Is AI going to kill your favourite SaaS company?

Our AI-resilience checklist

AI is advancing at lightning speed.

In just a few months, the narrative that AI is making software companies even stronger has been called into question by the release of Claude’s latest capabilities, which have reshaped expectations across the Software landscape.

We’re seeing market disruption happening in real time.

And I’ve been using Claude Code for a couple of months now, also for stock analysis, and I do believe the disruption is real.

It’s no longer: “Can I build it?” It’s should I build it?

But the breakdown of software companies won’t come overnight. Multiples will have a hard time rerating. Most of them will die slowly.

While this industry drawdown is playing out in real time, every investor should be asking the same two questions:

How do I know if a company is likely to be disrupted by AI?

Which names are being wrongfully sold off in this industry drawdown?

To answer both questions, we developed the following checklist.

Checklist

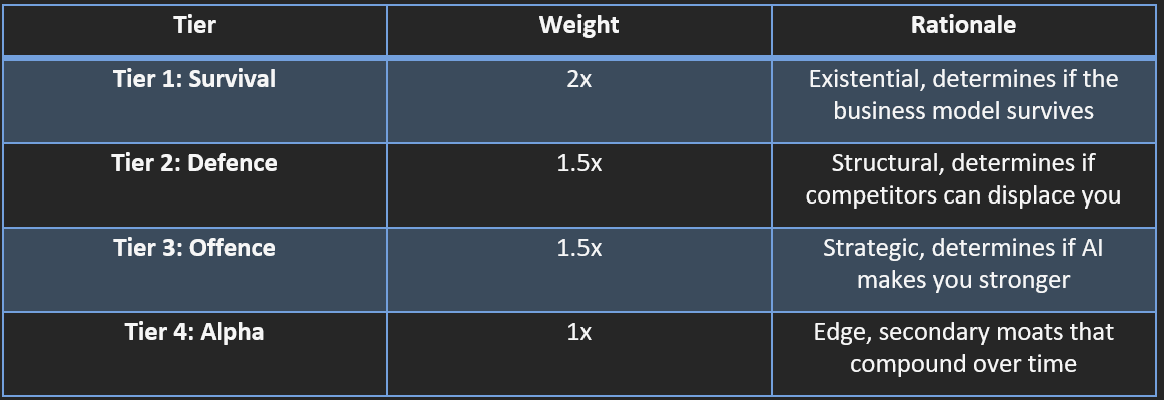

The Checklist consists of nine lenses across four tiers, with three exposure types (Exposed, Neutral, Antifragile).

We assigned a weight to each of them

Tier weights:

The scoring system is as follows:

Exposed = -1 point

Neutral = 0 points

Antifragile = +1 point

Score range: -13.5 to +13.5 (weighted)

Let’s dive into the framework…

Tier 1: Survival - Do you still have a business in 5 years?

1. Pricing Model (The “Cash Flow” Pillar)

Question: Does the company charge for an outcome or per user seat?

This is the most immediate threat to cash flow. If you charge per human seat and AI makes humans 10x more productive, your revenue will mathematically collapse by 90%. The shift from paying for work to paying for outcomes is the difference between a thriving business and a dying one.

Exposed: The company charges its customers solely per seat. Revenue is directly tied to headcount, which AI will compress.

Neutral: The company blends seat-based and usage-based charges. Some revenue still scales with headcount, but AI-driven efficiency can be offset by fees tied to data volume, API calls, or feature usage.

Antifragile: The company charges based on consumption, outcomes, or value delivered (compute, transactions, storage, data volume). AI adoption amplifies revenue as usage grows.

2. Failure Sensitivity (The “Liability” Pillar)

Question: How accurate does AI need to be to replace this software?

This defines the “Trust Gap”. AI is probabilistic; if a guess results in a typo in a blog post, it’s fine. If it results in a plane crash or a cybersecurity breach, it’s a disaster.

Exposed: 90% accuracy is good enough for the company’s core use case (e.g., marketing copy, basic graphic design). The software is likely to be replaced by AI.

Neutral: AI needs to be consistently reliable (97-99% accurate), but occasional errors are tolerable with human review. The software is partially defensible.

Antifragile: Failure or hallucination is catastrophic (e.g., medical diagnostics, cybersecurity, power grid management, financial compliance). The software is harder to replace with a probabilistic AI model.

Tier 2: Defence - Preventing competitors from eating your lunch

3. Workflow Integration (The “Stickiness” Pillar)

Question: How many system intersections does it control?

