Position sizing for massive returns

The 2nd secret weapon

The casino ban

Mohnish Pabrai is special.

He has a Las Vegas casino ban from the blackjack tables.

And he did it without counting cards.

The casino lords were baffled.

They could not figure out how he beat the casino without a counting system.

Here’s what he did.1

There’s a website that can give you the odds for every blackjack table in the US. And usually the odds are slightly in favor of the Casino. 51/49 etc. So in that list, there was one table in the El Cortez where the edge for the casino was extremely slim. In blackjack, you regularly have streaks of 6-7 hands winning or, inversely, losing.

When he was losing, he would decrease his bets. But when he was winning, he would continue to increase those bets.

So even though the casino had the odds in their favor, by increasing his bets when the odds were more in his favor, he managed to beat the house.

But there’s an even better example of the impact of position sizing…

Master and Apprentice

Finally.

He had been given the role of lead portfolio manager of the Quantum Fund. It was 1988, and his future looked bright. The Quantum fund was a macro trading fund, looking for asymmetric bets wherever in the markets.

And in 1992, it was time for a home run. Our portfolio manager found the most asymmetric bet he ever encountered. He found that the British pound was overvalued and was betting on a devaluation of the currency. In other words, he proposed to short the British pound.

When he proposed this to his manager, the manager said: That’s a mistake. The bet is good, but we need to go in 200%, with leverage.

You probably guessed it. The portfolio manager is Stanley Druckenmiller, and the other manager is George Soros.

The master (Soros) systematically outperformed the apprentice (Druckenmiller) through better sizing.

“it’s not whether you’re right or wrong that’s important, but how much money you make when you’re right and how much you lose when you’re wrong.”

-George Soros

Soros’s approach was to make large, concentrated bets when conviction was high, often using leverage to amplify returns, and to cut losses quickly when a trade didn’t work.

Note: I would stay away from leverage, though.

You can boil the entire investing game down into:

Buy right

Size right

Hold on as long as possible

That’s it.

But not enough emphasis is put on that middle step: the sizing

The magic of power laws

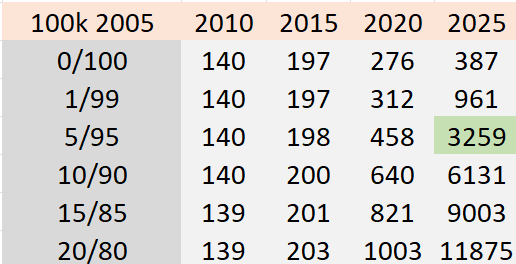

Let’s say it’s 2005, and you create a simple portfolio. An index fund combining with 1 single stock: Nvidia. We know that Nvidia will become a 100-bagger and then some. Now let’s vary the size of Nvidia. We’ll look at portfolios without Nvidia up to a 20% position. The index will return 7% each year over 20 years.

Now granted, Nvidia from 2005 to 2025 is a 670-bagger. So even a small percentage is crazy. But still, let’s look at what the results are:

The index alone grew from 100k to 387k.

Not bad.

But you can already see what happens when you add a tiny % of Nvidia to the mix. Suddenly, it balloons to 961k.

But at 5%, the portfolio starts to take off, towards 3 million USD.

If you remember how I construct our portfolio, for a core position, I bet anywhere from 5-15%. Read it here ⬇️

This is where the 5% comes from. For me, in the long run, it feels like the most minimal bet to have a solid impact on the portfolio. Everything below is an initial bet or speculative bet.

People who have a portfolio that outperforms is the result of a power law.

Outliers.

It’s the same in the stock market. 4% of all the stocks create 90% of the wealth. A power law. 2

Now the knife cuts both ways.

You take an underperformer and it starts losing for 20 years, you’ll see the impact. But I do hope you won’t hold on.

➡️Cut your losers fast, let your winners ride.

Sizing a bet

What did Monhnish and Druckenmiller have in common?

They increased their bet size when they felt they had an edge.

It’s not that easy. There’s no magic formula (sorry, Joel). It comes with experience.

There can be different edges:

Informational

Processing edge

Behavioral edge

Informational is probably rare these days. Maybe in the microcap space, you can dig deep and uncover information that very few investors have found, like we did with our favorite microcap. ⬇️

The processing edge is what Joel Greenblatt talks about. He explains it by looking at a company from a different angle. Like tilting your head, and seeing something that few investors see.

The last one is behavioral. Being able to stay calm when everybody panics. Or being greedy when others are fearful.

The most important thing is that the position sizing should come from conviction.

You can copy a man’s position, but you can’t copy his conviction.

-Unknown

And conviction is your 2nd secret weapon when volatility strikes (the first we covered last week).

My humble advice: Build positions slowly as your conviction in the investment case increases. Average up, or average down.

That’s what I do.

How do you handle position sizing?

May the markets be with you, always!

Kevin

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3537838

Position sizing makes all the difference. Thanks, Kevin!

Great post, the best part was about the conviction, I personally invested in a great business a year ago and the valuation was also good, but after few months I sold 100% stake cause I realised that I am not understanding the business properly.