The 15 best stock pitches from Omaha part 2

Part 2/3

Dear fellow hunters,

This is part 2 of the best stock pitches from Omaha.

You can read part 1 here.

Each company will have:

A short description of what they do

The type of company they are

The pitch

Only 48 hours left!

If you hesitated about taking a paid subscription, we’re running a special Omaha sale for the next week. You’ll get 25% off an annual subscription. Prices of the annual subscription will go up permanently after the sale. This is your chance to lock in the current rate.

Now let’s look at the next 5 stocks. The best ones are at the end of the article.

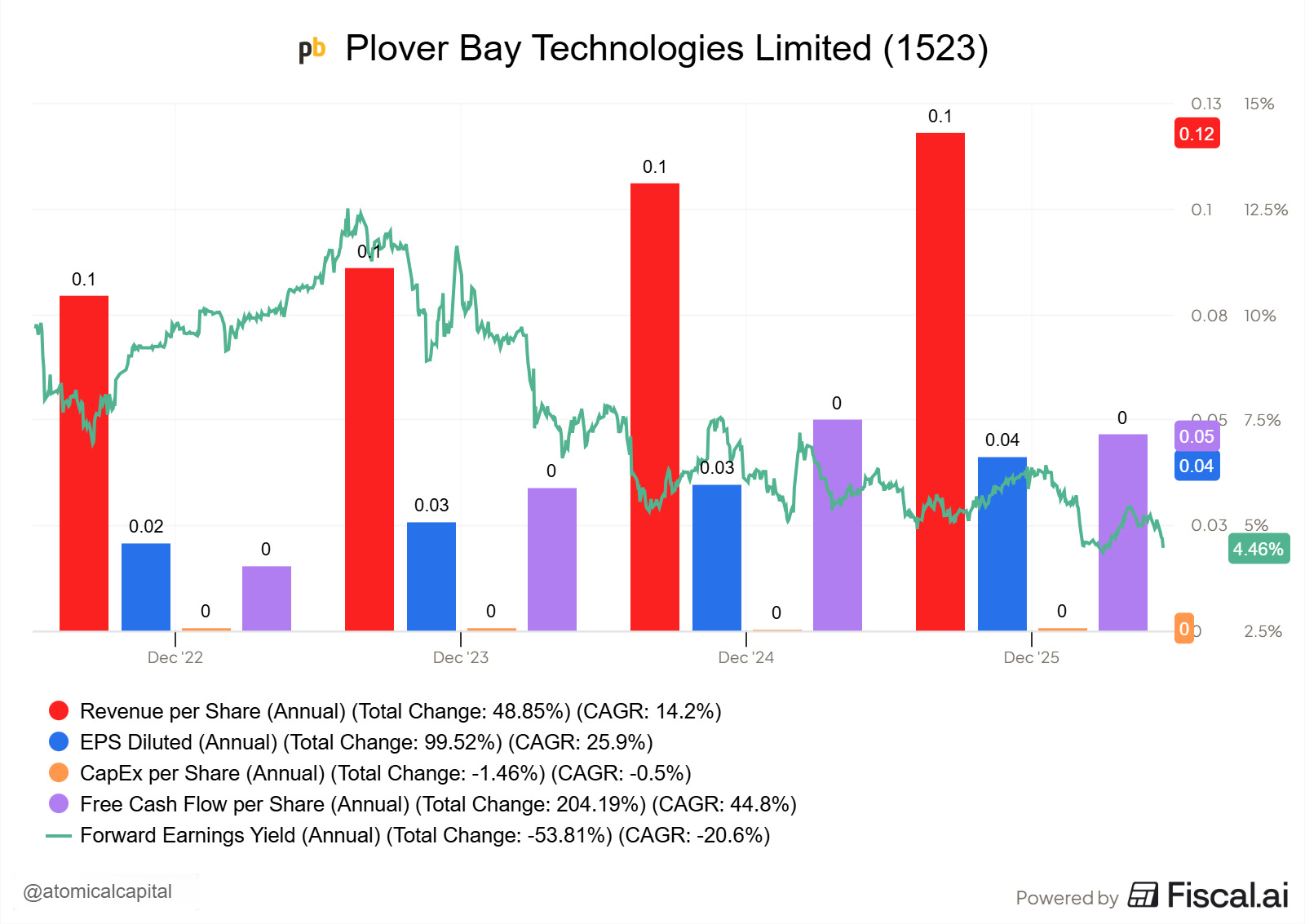

5 Plover Bay Technologies (1523 on the Hong Kong stock exchange)

Description: Plover Bay is a Hong Kong hardware-and-software company that makes routers and subscriptions for customers who need their internet to never go down.