Even if an AI tool is better, a company won’t switch if that software is the central nervous system connected to 50 other apps. Replacing a core workflow is like performing heart surgery; most companies would rather just upgrade their current heart with AI.

Exposed: The software operates as a standalone tool with minimal integrations, few dependencies, and low workflow entanglement. It is easier to replace.

Neutral: The software connects to multiple systems but does not serve as the central coordination layer. Replacing it creates friction, but not systemic breakdown.

Antifragile: The software sits at the intersection of many systems, acting as a coordination hub or workflow backbone. Replacement becomes structurally difficult.

4. Switching Cost (The “Friction” Pillar)

Question: How much accumulated value would a customer lose by leaving?

This is distinct from workflow integration. A product can have few integrations but enormous switching friction due to years of accumulated data, configurations, trained employees, and organisational muscle memory. The question isn’t how connected it is? It’s how painful it is to walk away.

Exposed: Customer data is easily exportable, minimal customisation is built on top, and retraining cost is low. A competitor can replicate the experience with minimal migration effort.

Neutral: Customers have a moderate level of accumulated investment, such as historical data, custom configurations, or trained workflows, but migration is feasible within a quarter with dedicated effort.

Antifragile: Customers have years of accumulated data, configurations, custom automations, compliance audit trails, and deeply trained teams. Migration would require months of effort, retraining thousands of employees, and risking operational disruption. The cost of switching far exceeds the cost of staying.

5. Customer Base (The “Inertia” Pillar)

Question: Who does it primarily serve?

Enterprise clients aren’t a moat on their own. However, the cost of software is often negligible compared to retraining 10,000 employees and reconfiguring 100 internal processes. There is a reason why so many people still use Microsoft solutions for use cases where better alternatives exist.

Exposed: The software mainly serves individuals or small businesses. Switching costs are lower, and experimentation is higher.

Neutral: The company serves both SMB and enterprise clients. Defensibility depends on contract structure, integration depth, and switching friction.

Antifragile: The software primarily serves large enterprises. Displacement is significantly harder. Enterprise environments involve procurement cycles, compliance requirements, multi-year contracts, security audits, and cross-department integration.

6. Network Effects (The “Ecosystem” Pillar)

Question: Does the product become more valuable as more participants join the ecosystem?

A product with true network effects creates a self-reinforcing flywheel that is difficult to replicate. It’s not enough to have integrations (that’s Workflow Integration) or switching costs (that’s Friction). This lens measures whether the ecosystem itself compounds in value as scale increases. A marketplace with 10,000 apps is not just 10x better than one with 1,000. There’s a quality difference.

Exposed: The product is a standalone tool with no meaningful ecosystem dynamics. Value is linear; each customer gets the same experience regardless of how many others use the platform. No integration marketplace, no third-party developer community, no cross-customer data benefits.

Neutral: The product has some ecosystem elements, a modest integration marketplace, partner channel, or community, but these are additive rather than compounding. Competitors could replicate the ecosystem with sufficient investment. The product would still function without the ecosystem.

Antifragile: The product sits at the centre of a self-reinforcing ecosystem where value compounds with scale.

Tier 3: Offence - Can AI make this company stronger?

7. AI Adoption Capability (The “Offence” Pillar)

Question: How effectively is the company integrating AI to strengthen its product and expand its market?

Defence alone isn’t enough. The companies that will win the AI era are the ones that use AI to widen their moat by embedding it into their product to deliver more value, expanding into adjacent markets, or creating entirely new revenue streams. A company that is antifragile on defence but slow on AI adoption can still lose to an incumbent that moves faster.

Exposed: The company has no meaningful AI strategy, no AI features shipped, and no public roadmap for AI integration. It is passively waiting for disruption rather than responding to it.

Neutral: The company has announced or shipped AI features (e.g., copilots, assistants, AI-generated suggestions, AI-powered automation), but these are incremental enhancements to existing products. AI is a marketing message and a feature, not a proven revenue driver. Most software companies in 2025-2026 fall into this category.

Antifragile: The company has demonstrated measurable AI impact on its business by not just shipping features, but also proving results. Only a few companies to this day have this.

Tier 4: Alpha - Secondary moats that compound over time

8. Data Ownership (The “Intelligence” Pillar)

Question: How much proprietary data is involved?

