The 15 best stock pitches from Omaha part 3

Part 3/3

Dear hunters,

This is part 3 of the best stock pitches from Omaha.

You can read part 1 here and part 2 here.

Each company will have:

A short description of what they do

The type of company they are

The pitch

Only 24 hours left!

If you hesitated about taking a paid subscription, we’re running a special Omaha sale for the next week. You’ll get 25% off an annual subscription. Prices of the annual subscription will go up permanently after the sale. This is your chance to lock in the current rate.

Now let’s look at the last 5 stocks. The best ones are at the end of the article.

5 Wise- Ticker WSE on the Nasdaq)

We wrote a deeper article about Wise here.

Description: Wise is a cross-border payments company that moves money between countries for people and businesses more cheaply and easily than their banks.

Their customer: A Polish nurse works at a London hospital. She earns about £2,800 a month and sends £400 home to her mother in Krakow on the first of every month. She walks into her bank, asks for an international transfer, and they tell her it'll cost a £20 wire fee. What they don't tell her is that the exchange rate they're giving her is roughly 3% worse than the rate you'd see on Google. So, on a £400 transfer, she's actually paying about £20 in visible fees plus another £12 hidden in the exchange rate. Total costs: about £32 to move £400.

Now she tries the same thing with Wise. She gets the mid-market exchange rate (the real one, the one banks use among themselves), and pays one small upfront fee of roughly £2. The money arrives in her mother’s account in seconds.

Wise built its own payment rails instead of using the bank network. When HSBC sends money abroad, it goes through a system called SWIFT, which is basically a chain of banks passing your money along, each taking a cut. Slow and expensive. Wise instead set up real local bank accounts in roughly 10 countries and connected directly to local payment systems like ACH in the US and Faster Payments in the UK. When you “send money from London to Krakow,” nothing actually crosses a border. Wise just takes pounds from its UK account and pays out euros from its Polish account. The money doesn’t move.

This is the moat. Building those direct rails takes years and a banking license in every country. Once you have them, your unit cost per transfer is a fraction of what a bank pays. Wise then deliberately cuts prices every year, making it impossible for competitors to catch up. The take rate has fallen from 67 bps to 53 bps in a single year. Volumes grow faster than prices fall. Revenue keeps going up.

Type: Economies of scale growth machine

The pitch: Global cross-border payments are a £32 trillion market. Wise has roughly 5% of personal, 1% of SMB, and almost nothing of the £16 trillion enterprise segment. That last bucket is the real motherload. Banks still own it because they make fat margins on FX. It will take years to gain a foothold, but the runway is huge.

The competition isn’t really competition. Remitly is a consumer remittance app. Revolut is a super-app.

