A stock investor’s n°1 secret weapon for excess returns

Too often overlooked

Let’s start at the beginning.

Damodaran

5 years ago, when I was going through the Damodaran “advanced valuation” class, I went deep into the weeds.

As an engineer, I loved this.

All the nitty gritty details. The elaborate Excel sheets. It got me salivating as if in anticipation of a juicy burger.

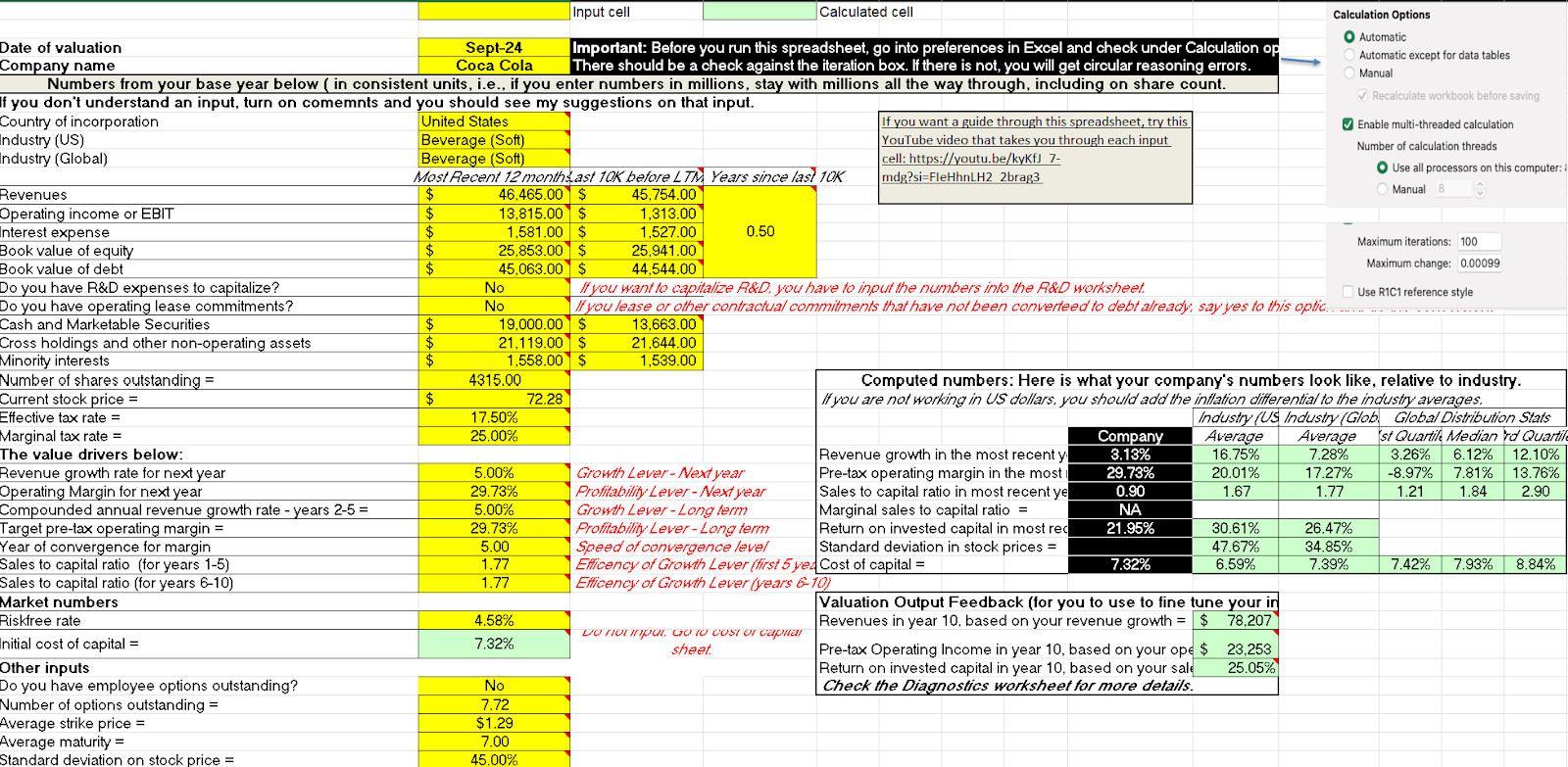

Here’s a ‘partial’ screenshot of one of the professor’s Excel spreadsheets with 17 tabs. It’s a full DCF calculator.

And it all makes sense. The theory behind it. All the assumptions.

But the one thing I struggled the most with was the cost of capital. And this number is not a detail. It’s your discount rate that is used to recalculate future cash in today's dollars. Tweaking this has a big impact on the result.

My brother-in-law, after graduating with his University degree in Economics, landed his first job and had to calculate WACCs all the time.

The Weighted Average Cost of Capital.

And on the surface, it makes sense. You make sure that the return on your investment is higher than the cost of it.

You can find this all over previous investing papers.

A company can grow while destroying value: ROIC < WACC

A company can grow while creating value: ROIC >WACC

The logic is irrefutable. If you raise money at 5% and you can earn at 10%, then you’ve got something good going on.

But to define the WACC

You first need to define the cost of equity, which requires the risk-free rate (OK) and the beta (what?)

You then need the cost of debt, where you try to assess the quality of the debt with the maturity to get to an interest rate

The result after going through the sheet?

A precise number of the intrinsic value you can compare to the current price

The cost of capital depends on the specific business

Damodaran then improves upon this by using a Monte Carlo simulation to get a distribution of intrinsic values. That’s smart.

But there are some caveats that I’ve learned over the years:

The process of calculating the intrinsic value is what is useful. Not the end result.

The final number is just a number. Valuation, by definition, cannot be precise. There is too much uncertainty.

What you want is when something that smacks you in the face, where you think: How can this be true? Where you don’t need Excel to know it’s undervalued. But these situations are rare.

The Magic of Constellation Software

Many articles have been written on Constellation Software and its president, Mark Leonard.

As a shareholder, you should be happy:

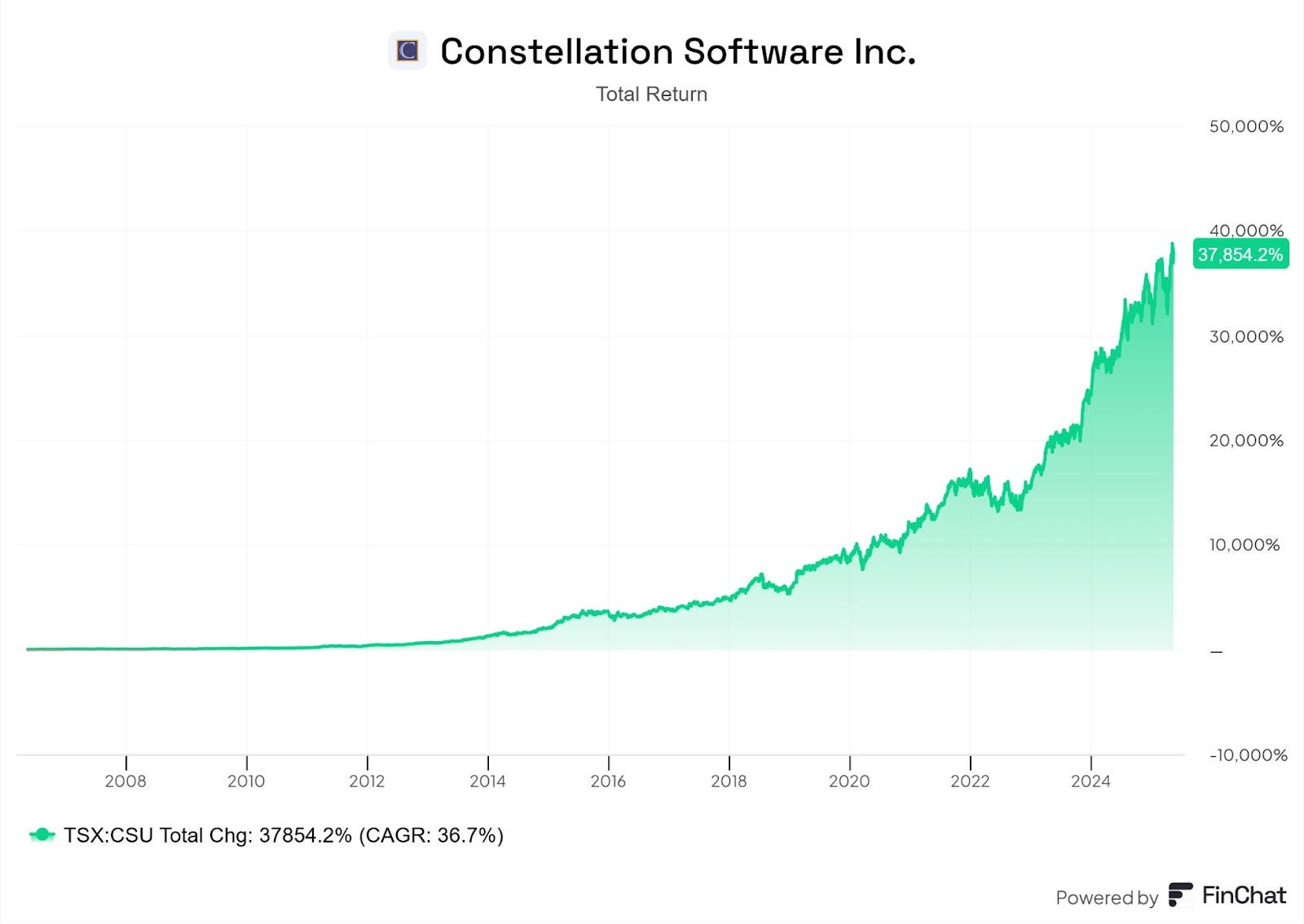

A 370-bagger

A 36.7% CAGR since 2006

Over the last 10 years:

EPS has quadrupled

P/E has doubled from 50 to 100

Yep, it has a PE of 100 now.

And what’s crazy about this company is, despite its size, it is actually accelerating revenue growth from a 19% 10-Y CAGR to a 24% 3-Y CAGR.

Their business model is simple: Buy and Build

Step 1: Acquire profitable Vertical Market Software businesses

Step 2: Grow them, make them better

Step 3: Use excess cash to repeat the process

Profitable niche software businesses are our favorite, too, if you’ve read the article below.

Constellation uses a decentralized approach, and over the last 30 years, it has served them well.

But their true magic bullet: An extreme due diligence process and maniacal focus on their hurdle rate.

Does Constellation calculate the cost of capital of its acquisition prospects? Probably.

But more importantly, they use a high hurdle rate and do an ROI assessment using that hurdle rate.

Although I don’t think they disclosed it officially, it's rumored to be 25%/year.

Your secret weapon: Your Hurdle Rate

How do you define your discount rate in a DCF or reverse DCF?

Some say, well, it depends on the company. How much risk is there?

Others say, well, I have no idea, but if I take 10%, I should be above the cost of capital, and we should be ok

Buffett would say: What is my opportunity cost?

I personally always set it at 15%. Because that is my hurdle rate. It’s the investment return I’m looking for.

But then I went to Omaha. The best investors I met, who had great returns, all used a very high hurdle rate up to 25%/year or more, just like Constellation does.

When applying the rule of 72, that means doubling in 3 years.

The big advantage Constellation has is that it can make businesses better. (the build part) That is a big disadvantage we have. We have to make do with what we buy on the public markets.

Increasing your hurdle rate makes sense, and there are 2 main reasons:

If you’re going through different opportunities, you only want to dive deeper into the best ones. The easiest way to filter? Use a high hurdle rate. Buffett has always said that your goal is to find reasons to say “no” to an investment. Increasing your hurdle rate makes it easier to dismiss opportunities.

The second reason is a natural margin of safety. If you use 25% as a hurdle rate, and your investment ‘only’ delivers 15%. That’s nothing to cry about.

What will I do?

We’re building a portfolio from scratch. If you’re a premium member, can you consult it at our investor portal, 100baggerhunter.com

There are currently 4 positions in it. We use a 15% hurdle rate. Once we’re fully invested, it seems logical to increase the hurdle rate. After all, the goal should be to only replace the companies in the portfolio for 2 reasons:

The business, for some reason, breaks down

You find something better

And the easiest way to find something better is to increase the hurdle rate.

Let me know what you think of this.

Have a great weekend.

And may the markets be with you, always!

Kevin

A hurdle rate of 25% is really high. Do you ever find something priced so cheaply? I guess it must really be a niche company, because anything that’s remotely known, can’t have an expected return this high. Correct?

A high hurdle rate is a weapon. It forces you to stay patient, disciplined, and avoid getting sucked into mediocre opportunities. Constellation focuses on execution and capital allocation. If you're not actively making what you buy better, you're already at a disadvantage. So yeah, set a high bar, but make sure you're holding your own feet to the fire too. Otherwise, it's just another number.