Data is only useful if it’s proprietary and clean. If your data is just a mirror of what’s on the public web, it’s not a moat. It only matters if it’s “under-the-hood” data that public models can’t see.

Exposed: The software relies primarily on public, user-exportable, or easily replicable data.

Neutral: The company holds some proprietary data, but it is customer-specific and not meaningfully aggregated across the network.

Antifragile: The company controls proprietary, network-aggregated data that improves as more users join. It benefits from strong data gravity. The system becomes smarter at scale in ways public AI models cannot replicate.

9. Regulatory Exposure (The “Red Tape” Pillar)

Question: Do legal or compliance barriers protect the business?

Regulation is a speed bump moat. It keeps small startups out because they can’t afford the legal fees, but it doesn’t stop a determined incumbent. It’s a great secondary defence, but a weak primary one.

Exposed: The software operates in a lightly regulated environment with minimal legal constraints.

Neutral: The company operates in a regulated environment, but compliance is standardised and replicable. Regulation slows entrants but does not prevent disruption.

Antifragile: The software operates in a highly regulated domain where legal approval, certifications, audits, and liability structures are complex and time-consuming. Regulation becomes a structural moat.

Stress testing HubSpot, SYS-DAT, and Rubrik

Now that we have established the framework, we are going to test it on three companies:

HubSpot is a CRM platform that helps small to medium-sized businesses attract customers, automate marketing and sales, and manage relationships all in one integrated system.

SYS-DAT is an Italian IT services company that supports manufacturing businesses in Italy through ERP solutions, cybersecurity, cloud infrastructure, and data management.

Rubrik is a cybersecurity company that protects and manages enterprise data by providing backup, recovery, and ransomware resilience across cloud and on-premise environments.

Walk through the checklist

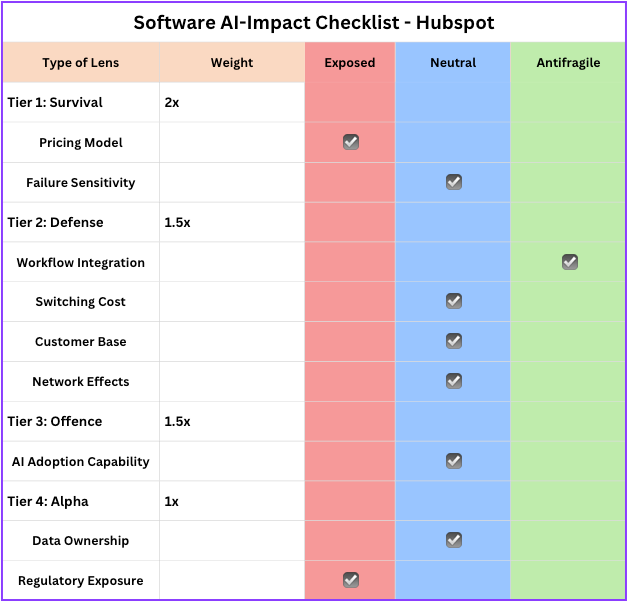

HubSpot is down 35% since the beginning of the year. Let’s see how well their moat holds up against AI:

1. Pricing Model

This is the Achilles’ Heel. HubSpot’s revenue is historically tied to Core Seats. If AI allows a small team to do the work of a department, the customer will naturally reduce their seat count, directly eroding HubSpot’s top-line revenue. They are attempting to shift toward platform-wide fees, but the seat-based legacy model remains high risk.

Verdict: Exposed

2. Failure Sensitivity

HubSpot’s primary use cases, like marketing emails, blog posts, and sales outreach, are probabilistic tasks. If an AI generates a draft that is 90% correct or the customer information has minor errors, it’s not the end of the world. However, there will still be human interaction needed, since customer information and blog posts vary and are customer-facing.

Verdict: Neutral

3. Workflow Integration

This is HubSpot’s greatest strength. It acts as the System of Record for the mid-market, connecting marketing, sales, and service. With thousands of App Marketplace integrations, pulling HubSpot out of a business often causes a systemic breakdown in operations.

Verdict: Antifragile

4. Switching Cost

HubSpot primarily serves the 20–500-employee segment, where years of CRM data, sequences, and workflows create meaningful switching friction. Switching is painful but not prohibitive, especially for the smaller end of HubSpot’s base, where customisation depth is lower and new tools could accelerate the process.

Verdict: Neutral

5. Customer Base

HubSpot is the king of the mid-market. While these businesses are stickier than individuals, they are also the first to experiment with lean, AI-only marketing teams to save on overhead during industry shifts. HubSpot primarily utilises annual contracts for its professional and enterprise tiers, while offering more flexible monthly options for starter plans.

Verdict: Neutral

6. Network Effects (The “Ecosystem” Pillar)

HubSpot’s 1,900+ connector marketplace and growing Breeze agent ecosystem are real, but they are additive rather than compounding. The integrations are overwhelmingly connectors to third-party tools like Slack, Google Workspace, Salesforce, and Zapier that push and pull data in and out of HubSpot, rather than ISVs building differentiated, standalone products on top of HubSpot that customers depend on in their own right.

Verdict: Neutral

7. AI Adoption Capability

Breeze Customer Agent resolves over 50% of support tickets during early HubSpot deployments. However, no AI-specific revenue has been disclosed, and the features (copilots, assistants, summarisation) are broadly similar to those offered by every major CRM competitor. Strong execution, but not yet a proven revenue driver or new-market unlock.

Verdict: Neutral

8. Data Ownership

HubSpot holds a massive amount of customer-specific data, but it is siloed. While they have launched “Breeze” to help aggregate insights, the data is ultimately user-owned and exportable. They lack a “network-aggregated” moat where one user’s data makes the tool significantly smarter for everyone else (unlike a cybersecurity firm).

Verdict: Neutral

9. Regulatory Exposure

HubSpot primarily operates in marketing, sales, and customer service - lightly regulated activities with no meaningful certification barriers. Any well-capitalised AI-native startup can compete in this space.

Verdict: Exposed

Weighted Score = (Tier 1 sum x 2) + (Tier 2 sum x 1.5) + (Tier 3 sum x 1.5) + (Tier 4 sum x 1)

HubSpot gets a final score of -1,5 (Score range: -13.5 to +13.5)

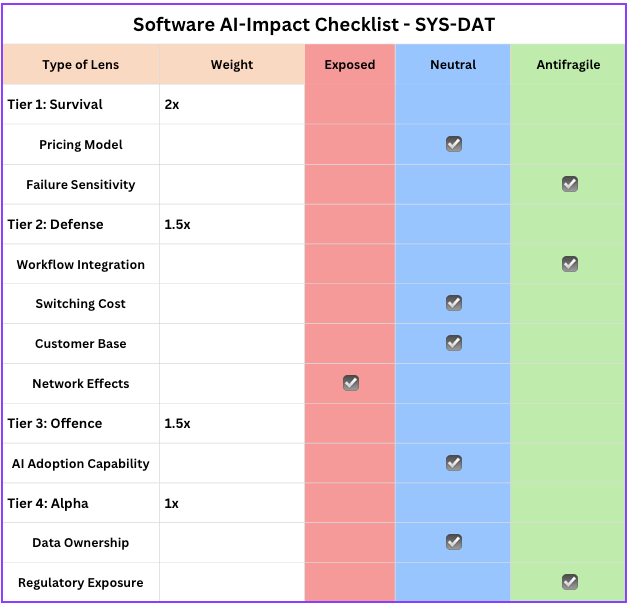

Now let’s walk through the checklist with SYS-DAT, which has been sold off by 20% ytd. You can read our deep dive here.

1. Pricing Model

Much of their revenue comes from long-term maintenance contracts, project-based implementations, and modular licenses. These are often calculated as a fixed percentage of the initial software value, regardless of how many people log in. Some revenue still scales with headcount, however.

Verdict: Neutral

2. Failure Sensitivity

SYS-Dat acts as the single source of truth for a business: warehouse management, finance, and supply chain. In the Italian regulatory environment, an ERP error in a VAT return or on a manufacturing line can lead to heavy fines or production shutdowns. You cannot hallucinate an inventory count.

Verdict: Antifragile

3. Workflow Integration

System integration is in their DNA. Their software acts as the central hub for manufacturing execution systems (MES), CRM, and Retail. It is the software glue that holds an Italian SME together.

Verdict: Antifragile

4. Switching Cost

Multi-year implementation projects, custom integrations, and trained internal teams create real friction during migration for SYS-DAT clients. But because SYS-DAT largely relies on third-party platforms, a client could theoretically switch to SYS-DAT as the integrator while retaining the underlying software.

Verdict: Neutral

5. Customer Base

SYS-DAT serves businesses ranging from micro-enterprises to large multinationals across the Italian manufacturing industry. The mix is broad rather than enterprise-focused, which provides revenue diversification but limits the structural inertia that comes from predominantly serving large enterprise clients with complex procurement and compliance requirements.

Verdict: Neutral

6. Network effects

SYS-DAT has no app marketplace, no developer ecosystem, and no cross-customer data flywheel. Value delivered to one client is independent of the number of other clients on the platform. It is a professional services and software reseller business with linear, not compounding, scale dynamics.

Verdict: Exposed

7. AI adoption

SYS-DAT references AI across its offering and has acquired cybersecurity and digital commerce capabilities. However, there is no evidence of disclosed AI-specific revenue, a proprietary AI model, or AI enabling entry into genuinely new markets. The strategy appears to be keeping pace with vendor roadmaps (SAP, Cegid) rather than driving a proprietary AI wedge.

Verdict: Neutral

8. Data Ownership

They own deep, industry-specific data silos (e.g., textile production cycles in Tuscany). While this data is clean and valuable, much of it is specific to individual clients rather than to a network-aggregated “mega-brain” that gets smarter across all users.

Verdict: Neutral

9. Regulatory Exposure

Italy has some of the most complex tax and labour laws in Europe. SYS-Dat builds these local legal nuances directly into its code. A Silicon Valley AI agent doesn’t know the specificities of Italian digital product passports or local labour audits. SYS-Dat is building its AI suite (ArIA) to be compliant by design within this specific Italian framework.

Verdict: Antifragile

SYS-DAT gets a final score of 3 (Score range: -13.5 to +13.5). Looking a little bit better than HubSpot, but a bit stuck in the middle.

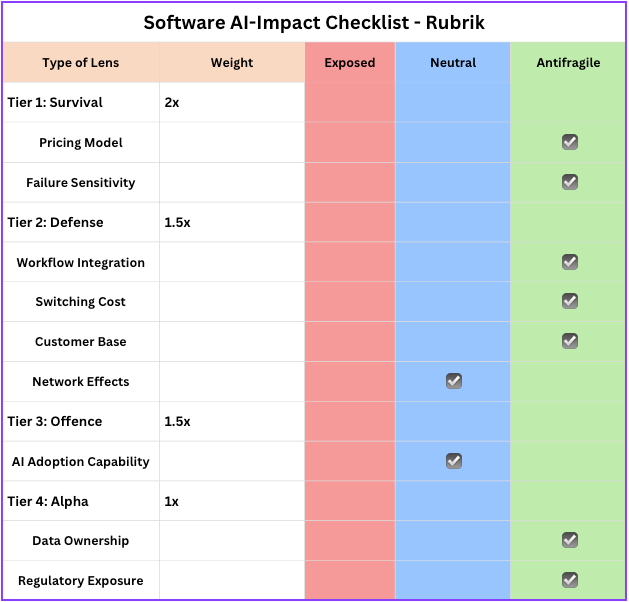

Last but not least, let’s look at Rubrik, which is down 30% ytd:

1. Pricing Model

Rubrik charges based on Subscription ARR (linked to data volume and capacity). As AI models generate massive amounts of new data and “Shadow Data” stores, Rubrik’s taxable surface area grows. They don’t care if a company has 10 employees or 10,000; they care about the Petabytes of data being protected.

Verdict: Antifragile

2. Failure Sensitivity

In the 2026 threat landscape, mostly recovered isn’t good enough. If Rubrik fails to restore an immutable backup after a ransomware attack, the client faces total operational collapse or even loss of life (in healthcare). AI hallucinations in recovery are unacceptable; the system must be deterministic.

Verdict: Antifragile

3. Workflow Integration

Rubrik is the central nervous system of a company’s Disaster Recovery (DR) plan. With the launch of Rubrik Agent Cloud in late 2025, they have moved to monitor and audit the actions of AI agents themselves, making them the coordination hub for AI safety and data integrity.

Verdict: Antifragile

4. Switching Cost

Rubrik customers accumulate years' worth of immutable backup snapshots, SLA policy configurations, compliance audit trails, and recovery runbooks within the platform. The switching cost is not primarily financial. It is the risk of losing validated recovery capabilities and audit continuity during any migration window. In a domain where downtime is measured in millions per hour, that risk is prohibitive.

Verdict: Antifragile

5. Customer Base

As of early 2026, 85% of their revenue comes from customers spending over $100k annually. These are Fortune 500 giants with zero trust mandates. The psychological and technical friction of moving an entire enterprise backup and security architecture to a new vendor is monumental.

Verdict: Antifragile

6. Network effects

Rubrik does not operate a marketplace that others build upon, and its value does not compound significantly across customers the way a platform with third-party developers would. There is a partial cross-customer benefit through shared threat intelligence (the Data Threat Engine learns from signals across its installed base), but this is not yet a primary, publicly quantified moat.

Verdict: Neutral

7. AI adoption

Rubrik’s Ruby AI companion handles backup failure diagnosis, root cause correlation, and guided cyber recovery workflows, and machine learning models in the Data Threat Engine continuously learn to reduce false positives. This is meaningfully integrated AI, not just a copilot wrapper, but Rubrik has not yet disclosed AI-specific revenue contribution or demonstrated that AI has opened genuinely new market segments. Strong execution, not yet proven commercial uplift.

Verdict: Neutral

8. Data Ownership

Rubrik sits on the most valuable data a company has: its backups. With Rubrik Annapurna, enterprises can now create secure embeddings from this data to feed into internal RAG (Retrieval-Augmented Generation) models. They are the gatekeepers of the company's proprietary brain.

Verdict: Antifragile

9. Regulatory Exposure

Rubrik is a certification fortress. With FedRAMP High, GovRAMP, and their new Security Cloud Sovereign (Jan 2026), they meet national security standards that generic software startups cannot touch. In 2026, data sovereignty is a legal requirement that Rubrik has productized into a moat.

Verdict: Antifragile

Rubrik gets a final score of 10,5 (Score range: -13.5 to +13.5).

Conclusion

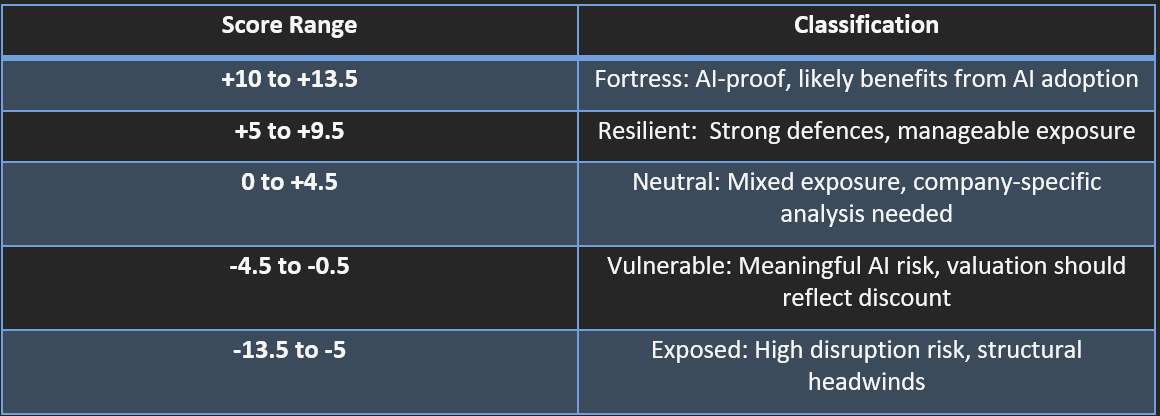

HubSpot (-1.5) is vulnerable.

HubSpot falls into the Vulnerable classification with meaningful AI risk, and a valuation that reflects this discount. I expected it to be in this category; however, I am still not certain if the harshness of the 70% sellof is justified for a company that could still grow modestly with smaller margins at 4x sales.

SYS-DAT (3) is neutral.

SYS-DAT is in the neutral classification, where only some parts of the business are affected, and only some parts benefit from AI. If they successfully integrate AI into their processes, they might actually benefit from the AI-eats-software narrative because of depressed valuations of future M&A targets.

Rubrik (10,5) is a fortress.

Rubrik is part of the fortress classification thanks to its cloud-native architecture and the implementation of AI in its core products. Those are the companies that will not only survive but also flourish, which is why Investors should pay extra attention to this category.

We’ll use this framework to analyze about 150 software companies, like Adobe, Duolingo, and many others.

It will give you an AI-resilience quality score that you can use to include in your overall analysis and valuation of the company.

Big Excel incoming…

May the markets be with you, always!

Kevin

Really like having a framework. The AI will kill SaaS narrative is lazy. It will come down to the things you describe. Well done.

Any thoughts on agents needing SaaS seats to operate?

Some will die, while others will survive and thrive.