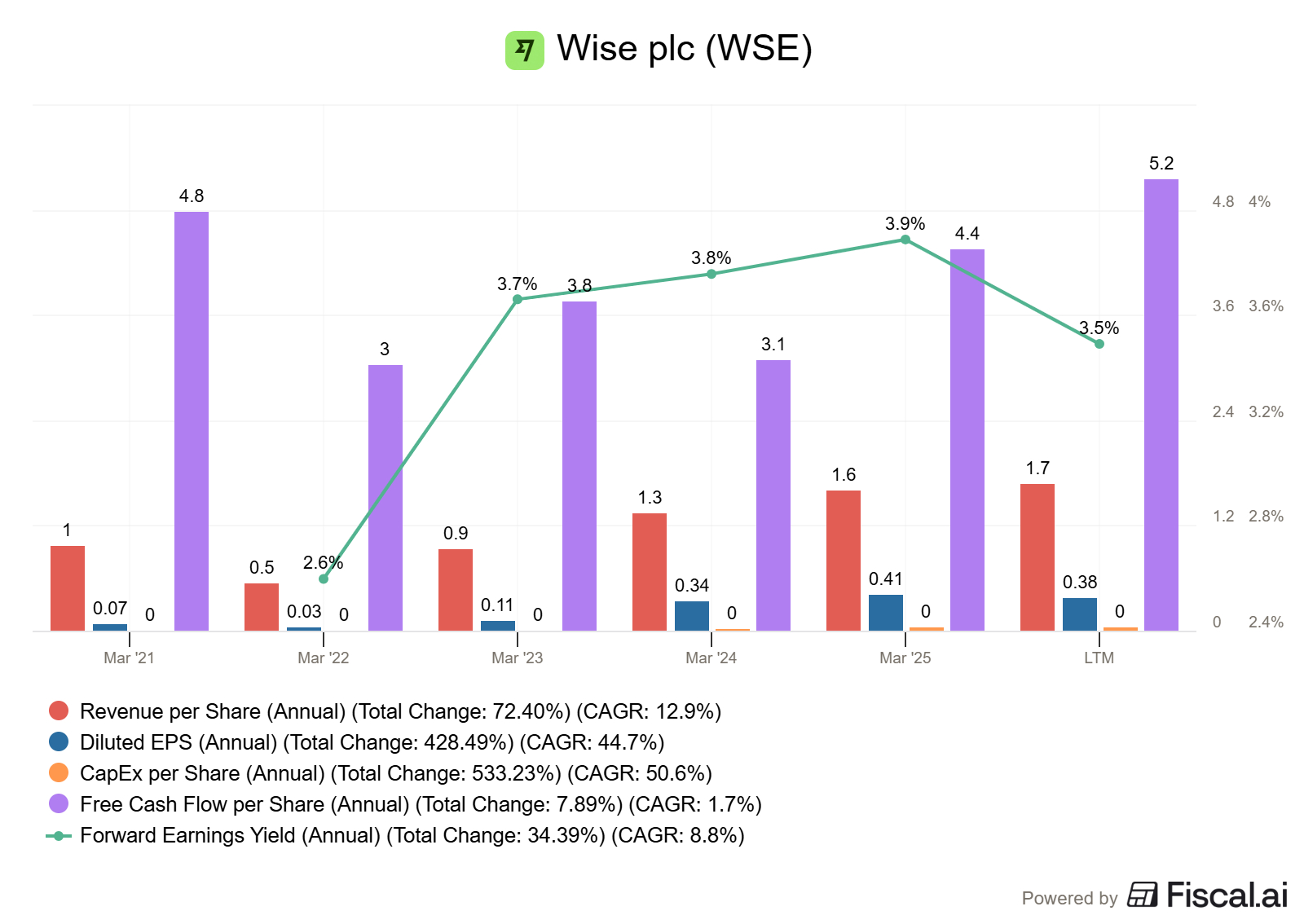

Here’s the data from fiscal.ai:

The FCF per share is larger than the revenue per share, but that’s because of the deposits.

Wise is deliberately under-earning today to build a payments network so cheap and so wide that nobody else can profitably catch up, and the market is punishing them for it.

4 Organo (6368 on Tokyo Stock Exchange)

Description: Organo is a Japanese water treatment company that builds the ultra-clean water systems chipmakers like TSMC use to wash silicon wafers.

Customer: To make a chip with circuits 3 nanometers wide (about 25,000 times thinner than a human hair), the engineers need water that is insanely clean. Not "bottled water" clean. We're talking water so pure it has almost no dissolved minerals, no metals, no microbes, and zero particles bigger than 10 nanometers. This is called ultrapure water (UPW). A single fab can use tens of thousands of tonnes of it a day.

As of FY03/25, Organo controlled an estimated 70 to 80% of TSMC's water treatment plants and roughly 100% of plants supplying fabs at 10 nanometers or smaller. TSMC alone is 14% of their revenue. Their core customer base is the world's most advanced semiconductor fabs, plus a long tail of pharma plants, power stations, and food refineries that also need very clean water.

They make money by building the water treatment system on site and then running it forever. This creates enormous switching costs.

A “boring” 80-year-old Japanese plumbing company that quietly became a chokepoint in the global semiconductor supply chain, paid first to build the water plant and then paid forever to keep it running.