Their customer: A firefighter captain rolling out of the station in Los Angeles during the January 2024 wildfires. He needs maps, weather feeds, a live video link to dispatch, and a connection to the hospital if a firefighter gets hurt. The cell tower three miles away is on fire. The cell tower behind her is congested because half the city is calling family. His satellite dish works, but only when the sky is clear of smoke.

He calls a normal enterprise networking vendor like Cisco. Cisco sells beautiful gear for a corporate office. They don’t really sell a single box that takes one Verizon SIM, one AT&T SIM, one Starlink dish, and one satellite phone, and welds them together into a connection that just keeps working when any one of them dies.

They use a land-and-expand business model.

Three revenue lines, stacked on top of each other.

Sell the box. A router with multiple slots for SIM cards, ethernet cables, and satellite uplinks. This is the chunky upfront purchase. Hardware was about 71% of revenue in 2024.

Sell the subscription. The router’s magic only works if you pay an annual fee for SpeedFusion (their bonding software, which ties multiple internet links into one) and InControl (cloud software that lets you manage a fleet of routers from a dashboard).

Sell the warranty. Annual support contract. Renewable.

It’s a capital-light business as all manufacturing is outsourced.

Type: Steady growing cash printer

The pitch: It's not that this company keeps growing earnings by 25% each year. Or that it gives back most of the cash through dividends. All those things are true.

The pitch is that almost 60% of their business comes from the US, and they have announced a spin-off to list on the Nasdaq in 2026.

Compared to US peers like Ubiquiti or Digi International (with much lower margins), that could lead to a 50% upside just from the rerating.

Here’s the overview: look at the FCF margin!

The spin-off is on track to be completed towards the end of the year.

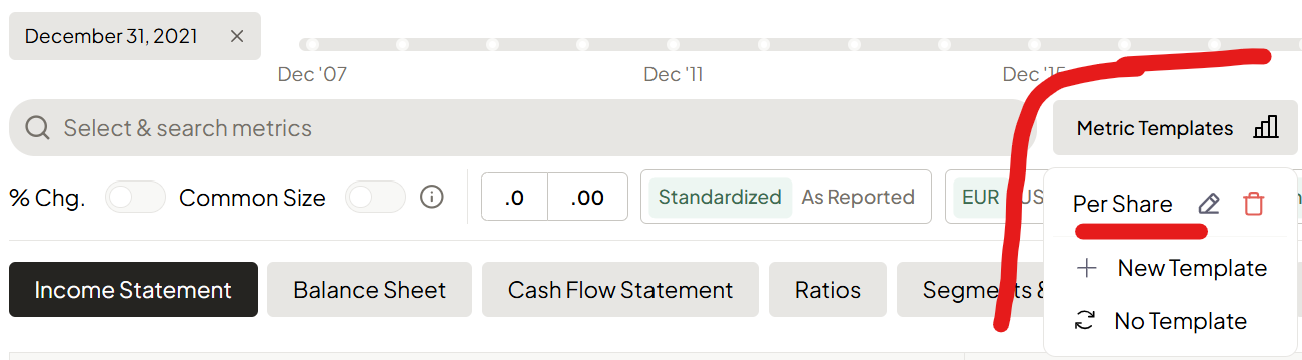

As you might have noticed, I use the same charts from fiscal.ai in every pitch. All per-share metrics are combined with the forward earnings yield. You can set this up once by creating a metric template:

Fiscal is running their annual 25% discount. You can use this link to get access.

4 Tasmea (TEA on ASX)

I wrote about Tasmea in a previous article.

Description: Tasmea is an Australian industrial services group that fixes, maintains, and upgrades the equipment inside big mining and utility plants for the giant companies that own them

Customer: A plant manager at a BHP iron ore site in the Pilbara, a remote corner of Western Australia. Her plant moves rocks, crushes them, separates iron ore, and loads it onto trains. The plant runs 24/7. Every hour it sits idle, the company loses about $500,000 in shipments. One morning, a giant electrical switchboard fails. She needs specialist high-voltage electricians on a plane today, with the right safety credentials, the right insurance, the right relationship with BHP’s procurement team, and the willingness to live in a camp 1,500 km from anywhere.

She calls a big generalist engineering firm. They build new plants. They don’t fly six tradespeople into a desert tonight to fix a switchboard. She calls a local electrician. He doesn’t have the high-voltage tickets or the BHP-approved safety system. She calls a global services giant. They want a 12-month contract negotiation. None of them are built for what she actually needs: specialist trades on call, sleeping in a camp, fixing the plant by morning. That’s the customer Tasmea was built for.

The actual customer base is what Tasmea calls “blue-chip essential asset owners”: large miners (iron ore, gold, copper, lithium), electricity transmission companies, water utilities, and oil and gas operators. In FY25, around 94% of Tasmea’s revenue came from repeat customers, and a single customer accounted for about 24% of total revenue.

The business model is simple: It’s labor arbitrage. Tasmea bills out skilled tradespeople (electricians, boilermakers, riggers, fitters) at a markup over what it pays them. That alone is a normal staffing business.

What makes Tasmea different is this:

The customer doesn’t care what Tasmea costs; they care that the plant keeps running. When a $4 billion iron ore mine is losing half a million dollars an hour, nobody is haggling over the electrician’s hourly rate. That’s why Tasmea earns roughly 25% gross margins and 15% EBITDA margins, while peer construction and engineering firms earn closer to 10%. Combine that with 70+ Master Service Agreements (multi-year contracts that lock Tasmea in as a preferred supplier), and you get a record $600 million secured order book heading into FY26.

Type: Roll-up (serial acquirer)

The pitch: It’s not complicated. You’re buying a high earnings growth roll-up (30%/year) in a boring industry at a forward P/E of 19. Tasmea profits from an electrification tailwind in Australia. Their electrical segment grew 66% in 2025 and contributes 44% to net profit. Management guides towards 110M in NPAT by 2028-2029. At today’s multiple, that’s a 3.7B company compared to a current multiple of 1.5B.

You can see from the chart that revenue is growing fast. Their capex seems low, but that’s because many acquisitions are cash, not reflected in the capex number. So the actual number per share is double or triple what is shown in the chart.

I like Tasmea; I liked it even more 2 months ago when I first wrote about it 😉 (when the price was 50% lower). But the company keeps performing, and more and more analysts have taken notice, which explains the multiple expansion.

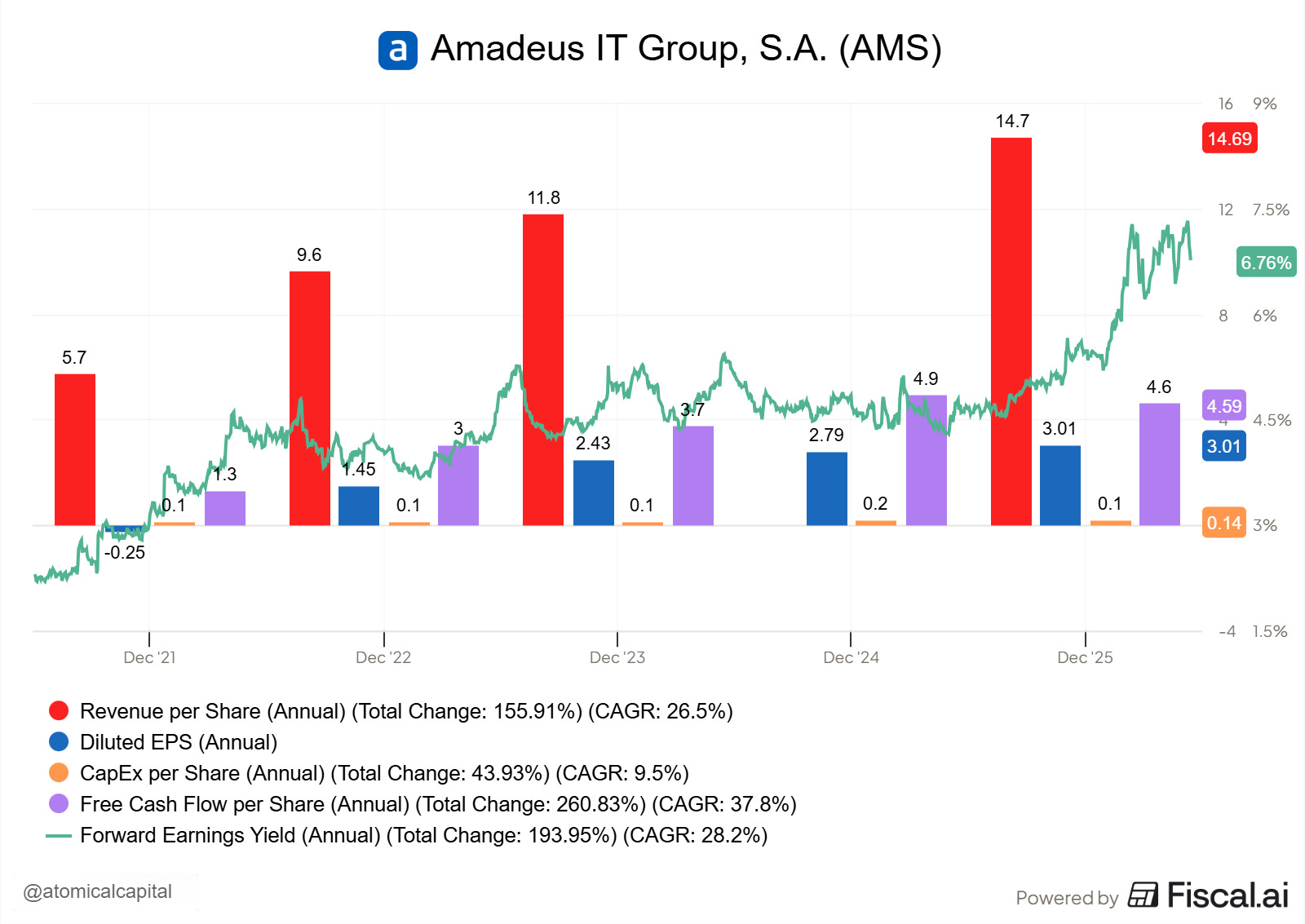

3 Amadeus IT Group (AMS on Bolsa de Madrid)

Description: Amadeus IT Group is a Spanish travel technology company that runs the booking plumbing between airlines, hotels, and travel agencies.

Customer: TAP Air Portugal. A medium-sized airline with a decent network out of Lisbon, mostly flying Europeans to Brazil. They want their flights to show up when a travel agent in Singapore types “Lisbon to Rio” into a screen. They also want to be bookable by a corporate travel desk in Frankfurt and an online travel site in Dubai.

So they call Singapore. “Hey, can you integrate with our reservation system?” Singapore says no. Singapore already has 700 airlines they could integrate with one by one. Nobody is building 700 custom phone lines. Dubai says the same thing. Frankfurt too.

That’s the customer Amadeus was built for.

Airlines plug into Amadeus once. The moment they do, they are bookable by around 190,000 travel agencies and online sellers worldwide. The same model works in reverse for the travel agents.

Amadeus runs three businesses, and the mechanism is different for each. Total group revenue in 2025 was €6.5 billion.

Air Distribution (€3.1 billion in 2025). This is the GDS, short for Global Distribution System. A giant electronic marketplace. Airlines list their seats. Travel agencies search for them. When the agency books a ticket, the airline pays Amadeus a fee per booking, roughly €5-€6 per ticket. The travel agency pays nothing. Amadeus often pays the agency to use Amadeus instead of a competitor. Those payments are called incentives, and they are a major cost line item.

Air IT Solutions (€2.3 billion in 2025). This is software-as-a-service for airlines. Amadeus runs the airline’s reservation system, inventory, check-in, and boarding. Their flagship product is called Altéa. The airline pays a fee for every passenger boarded. If Altéa goes down, the airline cannot fly.

Hospitality and Other Solutions (€1.1 billion in 2025). Same model, but for hotels. Marriott and Accor both pay Amadeus to run their central reservation systems. Add some payment processing and travel data on top.

This is a two-sided network. The more airlines on Amadeus, the more useful it is to travel agents. The more travel agents on Amadeus, the more useful it is to airlines. Sabre and Travelport are the only real competitors. That is the whole market. Three players. The switching costs are enormous. When Ryanair runs on Amadeus’s low-cost-carrier system Navitaire, ripping it out and replacing it is a multi-year, multi-million-euro project that nobody wants to greenlight. So they renew. Ryanair just renewed for another stretch, marking 25 years on the system.

Type: Monopoly in a 3-player oligopoly (mature growth)

The pitch: Amadeus has a 40% market share of global airline bookings, 20%+ net margins, zero net debt risk, and multi-year recurring contracts with the world's biggest airlines and hotel chains.

It is the picks-and-shovels play on global air travel growth (which has outpaced GDP for 50+ years), it grows revenue mid-to-high single digits, returns cash via dividends and a €1.3bn buyback program, and it just signed Marriott, Accor, British Airways, Air France-KLM, and Lufthansa Group to long-term deals. The stock is down 30% over the past year, trading at the lowest multiple in a decade.

The stock is down on AI fears. But they seem to be overblown.

Booking a flight is not the same as searching for a recipe. It requires real-time inventory, fare rules, seat maps, payment processing, and PNR creation (PNR = the booking record). AI agents that try to book directly still need to hit somebody's infrastructure. That infrastructure is Amadeus, Sabre, or the airline's own system (which is often, you guessed it, Amadeus's Altéa).

Amadeus has already signed British Airways, Air France-KLM, and Lufthansa Group as launch customers for Nevio, their AI-native airline retailing product. So far, the data says AI is making them more relevant, not less.

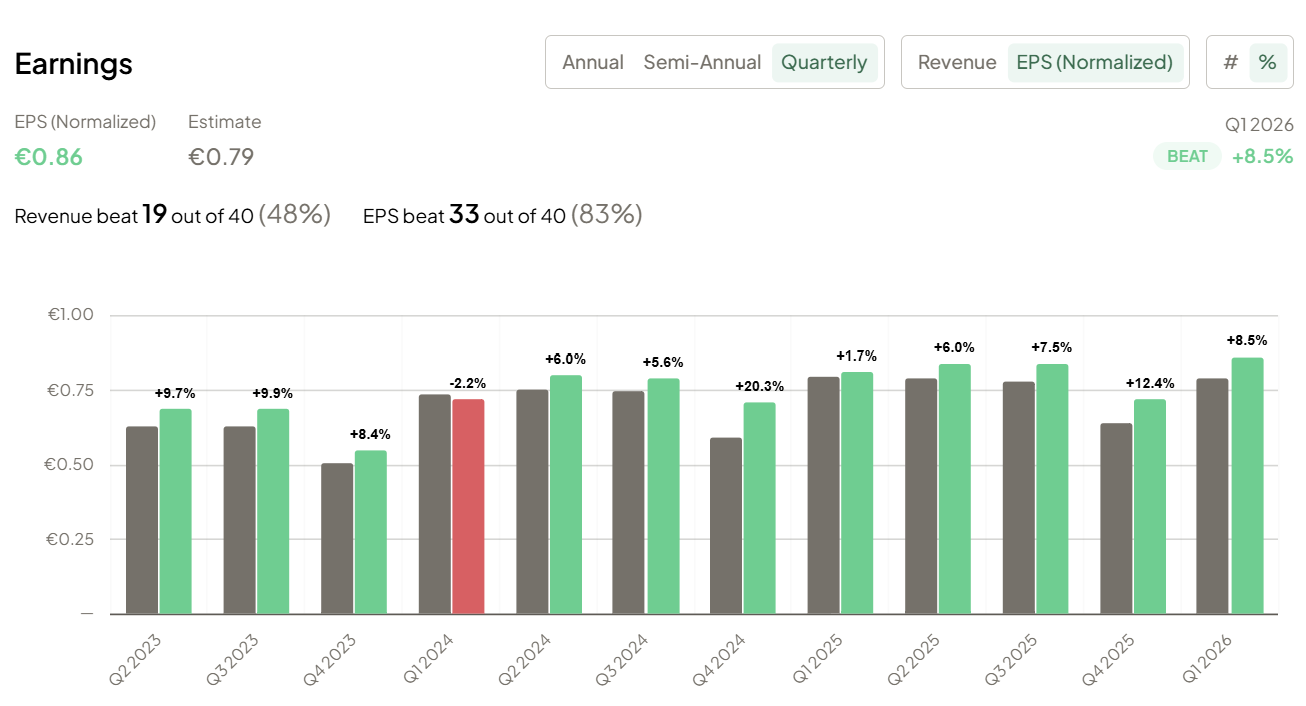

The beat expectations on their latest Q1:

The bet is achieving about 15% annual growth in earnings, dividends, and buybacks. If the stock reverts to its prior multiples, you’ll earn more.

Now let’s get to the final 2 on this list.

If you want full access, consider the current 25% discount to continue reading.

Let’s dive in: