How to find your investing edge for outsized returns

What's your edge?

Hi hunters,

If you’re new here.

My name is Kevin, and after 15 years in the markets, this is my investing strategy.

Our 2 portfolios, created at the start of 2025, are doing well, outpacing the S&P500 nicely.

No leverage.

No short positions.

Uncorrelated to the S&P500.

We are sitting on a 45% return since inception compared to the S&P’s 28%.

I mainly hunt for microcaps that can double several times. And as long as the business keeps performing, we can keep holding and maybe nail a 100-bagger.

If this strategy resonates with you, you can unlock the full content, all 400,000 words ⬇️

Today, we’re going to talk about edges. And why it’s important to find your own.

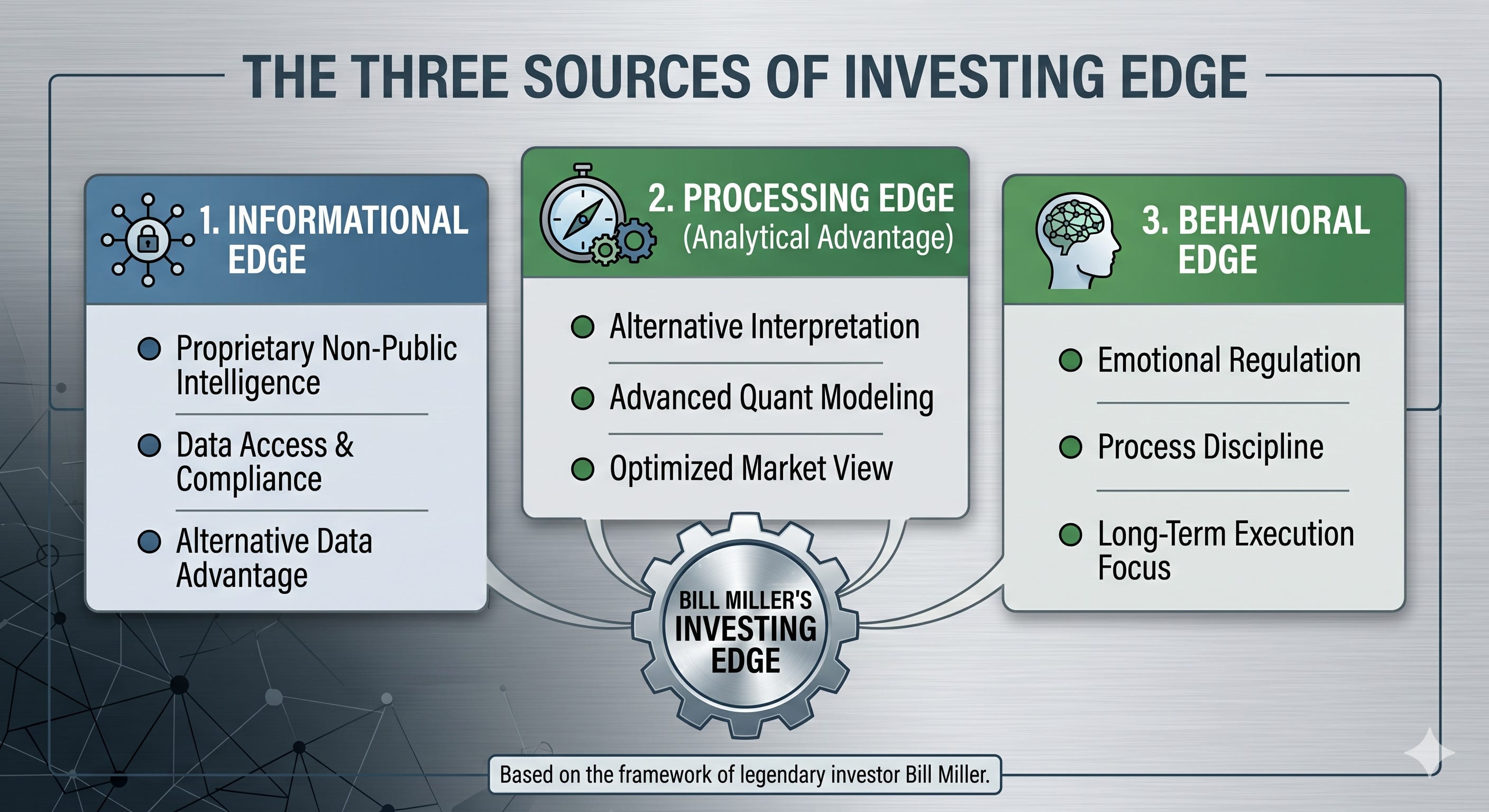

Bill Miller, a renowned value investor, mentioned in the past that an investor’s edge can be sourced in 3 areas:

Information

Your process

Your behavior

What I consider my edge can be broken down into 3 parts:

Choosing the right arena: Microcaps

Having a unique lens: Grounded in physics

Amplifying my entire process (ideas, research) through AI

This may surprise you, but I do not consider myself a growth, value, or quality investor. (although growth is always needed)

I don’t want to be locked inside a category.

I hunt for mispricings in the market.

Mispricings mean the market prices a stock below its intrinsic value.

Why?

Because of an overall market crash, the easiest

Because of a sector downturn: a bit harder → check our analysis of the Saaspocalypse

Because of a company downturn, the hardest

Behavior is important, but information asymmetry is often overlooked.

Information asymmetry means:

Having information that the market does not (very rare)

Having information that the market only recognizes slowly (rare)

Processing information in a unique way to create a different view (more common)

That asymmetry is most pronounced in the microcap space. Constructing a different view is easier thanks to my background in nuclear physics.

Let’s go through Bill Miller’s framework and how you can think about this for yourself.

The informational edge

Information is what we discussed in the introduction. The fact that you have information the market does not have, or has not recognized yet.

When Buffett was browsing through the Moody’s manuals, going through thousands of pages all those decades ago, he was exploiting an informational edge.

As you can see, a Moody’s page is not very sexy.

Imagine browsing through thousands of these.

In that time, you did not have an online broker. Quotes for stocks were displayed in the newsletter. If you wanted to buy a stock, you had to call your bank, and it took time.

Time flowed more slowly back then.

But going through those manuals, Buffett did something few others did. He took the time and effort to search for a needle in a haystack.

He created information asymmetry for himself.

And when he started out, he hunted for small companies, sometimes obscure, with low liquidity. Focusing on their balance sheet, buying companies at 25% of their cash value. Coca-Cola and Apple came later, when he had significant capital to deploy.

Buffett is a very smart man. And a shrewd investor. That’s without a doubt.

Last year in Omaha, I was impressed by how sharp he still is at 94.

But what he did in his early days had nothing to do with being smart.

He chose a specific arena: Micro and small caps

He hunted for information asymmetry: Going through the Moody’s manuals

And this asymmetry was even more pronounced when he became known as a smart businessman looking to buy companies.

He did not only have to hunt for ideas as we do.

Ideas came to him.

He got a deal flow that is not accessible to most investors.

That again is an example of information asymmetry.

The processing edge

The beauty (and difficulty) of the stock market is that 2 analysts, with exactly the same information, can come to different conclusions.

Making money in the markets is about creating a variant view of what the market has priced in.

And a variant view is created by having a unique process (or unique information).

Did Buffett have a unique process?

I don’t think so.

But what he did do was be very picky about what he was processing. He chose his arena carefully.

Before trying to be the best at a certain game, be mindful of what game you want to play.

He only looked at things he deeply understood.

By gaining a deep understanding, you gain conviction.

Through conviction, you withstand volatility in the markets.

That’s how you make money. It avoids you selling at lows.

So even if Buffett did not have a unique process, that doesn’t mean you can’t.

My process is grounded in physics. Yours could be completely different based on your background.

What helps is writing it down. (for me)

Buffett has never written down his process. (Others have tried in numerous books, though.)

The behavioral edge

If you’re a quant, all decisions are based on rules.

Buy on X, sell on Y.

I’m not a quant, and I am envious of their strong process. The human element is involved only in constructing the process itself.

So why don’t all quants win, even if their backtesting shows outperformance over multiple decades?

Because there will be years when a quant process underperforms, while the rest of the market does well. (you can see this in backtesting).

That’s hard.

Imagine your quant portfolio is down 15%, and the market is ripping.

You start doubting your process. Do I need to change it? And most investors will intervene, possibly breaking a great quant strategy, because they could not stomach a temporary loss.

Buying a position is easy. It’s the easiest decision one can make. Behavior still matters, though. Don’t chase a stock because of FOMO.

Buy because you did the work. Have a variant view of the market. No emotion.

But behavior is a much bigger factor when volatility kicks in. It comes down to the question:

When do you sell a position?

My stock is down 30%, what do I do?

My stock is up 100%, what do I do?

My stock has done nothing for a whole year. What do I do?

The perfect setup is when your business keeps performing, and the stock price tracks performance perfectly.

But that never happens.

Many investors say their edge is taking a long-term view. Decades.

It’s easier said than done. And most companies don’t earn your attention for a full decade. Most falter. Only a few outperform.

Our solution to solve the behavioral problem is the 2 last two parts of our edge.

Our process, grounded in physics, aims to eliminate emotional decision-making. Like a quant, we want our process to be so strong that it becomes the primary reason for a decision.

Secondly, one of the prime uses of AI is to counter our behavioral biases. It’s our bullshit detector. AI is designed to conform to you. But you need to set it up so that it disagrees with you.

You can do some incredible things with Claude: build advanced screeners and automate portfolio tracking, but the number one use case remains pushing back on your ideas.

We’ve written about different behavioral biases in the past. Check them out in our archive.

How to find your edge?

Start by thinking about it.

Take a pencil and a piece of paper. Use the Bill Miller framework.

Now write down what you believe your edge is.

If you struggle at first, don’t sweat. It’s an iterative process. You write down what you know. And you come back to it once a year. Over time, your edge will surface.

One thing is important: Notice that our edge is very specific. We choose an arena. We use a unique lens. We state how we want to tackle our behavior.

If you write down: My edge is: ‘I think long-term’.

That’s not enough.

What actions are you taking to support that claim? Apply first principles. Try to break it down to its bare bones.

Get away from the abstract and write down specifics.

A unique edge could look like this. Let’s say you’re a medical doctor.

Arena: We only invest in the healthcare sector

Lens: Biology. You analyze companies with a unique framework. (There’s a great book: What I learned about investing from Darwin)

Every investor’s process is unique. It is based on past experiences and learnings.

The goal is to keep learning and refining your process every year.

It took me 15 years to find my edge. And maybe in 5 years, it will have changed again.

It’s a journey, not a destination.

So, a final question: Care to share your edge?

May the markets be with you, always!

Kevin (Atomical Capital)

P.S.: Write-up almost ready on a new company + update on some of the holdings. Stay tuned. Got delayed a bit due to sickness.