Type: Slow growing but high operational leverage

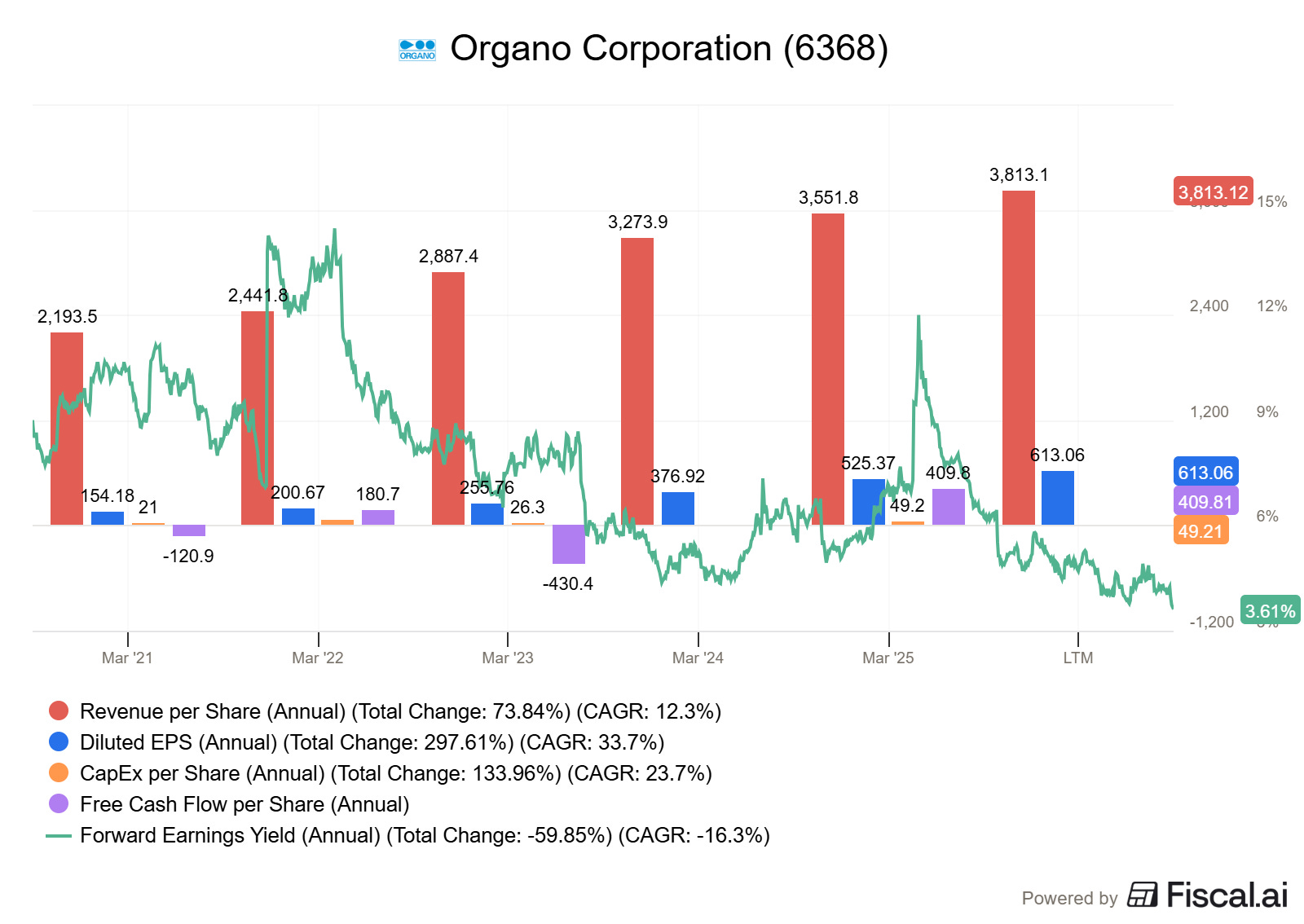

The pitch: Organo has a dominant market share. Their margins have expanded over the last few years, but it’s not by accident. There are 3 reasons: the service business is growing as a share of revenue (now 40-50% of sales). Tight UPW supply lets Organo charge premium prices on new builds. High-margin specialty chemicals and resins are made in-house. This is why earnings have grown faster than revenue.

TSMC is building fabs in the US (Arizona), Japan (Kumamoto), and Germany. Organo is following them. Their US business is being built out alongside TSMC's CHIPS Act fabs. The pharma side, especially injectable drug water, is also accelerating.

