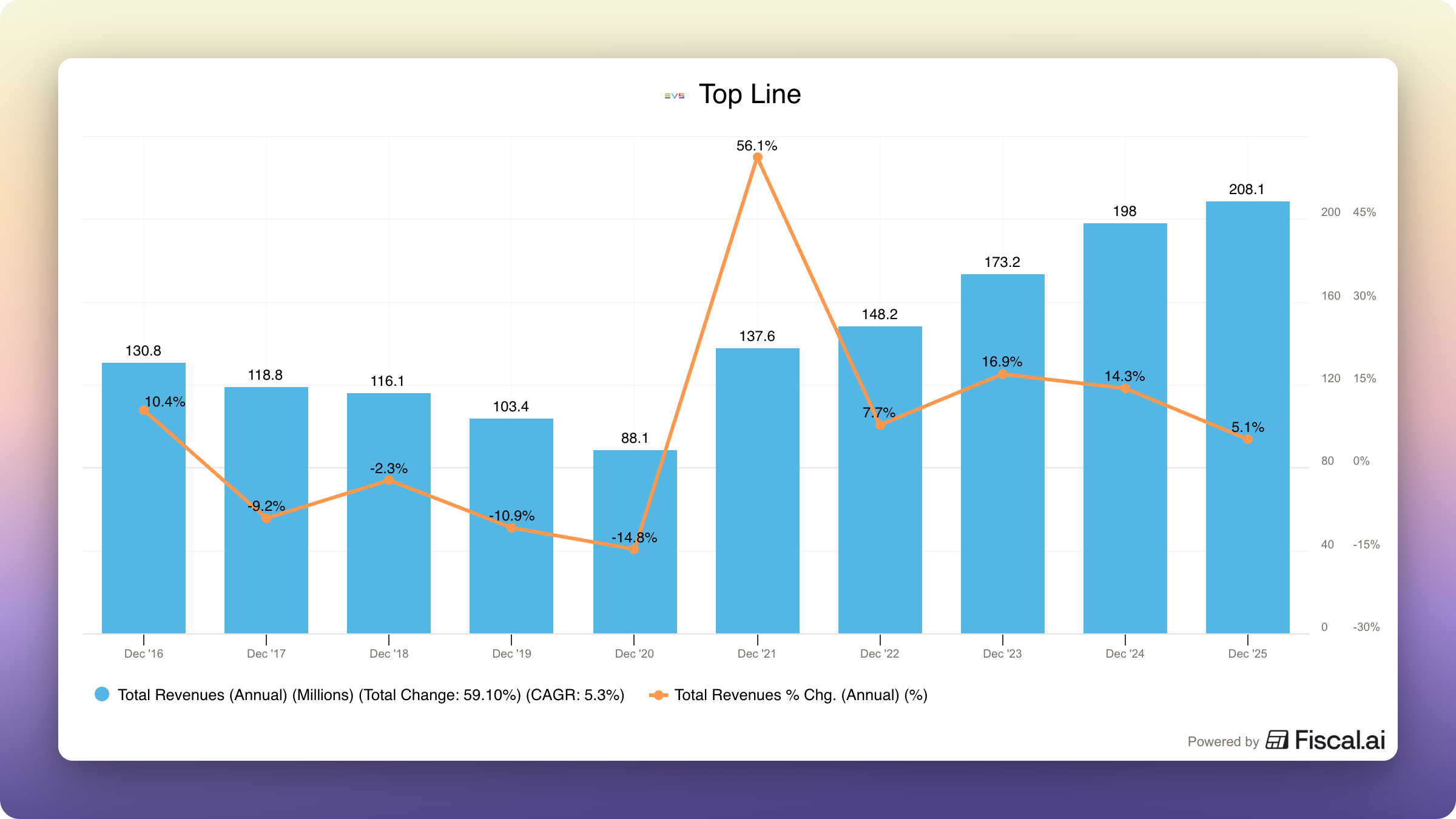

The Financials - why EVS stood still for a decade

We use fiscal.ai for all our charting. Grab a 15% discount through this link.

In EVS’s 2023 annual report, the company acknowledged a plateau in revenues since 2012. The cause was structural. Even though EVS dominated live replay servers, the market matured as the company only replaced outdated equipment. And for years, EVS simply failed to build a second pillar because its replay franchise was so dominant that it became a comfortable trap. To counter this inertia, the new CEO announced the PlayForward Strategy mentioned earlier.

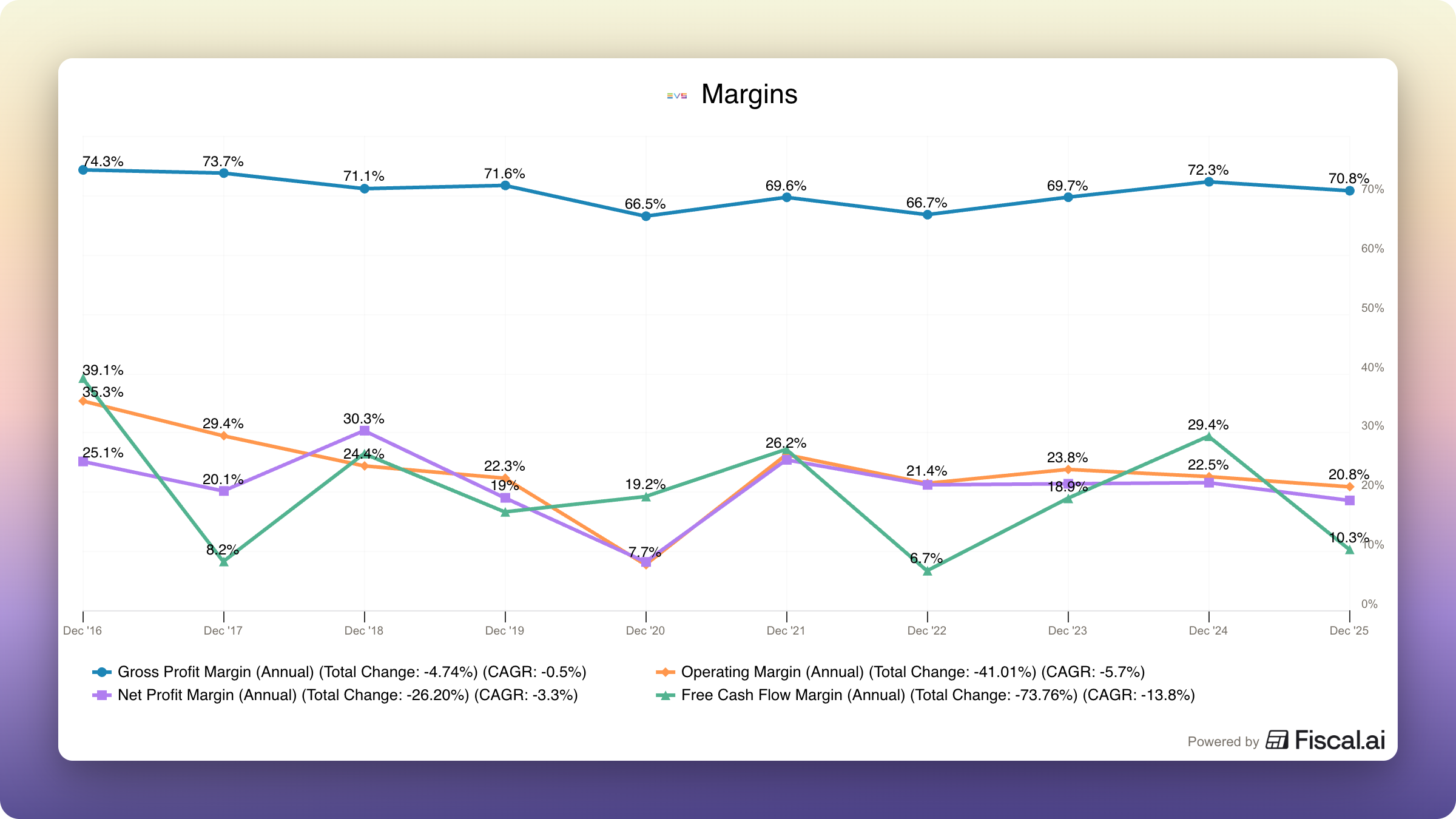

On the margin side, it looks similar, as the company’s margins are in a slightly downward trend over a 10-year perspective. This is partly due to North American expansion, which increased SG&A costs.

The ROIC and ROE are moving on a similar plateau between 17-25%, which is similar to Evertz.

How much does EVS invest in the future?

EVS is, at its core, an engineering company where R&D is the real investment in the future and almost as big as SG&A. The business itself is high-margin, asset-light, and cash-generative, with excellent existing economics but historically mediocre incremental returns. This should change as EVS revenue becomes more predictable, as evidenced by order backlog visibility. Entering 2026, EVS has a record order book of €182.2 million. This provides coverage for nearly 80% of the 2026 revenue guidance (€220-240 million).

EVS pays a €1.10 dividend at a ~35% earnings payout ratio, while still accumulating net cash. This tells me that EVS has a hard time finding enough high-return projects to absorb them. That is the classic signature of a high-quality but low-reinvestment-runway business.

The counter-signal is management’s public ambition of reaching €350m in annual revenue by 2030. If they mean it, the reinvestment rate should rise from here, and that is the number to watch, not the current margin.

So, although the past looks bad and the future looks promising, is this company a BUY or not?

In the end, it’s all about valuation, as a great company can still be a bad investment.

So what is EVS worth?