This is a strong company with a moat, where EPS is growing faster than revenue. The market has taken notice and priced it higher.

3 Samsara (Ticker IOT on NYSE)

Description: Samsara is a software and sensors business that helps trucking, construction, and field service companies see what their trucks, equipment, and workers are actually doing.

The perfect customer: Meet Maria. She’s the dispatch manager at a 90-truck regional trucking outfit in Memphis. Her job is to know where every truck is, whether her drivers are tailgating or falling asleep, when the next oil change is due, and why fuel costs jumped last month. In practice, she has a whiteboard, a stack of paper logbooks, and a phone that won’t stop ringing. When a truck misses a delivery, she calls the driver. When the driver doesn’t pick up, she calls his wife. That’s her tracking system.

Last year, she tried calling one of the big incumbent telematics vendors (think Verizon Connect, Geotab, Trimble). They told her: Six months of implementation and a six-figure quote. And software that still required three separate screens to locate one truck.

Samsara is a subscription software business.

A trucking or construction company signs a 3-year contract.

Samsara ships gateways, AI dashcams, and tags. Each device plugs in or sticks on in minutes.

The hardware streams data to Samsara’s cloud-based software.

The customer pays roughly $27 to $33 per vehicle per month for basic GPS, climbing to $40 to $60+ once you add the AI dashcam and driver coaching.

What’s interesting is the per-application, per-asset pricing.

If a customer has 50 trucks and wants both GPS tracking AND the video safety camera, that's 100 subscriptions, not 50. Every new product Samsara ships (equipment tags, site cameras, maintenance, workflows) is sold as a separate per-asset line item to the same fleet. Over 95% of their $100K+ customers buy two or more products, and that cross-sell is the growth engine.

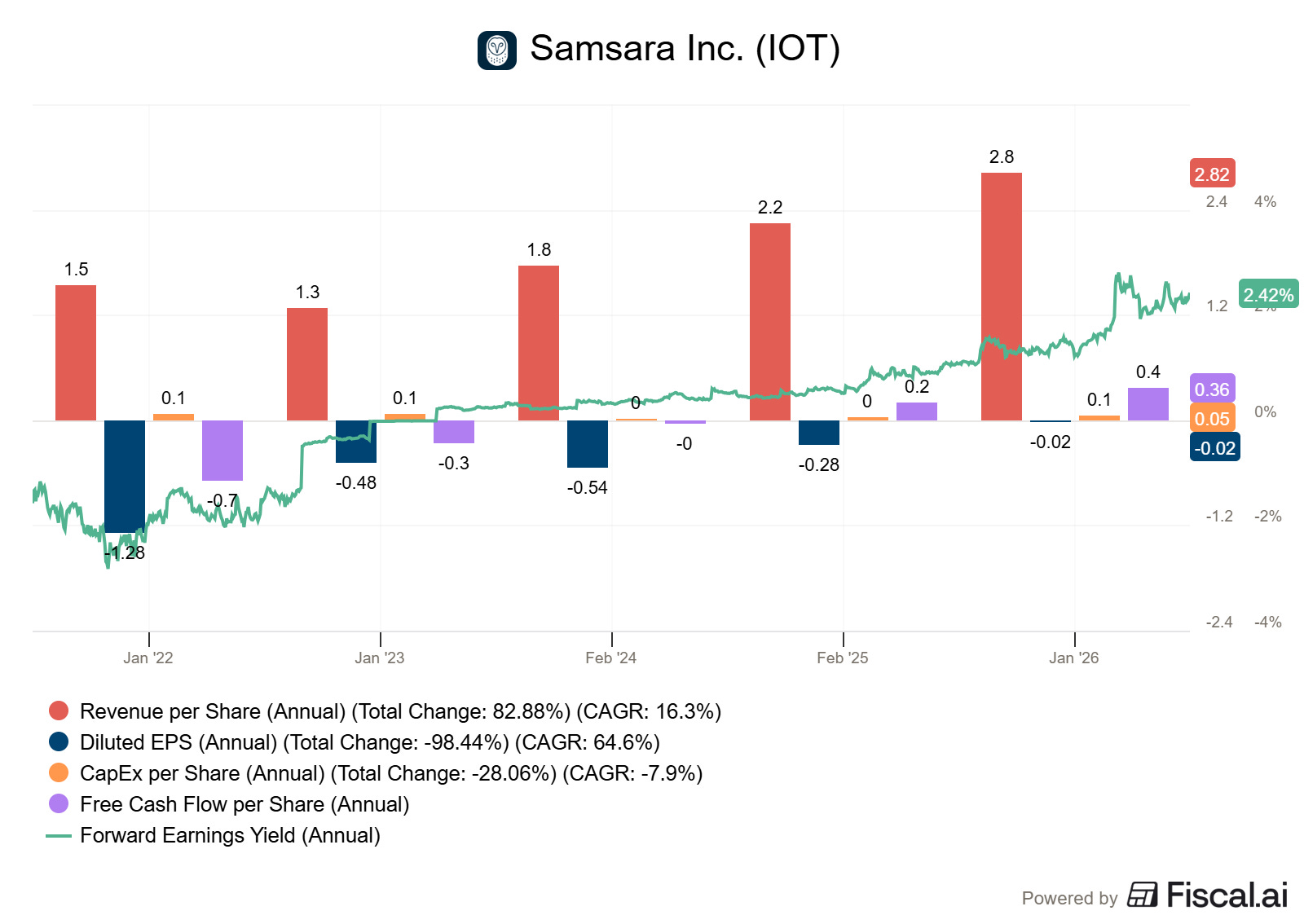

Here’s a chart you don’t see every day. Revenue and free cash flow per share are growing, and earnings yield to. That means the stock price is dropping while the business seems to be getting stronger and stronger. (stock is down 40% over the past year)

Type: Fast grower

The pitch: The market puts Samsara in the SaaS bucket and judges it on SaaS multiples. That's the mistake. Samsara is not a SaaS company. It's the company digitizing the physical operations of the working world, and the SaaS label undersells both what they do today and what's coming next.

Once Samsara's hardware is wired into a customer's 10,000-truck fleet or bolted onto 200 construction job sites, switching vendors is not a software decision. It's ripping off the most sticky band-aid, breaking compliance reporting, driver coaching workflows, insurance arrangements, and dispatch routines.

The next bet is AI for the physical world: robots, autonomous trucks, smart job sites, and electrified fleets. Samsara processes over 25 trillion data points a year through GPS telemetry, AI dash cams, and sensors, the kind of dataset you cannot scrape from the internet.

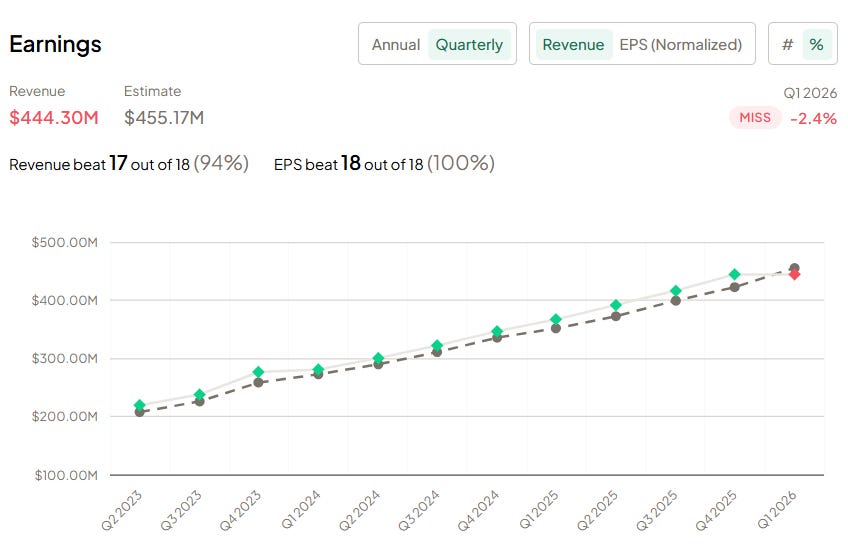

They have seen strong performance over the past years, but missed their last quarter (revenue, not EPS!).

If you want full access, consider the current 25% discount to continue reading.

Let’s dive in: